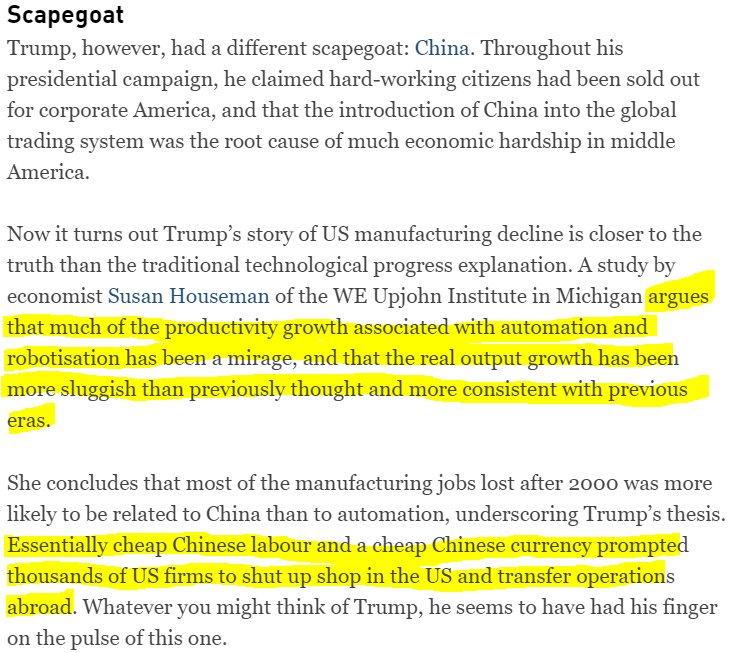

,

14 tweets,

4 min read

Read on Twitter

I suspect the foundations for Argentina's crisis were laid back in 2017, when a jump in imports pushed the current account deficit toward 5% - high for a country with a small export base.

But recent debt management choices helped create the conditions for a perfect storm

1/x

But recent debt management choices helped create the conditions for a perfect storm

1/x

Earlier this year, Argentina shortened the maturity of its debt issuance, creating a bunching of maturities ahead of the election ....

Understandable given the cost of issuance, but risky ...

Understandable given the cost of issuance, but risky ...

The IMF was well aware of the risk -- this is what they rote in their last report on Argentina. Pretty much describes what happened

3/x

3/x

The IMF program was also based on an increase in Argentina's fx debt. That's intrinsic to borrowing from the IMF. But it was a reaction to the problems the central bank had rolling over LEBACs (peso paper) back in 2018. The LEBACs had prompted Argentina to go to the IMF.

4/x

4/x

This chart - showing Argetina's real effective exchange rate - bothered me from the start. The peso fell when Macri moved off the peg at the start of his term, but quickly appreciated. And it has been strong relative to history ...

The fine print of the IMF program documentation has always shown a large vulnerability to a big move in the peso. This is public debt to GDP. The purple line shows the impact of an exchange rate shock.

7/x

7/x

The impact of a large move also shows up in the Fund's assessment of external debt sustainability (which unfortunately in my view has been downgraded a bit relative to assessment of fiscal debt sustainability)

8/x

8/x

The chart above basically shows that an exchange rate shock has a bigger impact than a shock to growth and to the interest rate. That's what happens when your debt is denominated in fx.

9/x

9/x

Argentina's problem is that because it has a small export sector, it takes a really big move in the real exchange rate to move the trade balance around -- and that big real exchange rate move devastates its debt sustainability.

10/x

10/x

As Paul Krugman argued earlier today, this is an old story (see original sin, liability dollarization, debt intolerance).

11/x

11/x

What's different -- at least compared to 2000 and 2001 -- is that this has played out in the context of a (managed) float. And Argentina has displayed a lot of inflation inertia -- so much so that the IMF wanted a stronger RER to help bring inflation down.

12/x

12/x

The IMF was encouraging Argentina not to build reserves and fight fx strength (back when that was an issue) for this reason. (a stronger RER also helped with the Fund's debt sustainability calculation)

imf.org/en/Publication…

13/x

imf.org/en/Publication…

13/x

Macri was never able to get out of this trap - Argentina's government appeared not to be that indebted when he took office, but that was a bit of an illusion. Argentina didn't really have the capacity to bear more fx debt!

14/x

14/x

The silver lining, if there is one - Argentina actually has quite a bit of debt coming due over the next year and a half.

Which means a reprofiling (or more likely a restructuring) does in theory provide a bit of policy space ...

15/15

Which means a reprofiling (or more likely a restructuring) does in theory provide a bit of policy space ...

15/15