1/ Book value is an increasingly flawed accounting metric which is creating issues for passive and active investors. This thread highlights research by my colleague @tbfairchild on 1) the problems with using book value and 2) potential solutions which correct the largest issues

2/ Two unusual categories of stocks have emerged.

Stocks with negative book values, and “veiled value” stocks, which are in the most expensive third of the market on p/book, but cheapest third on other metrics.

Stocks with negative book values, and “veiled value” stocks, which are in the most expensive third of the market on p/book, but cheapest third on other metrics.

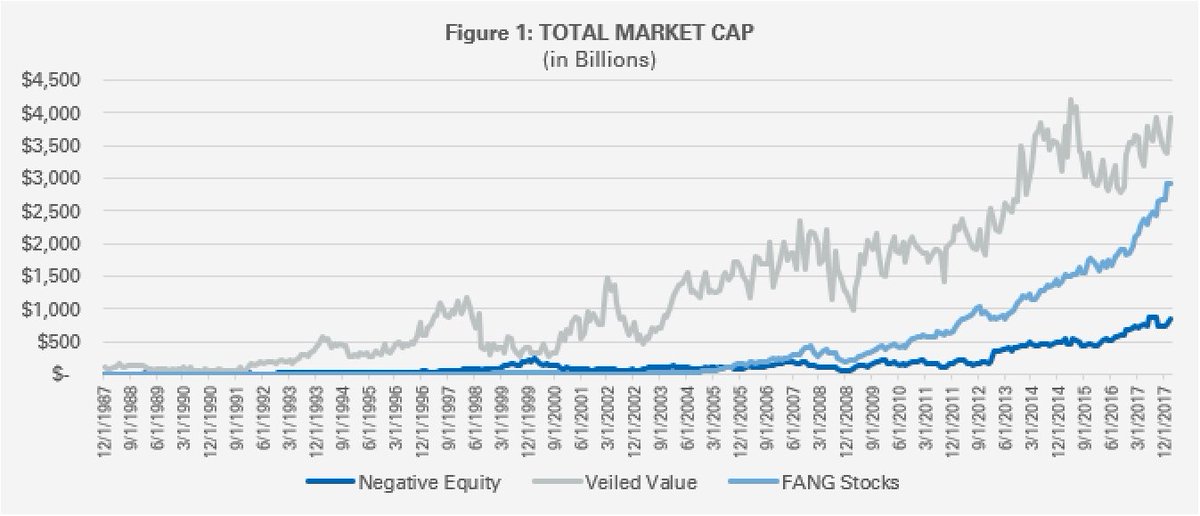

3/ In 1988, there were only 13 companies with negative equity with a combined market cap of $15B (infl adjusted); now there are 118 worth $843B. There also 258 veiled value stocks representing over $3.9 trillion of market value.

4/ Over 90% of the Veiled Value group of stocks are defined as growth stocks by Russell’s methodology. Of the 25 largest Large Cap Value funds ($817B total AUM), all but two of the managers were underweight the Veiled Value stocks. Average underweight these names by 5.7%.

5/ Why is this a problem? At least historically, both categories—negative equity and veiled value—have outperformed the market.

6/ This has happened for 3 primary reasons.

1) Understated intangible assets

2) Understated tong term assets &

3) buybacks and dividends

1) Understated intangible assets

2) Understated tong term assets &

3) buybacks and dividends

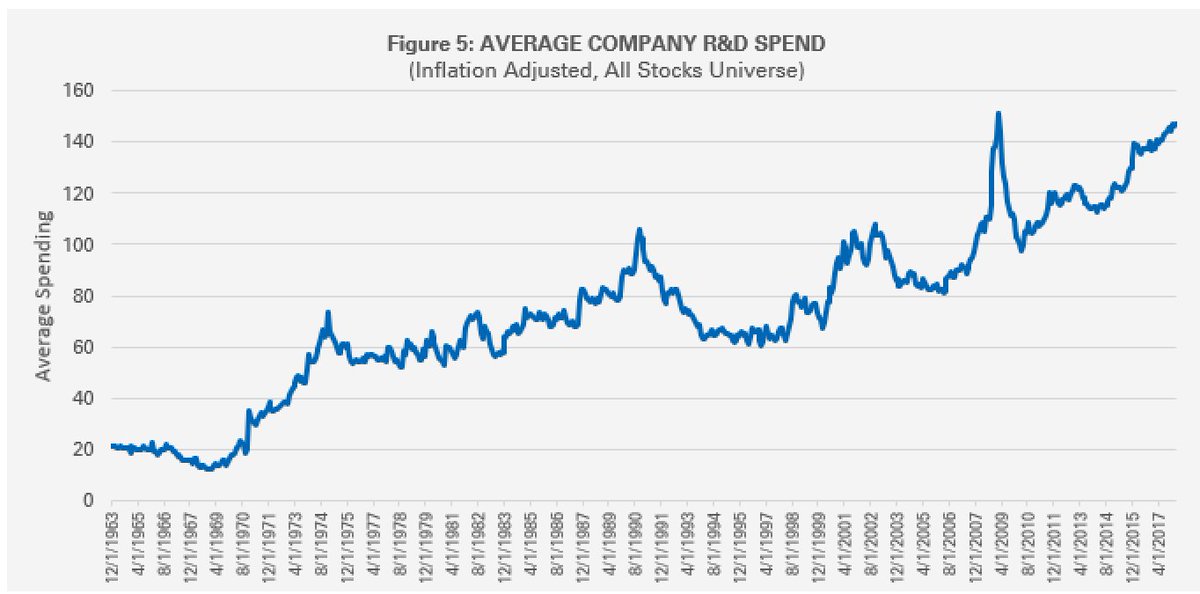

7/ First, intanbibles—brand names, human capital, advertising, and research and development (R&D)—are rarely represented on the balance sheet.

8/ the average company today spends much more on R&D than in 1975. Firms with substantial R&D expenses are common negative book value and Veiled Value companies. Boeing has spent over $100 billion designing aircrafts and all that investment does not create an asset.

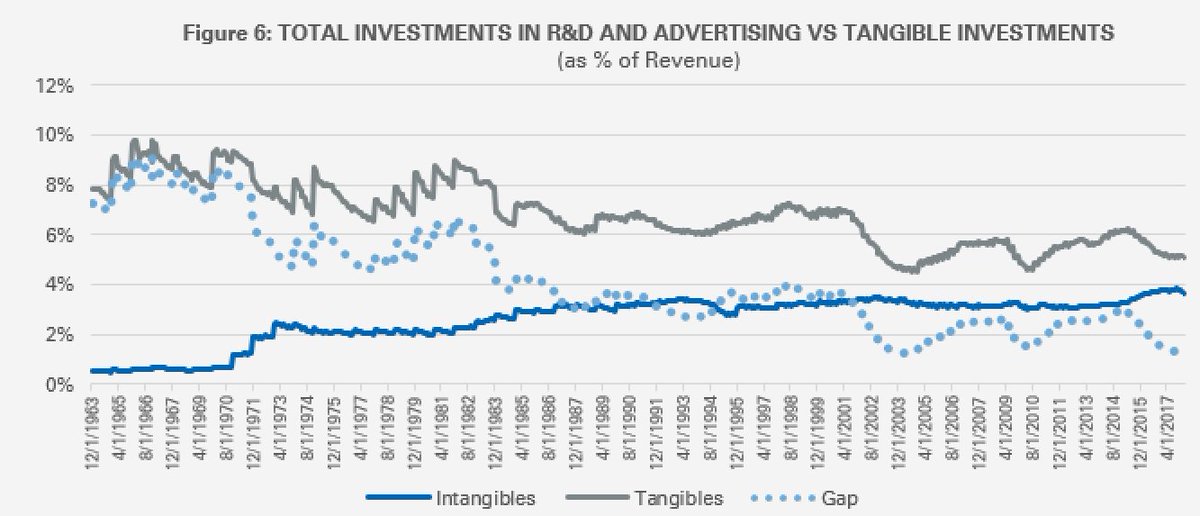

9/ Some researchers estimate that total intangible investments have surpassed investment in tangibles. Just looking at total R&D and advertising expense vs. total capital expenditure we see that the spend on these intangibles is converging with total tangible investments.

10/ companies like Interbrand try to estimate the dollar value of each company’s brand and the gaps between the market value and the book value is often measured in the billions of dollars

11/ Second, long term assets are often depreciated faster than their useful lives.

For example: companies with balance sheets that are nowhere close to reflecting the true value of their real estate owned.

For example: companies with balance sheets that are nowhere close to reflecting the true value of their real estate owned.

12/ some people value Macy’s real estate assets at multiples of their total market cap. The New York location alone valued at $3.3 billion would represent more than 50% of Macy’s market cap.

13/ McDonalds is a new member of the neg equity club and in addition to brand its’ real estate is well below market value on the balance sheet.

The once CFO of McDonald’s, Harry J. Sonneborn said, “We’re not technically in the food business. We are in the real estate business."

The once CFO of McDonald’s, Harry J. Sonneborn said, “We’re not technically in the food business. We are in the real estate business."

14/ That real estate is worth $Bs more than its book value. They depreciate their properties straight-line over the shorter of the lease term or 40 years. Their typical lease is 20 years so much of what they bought prior to 1998 and leased to franchisees is held on the books at 0

15/ Third, buybacks and dividends: when buybacks and dividends exceed net income, they create a decrease in equity which can accelerate distortions

16/ When a company has a price-to-book ratio that is above 1 then any buyback or dividend will decrease book value of equity by a larger percentage than it will decrease market value. To illustrate, take the simple example of two companies.

17/ Company B’s market value will also go down 20% but its book value will get cut by 50%, exaggerating company B’s already depressed book value and ending with a price-to-book ratio of 80/20 = 4

18/ So can we salvage price-to-book?

Here are some simple improvements one might make:

1) Create a Research Asset

2) Create a Brand Asset

3) Adjust Real Estate Values to Get Closer to Market Value

4) Adjust for buybacks and dividends (use as part of the ranking)

Here are some simple improvements one might make:

1) Create a Research Asset

2) Create a Brand Asset

3) Adjust Real Estate Values to Get Closer to Market Value

4) Adjust for buybacks and dividends (use as part of the ranking)

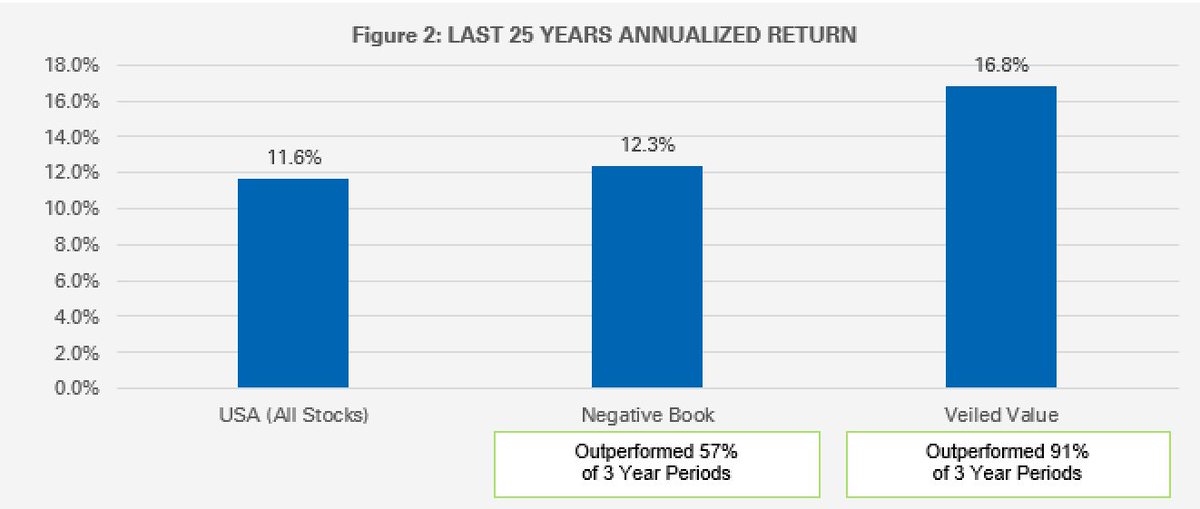

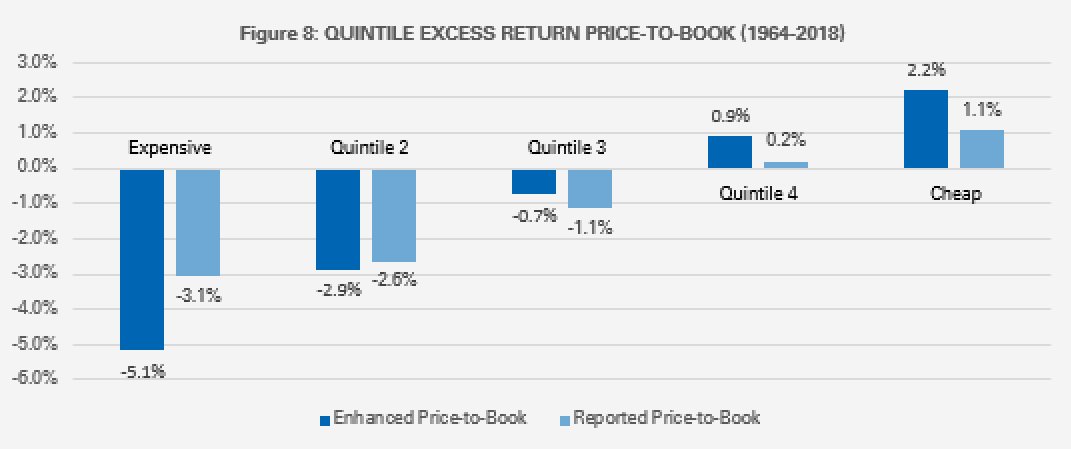

19/ This isn’t meant to be an exhaustive exercise, just an illustrative one. Here are the historical results.

20/ Like any investing strategy, factor-based strategies need to evolve and live in the real world. Book value has proved less and less useful, but is still broadly relied upon. Thanks to @tbfairchild for the deep dive. Follow that man!

21/ Here is the full piece, which offers far more detail osam.com/Commentary/Blo…