,

28 tweets,

8 min read

Read on Twitter

1/ This legislation builds on a core idea from #WY: It must be possible for entrepreneurs to develop and sell software that is inherently consumptive in nature (i.e., not a passive financial instrument and intrinsically is for use/consumption) w/o implicating securities laws.

2/ The SEC seems to agree and so have regulators/policymakers in just about every other developed nation. The difficulty arises, however, in defining the boundaries of this principle - stated differently, when if ever is usable software actually a security?

3/ Many regulators have taken a clear bright-line approach based on a token’s intrinsic characteristics: Inherently consumptive or use-based tokens are never securities. The UK, France, and Singapore are among the regs/jurisdictions in this camp.

4/ The US SEC has taken a different approach. It evaluates a token’s intrinsic and extrinsic characteristics, the latter of which involves sales practices and objectives of reasonable purchasers. This approach is flexible, in ways that arguably are both good and bad.

5/ The (arguable) “good”: SEC cooled off a market and practices that troubled many. Without, I doubt that as many people would support important work from @TheBKP_Official, @GlobalDigitalFi, @MessariCrypto, @TruSetData on important topics like transparency and codes of conduct.

6/ The (arguably) “bad”: SEC’s approach is chilling legitimate, non-securities innovation. The hype of 2017 arguably outpaced the tech, but now the tech is catching up. Projects are ready to launch tokens that are usable software, but the SEC’s approach remains unclear.

7/ The lack of clarity is scaring off investors and customers. Not just due to potential liability, but also because an inherently consumptive token cannot really operate as a security under US federal law.

8/ The securities laws don’t work for consumptive/use-based products, which is why they haven’t historically applied to those products. (h/t @NYcryptolawyer)

9/ You can't launch a token-powered uber or eBay if the marketplace could only involved accredited investors and operate through regulated broker-dealers or ATSs. But that’s effectively what happens if you apply securities laws to the token that operates those networks.

10/ Right now, the market doesn’t have confidence in the boundaries of the SEC’s approach. It doesn’t understand, e.g., the rules for whether and how a decentralized eBay could ...

11/ (1) raise money from investors, especially where they may want exposure to tokens; (2) sell product to customers; or (3) permit buyers to “resell” a token at some point for a profit.

12/ These need clarity. I think I know where the SEC would draw these lines, but, while that might be enough for a law review article, it’s not enough for investors to risk hundreds of millions of dollars or entrepreneurs to risk their livelihood. The market needs more clarity.

13/ Which brings back to why these state safe harbors are important. They don’t articulate the full boundaries of securities laws, which would be difficult and controversial. Rather, they just provide a few clear, bright-line rules.

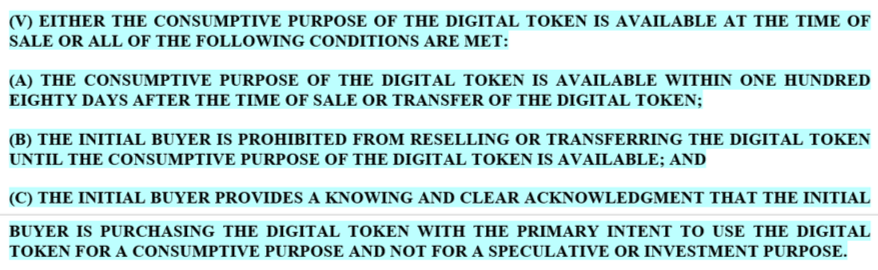

14/ In doing so, they provide clarity that is simultaneously helpful and not too controversial. They articulate a balance of intrinsic and extrinsic factors that are reliably in favor of not applying securities laws to usable, consumptive tokens.

15/ There are many useful points in the state legislation, but here are, in my opinion, a few of the most important clarifying points:

16/ Point #1: You can presell a token without making the token a security. This is consistent with how many businesses today produce and sell products, including, e.g., tickets, teslas, and kickstarter products.

17/ In #CO, here are the factors that, if present, allow a pre-sale of tokens to still qualify for the safe harbor (h/t @propelforward):

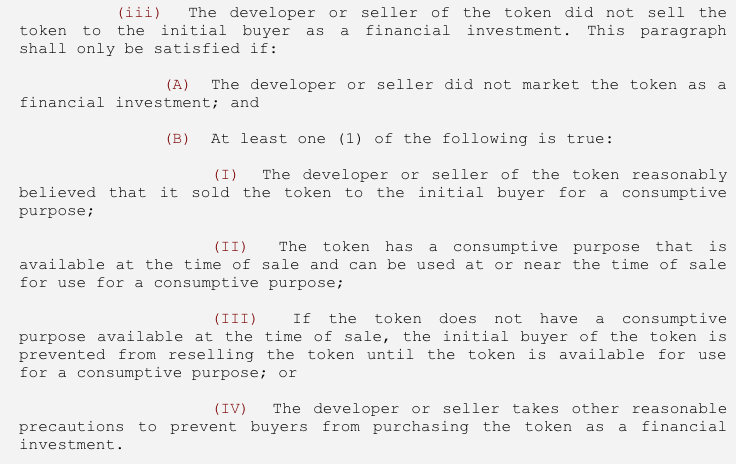

18/ Similarly, in #WY, here are the factors that are needed for a pre-sale to qualify for the safe harbor:

19/ In both jurisdictions, “locking up” presale tokens until they are usable for their consumptive purpose works. This mitigates risk of overly speculative markets before tokens are usable, which seems to be one of the extrinsic characteristics that has concerned the SEC.

20/ Point #2: The safe harbors also effectively recognize that profit-seeking resellers can eventually participate in markets for tokens without transforming them into securities. Again, this is true in markets for other consumptive products, and I think it makes sense here.

21/ Point #3: The safe harbors don’t try to measure the quality or completeness of software. They keep it simple and ask when the token is usable for a consumptive purpose. I think this is significantly better than having the law turn on whether the token is “fully functional.”

22/ I don’t know what “fully functional” means, but I know (1) software is iterative and changes a lot; and (2) I don’t think we’ll benefit from having securities regulators decide when usable software is “fully functional” or just “partially functional.”

23/ Point #4: The safe harbors don’t turn on whether a project or token is “sufficiently decentralized.” Some projects may end up decentralized like bitcoin and ethereum, which is great. And for them, the SEC is correct that securities laws don’t make sense.

24/ But some projects won’t, and we shouldn’t inadvertently force them to achieve or (frankly) fake decentralization . . .

25/ … because doing so will be (1) bad for technology, bc products suffer if they “decentralize” only to launch w/o securities laws (many projects can’t launch if securities laws apply to a usable token); and (2) investors and consumers, bc it may lead to less accountability.

26/ I hope other states follow the lead of #WY and #CO (cc: @CaitlinLong_). And hopefully the SEC carefully considers and acknowledges these approaches in their forthcoming guidance (cc: @HesterPeirce).

27/ Ultimately, clarity like this will help innovators comply with securities laws while still launching networks powered by usable software tokens. All parties involved will know they can buy, sell and use the tokens without worrying about running afoul of securities laws.