Im going to make a thread about why Digital Lenders should look at chamas and social savings as a new opportunity for digital financial products /n #CISConference2018

Digital lenders look at lenders from one lens - that of an individuals.

Its why their emphasis is skewed on collecting more data from individuals

Mobile phone

Mpesa

Airtime habits

Data bundle habits

SIM card data etc /2

Its why their emphasis is skewed on collecting more data from individuals

Mobile phone

Mpesa

Airtime habits

Data bundle habits

SIM card data etc /2

Yet in the real world Kenya people exist as individuals AND as individuals in groups ie Chamas, social savings groups, communities, social networks (online/offline)

This is V significant for a market like Kenya and arguably East Africa /3

This is V significant for a market like Kenya and arguably East Africa /3

Types of groups of Chamas we have come across

Merry Go round

Savings

Insurance

Investment Club

Traders

Cooperative

Causes /4

Merry Go round

Savings

Insurance

Investment Club

Traders

Cooperative

Causes /4

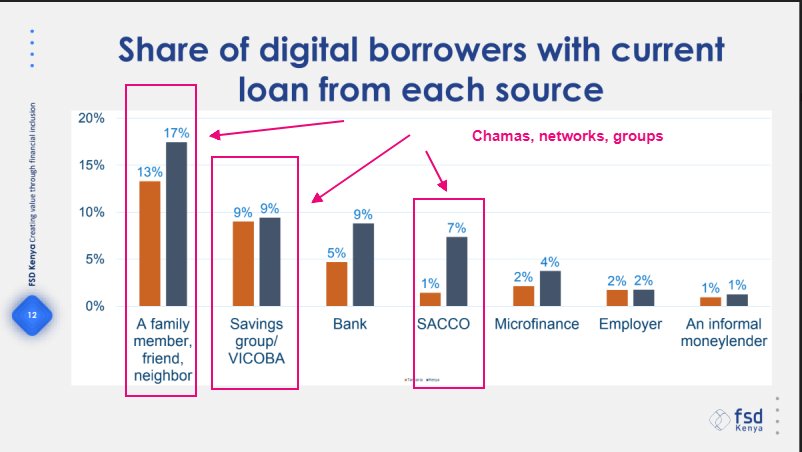

Have a look at these results from report titled Tech-enabled lending

in Africa a survey conducted by FSDKenya

It shows the share of digital borrowers with current loan from each source

Highest Aggregate sources = groups /5

in Africa a survey conducted by FSDKenya

It shows the share of digital borrowers with current loan from each source

Highest Aggregate sources = groups /5

So its important to take a look at Groups as users

Co-create with groups/chamas /6

Co-create with groups/chamas /6

Here is a list of what is ailing digital lenders in Kenya from all i have come across

Fraud (SIM/Identity)

Default rates

Looking for New Markets (originate new loans)

Competition for digital lending apps by (banks)

Cost of borrowing (price vs risk) How to price accurately /7

Fraud (SIM/Identity)

Default rates

Looking for New Markets (originate new loans)

Competition for digital lending apps by (banks)

Cost of borrowing (price vs risk) How to price accurately /7

More

Purpose lending (do you know where money is going hint: they dont)

Economic slowdown, less money in people's pocket

Calls for Regulation of digital lender

Too much focus on digital data/online, no clue what is going on offline

Privacy of data /8

Purpose lending (do you know where money is going hint: they dont)

Economic slowdown, less money in people's pocket

Calls for Regulation of digital lender

Too much focus on digital data/online, no clue what is going on offline

Privacy of data /8

Now lets have a look at how chamas, groups, trade networks solve all of these problems

Chama identity - you cant steal someone's chama Identity

Lower default because of social pressure from group (these are people you work with or meet everyday) /9

Chama identity - you cant steal someone's chama Identity

Lower default because of social pressure from group (these are people you work with or meet everyday) /9

New market - lending to chamas or lend to individuals via chamas

Banks haven’t encroached the chama market

Lending to individuals via chamas reduces risk of default (social pressure, guarantees)

Lend to professional chama groups - boda boda, mama biashara (inventory) /10

Banks haven’t encroached the chama market

Lending to individuals via chamas reduces risk of default (social pressure, guarantees)

Lend to professional chama groups - boda boda, mama biashara (inventory) /10

Lend to Savers in Chamas, lower risk - chamas for savings/chamas for investment

Chamas give you a better grasp of offline biashara b/c chamas are last mile

Privacy - group privacy & identity means Chama owns records/data

New products - insure-tech (emergency/burial chamas) /11

Chamas give you a better grasp of offline biashara b/c chamas are last mile

Privacy - group privacy & identity means Chama owns records/data

New products - insure-tech (emergency/burial chamas) /11

This stuff is already happening. And its NOT by digital lenders nor digital fintech

eg

Women's Chama group in ruiru accesses group insurance from Britam via group aggregators (ECLOF) /12

eg

Women's Chama group in ruiru accesses group insurance from Britam via group aggregators (ECLOF) /12

eg a long time ago Kiva (american lender) would lend to groups under a group aggregator (Joymwo) by leveraging groups guarantees and social pressure /13

eg Business groups in Ruiru access credit via groups managed by CBO (aggregator) where groups with surplus lend to groups with a deficit

Cross chama lending /14

Cross chama lending /14

eg Inventory lending where farmers association advances goods to Harriet fruit vendor on credit to pay later /15

eg I just met a SACCO at this event CIS Conference with 1000 people under their SACCO who are - guess what - all organized into groups! /16

Someone needs to build a Group platform that can open up all the latent data trapped in offline networks

I believe this will unbundle

New data

New markets

and

New digital products/services /n

I believe this will unbundle

New data

New markets

and

New digital products/services /n