,

16 tweets,

10 min read

Read on Twitter

What in the world is going on in the bond market? Here's a 3-minute thread on where it was, where it is now, and where it’s going. And why it’s important to our economic future.

By @BChappatta ⬇️

By @BChappatta ⬇️

@BChappatta The $16 trillion U.S. Treasury market is the biggest, most-liquid bond market on the planet and is one of the first places investors turn in times of trouble.

It’s virtually impossible for the U.S. to default on its debt, as it controls the dollar, the world’s reserve currency.

It’s virtually impossible for the U.S. to default on its debt, as it controls the dollar, the world’s reserve currency.

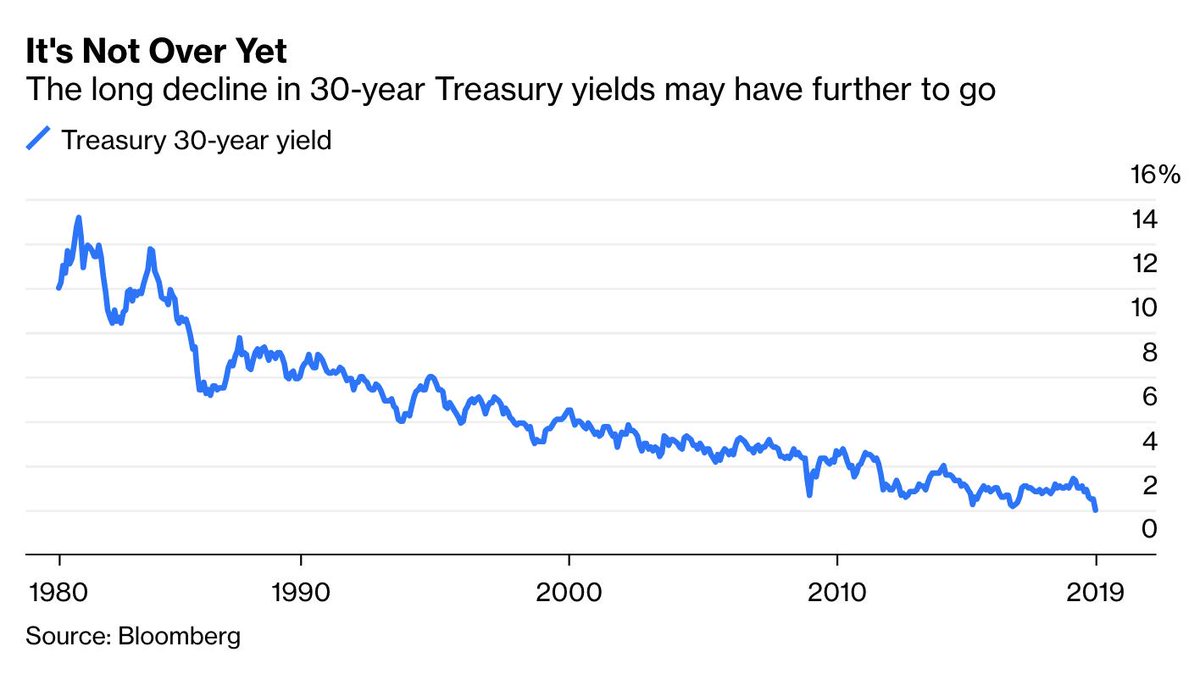

@BChappatta Treasuries have been in a three-decade bull market. It peaked in July 2016.

Bonds “rally” when yields fall and prices rise. The 10-year Treasury yield, a global borrowing benchmark, was almost 16% in 1981. In July 2016, it fell as low as 1.32%. bloom.bg/2zYf61s

Bonds “rally” when yields fall and prices rise. The 10-year Treasury yield, a global borrowing benchmark, was almost 16% in 1981. In July 2016, it fell as low as 1.32%. bloom.bg/2zYf61s

@BChappatta Treasuries returned an average of 7.5% a year since that record high in 1981.

The S&P 500 Index returned an average of 11.7% a year, albeit with considerably more volatility.

The S&P 500 Index returned an average of 11.7% a year, albeit with considerably more volatility.

@BChappatta Yields on Treasuries are now back near those July 2016 lows. The 10-year yield fell to as low as 1.43% this week.

Remember, the *all-time* low is 1.32%. So yes, we are close.

Remember, the *all-time* low is 1.32%. So yes, we are close.

@BChappatta This is happening now for a number of reasons. Most of them boil down to trade disputes.

Trade wars threaten global growth. If growth slows, companies are less profitable, and not worth as much. Therefore, stocks decline. When that happens, investors rush to Treasuries.

Trade wars threaten global growth. If growth slows, companies are less profitable, and not worth as much. Therefore, stocks decline. When that happens, investors rush to Treasuries.

@BChappatta Rapidly falling Treasury yields, in turn, catch the attention of officials at the Federal Reserve. The Fed can effectively control rates on short-term debt because it sets the fed funds rate itself.

It has less control over longer-term bonds.

It has less control over longer-term bonds.

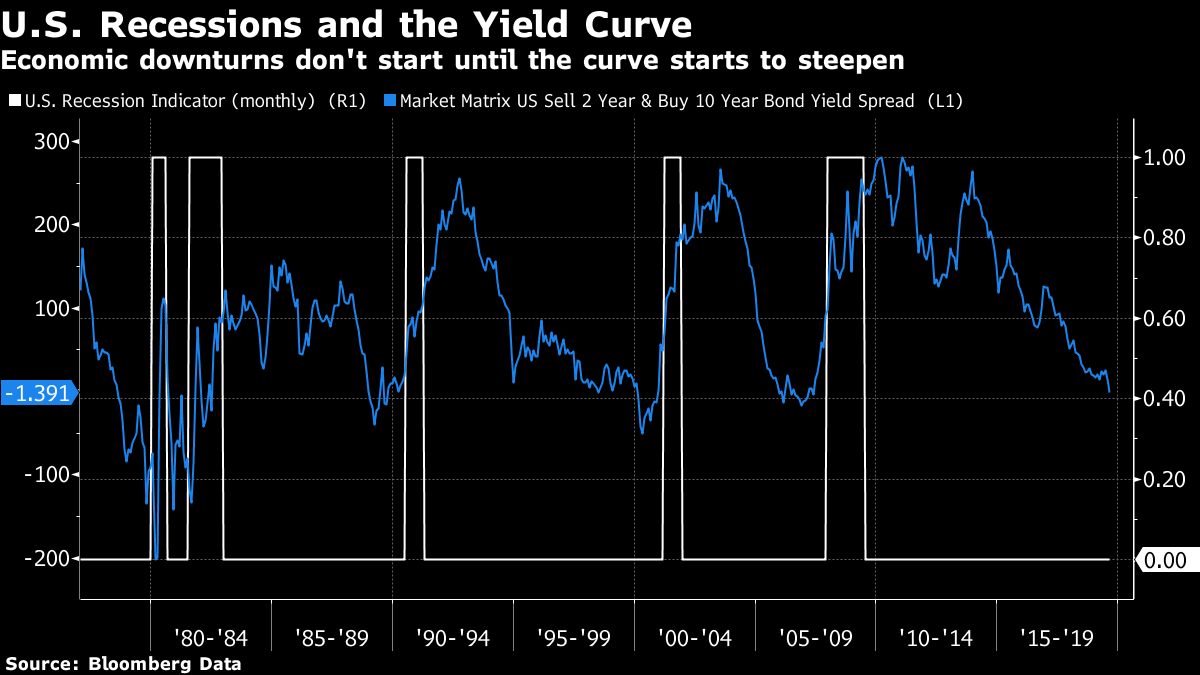

@BChappatta It’s also why the “inverted yield curve” matters. It means 10-year yields, which the Fed can't control, are *lower* than the short-term yields the Fed controls.

That usually portends recession. At the very least, it’s a sign that the Fed should be lowering rates more quickly.

That usually portends recession. At the very least, it’s a sign that the Fed should be lowering rates more quickly.

@BChappatta Investors expect the Fed to keep cutting interest rates because of ongoing trade skirmishes. Some even expect the short-term rate to fall to zero before long.

Similar rates are already below zero elsewhere in the world, like Europe and Japan. bloom.bg/2zYwtiQ

Similar rates are already below zero elsewhere in the world, like Europe and Japan. bloom.bg/2zYwtiQ

@BChappatta This is why @bopinion columnist @agaryshilling says Treasury bond yields have yet to see a bottom bloom.bg/2zWyHPz

@BChappatta @agaryshilling “Don’t worry about the paltry yields. I’ve never bought bonds for yield and couldn’t care less what it is, as long as it’s going down and, as a result, Treasury prices are rising.”

This is a rather uncommon view for fixed-income investors. But it has paid off over 30+ years.

This is a rather uncommon view for fixed-income investors. But it has paid off over 30+ years.

@BChappatta @agaryshilling Other investors appear to be waiting for a backup in yields to lock in a somewhat higher return. They want to “buy the dip” in bonds.

On Thursday, 10-year yields had the biggest intraday increase since November 2016, but few actually stepped up. bloom.bg/2zTUwPQ

On Thursday, 10-year yields had the biggest intraday increase since November 2016, but few actually stepped up. bloom.bg/2zTUwPQ

@BChappatta @agaryshilling Lower-for-longer bond yields won’t be going away anytime soon.

That’s good news for borrowers – U.S. investment-grade companies issued a record $74 billion in debt this week – but makes it challenging for savers to earn any steady income on investments. bloom.bg/2zZcqR6

That’s good news for borrowers – U.S. investment-grade companies issued a record $74 billion in debt this week – but makes it challenging for savers to earn any steady income on investments. bloom.bg/2zZcqR6

@BChappatta @agaryshilling Another @bopinion columnist, Jim Bianco, even goes so far as to say that negative rates could ultimately threaten the financial system bloom.bg/2zTVJGS

@BChappatta @agaryshilling The general consensus is that monetary policy has its limits. Zero (or negative) interest rates can only do so much. Will people really spend more if short-term rates are 0% instead of 1%?

Fiscal spending on infrastructure could be the next frontier. bloom.bg/2LyZzug

Fiscal spending on infrastructure could be the next frontier. bloom.bg/2LyZzug

@BChappatta @agaryshilling Simply put, the global bond market is raising a lot of tough questions right now for investors, economists, central bankers and government officials.

Stick with @bopinion columnists as we sort out the answers.

Stick with @bopinion columnists as we sort out the answers.