,

18 tweets,

6 min read

Read on Twitter

I head a closed cooperative society that in the last 3 years have given out over N100m in loans at 0% interest rate. Yes you heard right - 0% interest rate. The maximum members pay is a 10% flat fee irrespective of the tenure of their loans which can extend to 24 months or more

As a treasurer, I've listened to the concerns of SMEs about the cost of finance. Banks typically lend to retail at above 2.1% per mth (25% p.a), while micro finance banks lend at between 3.5 - 5% per mth (42 - 60%p.a). A friend told me he borrowed from a loan shark at 10% per mth

The reality is that there are not many options of cheap sources of micro credit to individuals & small businesses. But one option stands out and that is Cooperative Society. With the CS, members are able to pull funds and decide the terms & condition for accessing or investing it

Cooperative provide the unique platform to do many things. For instance, apart from our 0% lending rate, we are able to invest members funds in T-Bills, Bonds and other investment options. We are also able to assist members with special loans for emergencies & paying school fees.

We also assist members in purchase loans paid directly to the vendors and at the End of Year, we divide the surplus by two, pay one half as dividends to members, one quarter is kept in reserves and the remaining is used to cover statutory fees to the State and AGM expenses.

The opportunities are immense. In 2017 our Cooperative signed up with a Fintech coy that was pioneering Cooperative Banking in Nigeria. The org called @RibyFinance, introduced us to its web app that allowed us migrate data from a manual (passbook) record system to an online one.

The impact of this was instant. It gave members the power of visibility of their contribution & loan data. The cooperative is like a bank. They save, they lend and keep records. So If you can view my bank account online, I shd be able to view your cooperative account online also.

@RibyFinance gave us that platform and within a year, we moved from not just contributions and repayment visibility on the platform, to loan administration process where members can apply for loans right from the platform without the need to physically see anyone.

They could start and finish the process (get their loan credit alert) Without seeing anyone or leaving their desk. It was that good.

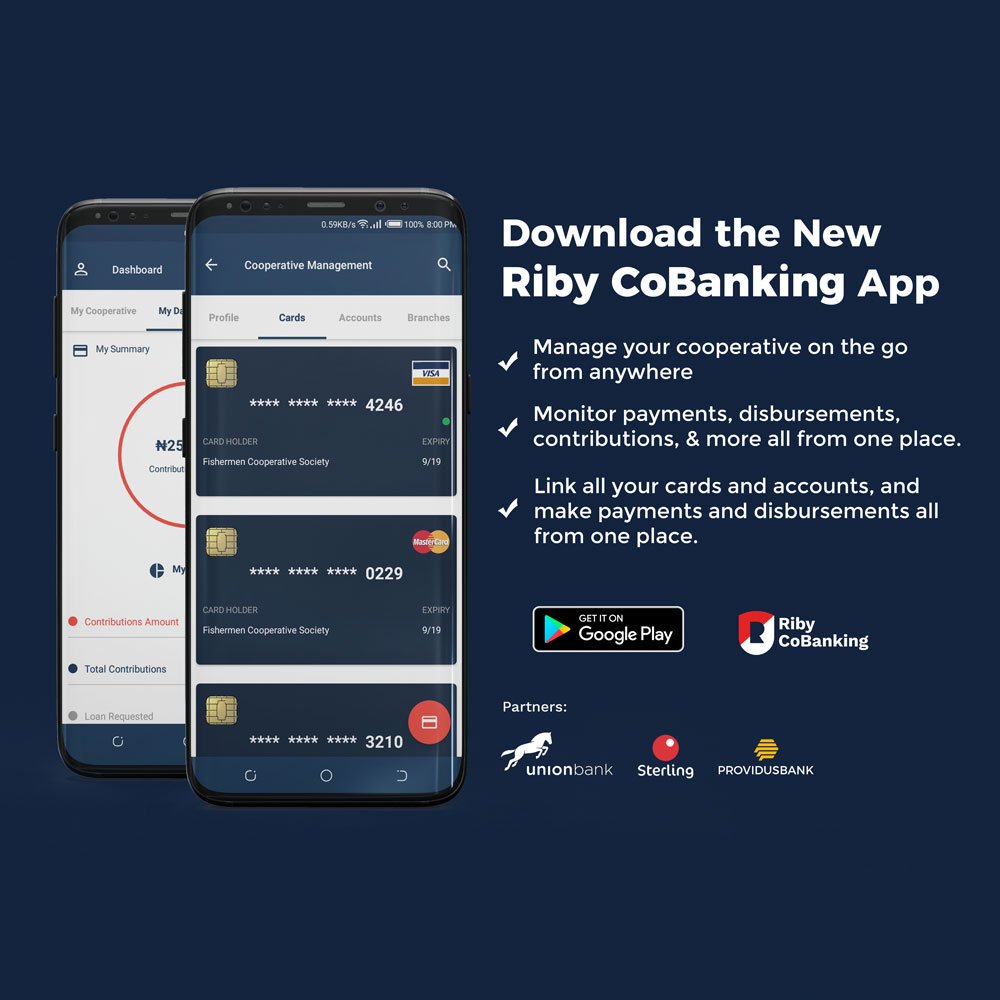

In Feb 2019, Riby upgraded the version they gave us called "Riby for

Cooperative", and launched a new version called the Riby Co-Banking App.

In Feb 2019, Riby upgraded the version they gave us called "Riby for

Cooperative", and launched a new version called the Riby Co-Banking App.

If "Riby for Cooperative" was great, Riby Co-Banking was revolutionary. It was Co-Banking on steroids. First, it was no longer a web app, but also a mobile app. With improved security features, members cld download the app on their device, sign in & check their data from anywhere

They could also apply for loans on the go or respond to request as a guarantor of other loans. It didn't end there. With the new version, they're able to transfer savings direct from their bank a/c to the coop account without the need of going to the bank and (wait for this)...

...the platform comes with the opportunity to participate in investment options opened up. So members can decide to invest directly in select investment windows created by the cooperative in conjunction with different providers. They have the option of splitting their savings...

...between what goes to their cooperative contribution and what can go towards investment. And did I mention the brilliant admin end of the app and the fantastic 24 hours online support that includes phone, emails, live chats and WhatsApp by the incredibly motivated Riby team. 👍

What is the result of all these developments? Our membership have grown by over 60% from before we started using Riby and now. It turns out that transparency and accountability pays off. People are more inclined to participate when the process is transparent and inclusive.

A lot has been said lately about "Financial Inclusion". I'm convinced that the cooperative system is an important enabler of the financial inclusion conversation. Imagine what we can do with it?

- Micro Credit that competes with bank credit,

- New market for insurance products.

- Micro Credit that competes with bank credit,

- New market for insurance products.

- E-Payment utilisation by connecting Coop Society Accounts to the financial E-commerce eco-system.

This is why I'm proud to recommend Riby Co-Banking App to already existing cooperatives & those looking to form one. I don't say this for the sake of it, I say because I use it.

This is why I'm proud to recommend Riby Co-Banking App to already existing cooperatives & those looking to form one. I don't say this for the sake of it, I say because I use it.

I will be speaking at the first Riby Cooperative Conference scheduled for this Wednesday at the Recency Hall, Alausa. The conference is opened to the public and registration closes at midnight. If you want to scale up your Cooperative, this is one conference you MUST attend.

To register for the conference, you can click on this link. See you there on Wednesday.

eventbrite.com/e/riby-coopera…

eventbrite.com/e/riby-coopera…