Heading in to our first session at the 2020 Financial Reaearch Association conference; live-tweet starts now. (If you’re not interested, please 48-hour mute hashtag #FRA20 ). Program with paper links is here: fraconference.com/current-progra…

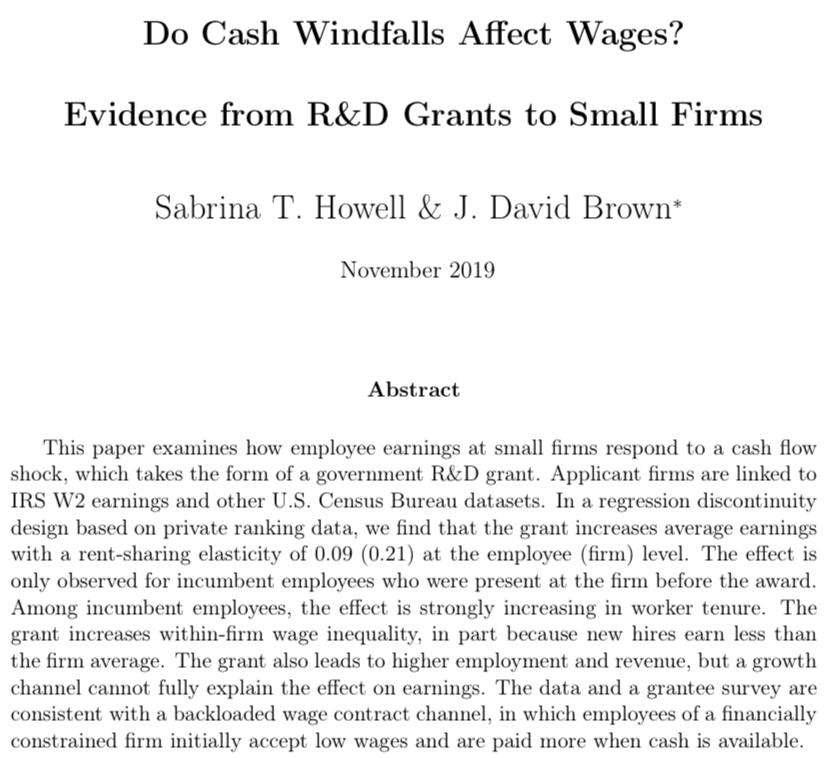

First paper is on cash windfalls and wages (by Sabrina Howell and J. David Brown; presented by Cesare Fracassi).

Lots of papers ask what happens when firms get cash windfalls. Paper uses SBA-provided Small Business Innovation Research Grants (~$2.2B/yr). #FRA20

Lots of papers ask what happens when firms get cash windfalls. Paper uses SBA-provided Small Business Innovation Research Grants (~$2.2B/yr). #FRA20

Competitive grants to SMBs:

- $150K for proof-of-concept

- ≤$1M followup

Applying takes 1–2 months of FTE work, and program officials rank applications.

Data: 270 competitions; 4,300 applications; 800 winners. (~3 of 16 win each competition). Link to IRS W2 and LBD. #FRA20

- $150K for proof-of-concept

- ≤$1M followup

Applying takes 1–2 months of FTE work, and program officials rank applications.

Data: 270 competitions; 4,300 applications; 800 winners. (~3 of 16 win each competition). Link to IRS W2 and LBD. #FRA20

Why might grants affect wages?

✔︎ 1. Financial constraints (implicit contract to pay below-market wages until constraint relaxed)

✘ 2. Productivity growth

✘ 3. Bargaining

✘ 4. Incentive contracting (e.g., win bonus)

✘ 5. Agency issues

✘ 6–8. [Other] #FRA20

✔︎ 1. Financial constraints (implicit contract to pay below-market wages until constraint relaxed)

✘ 2. Productivity growth

✘ 3. Bargaining

✘ 4. Incentive contracting (e.g., win bonus)

✘ 5. Agency issues

✘ 6–8. [Other] #FRA20

Builds on SH’s 2017 AER aeaweb.org/articles?id=10… . Approach basically diff-in-RDD (of course CF has some suggestions).

Winning firms

- Incease wages

- Basically only for incumbent employees (i.e., at firm pre-grant)

- Roughly equal for higher- and lower-paid employees

#FRA20

Winning firms

- Incease wages

- Basically only for incumbent employees (i.e., at firm pre-grant)

- Roughly equal for higher- and lower-paid employees

#FRA20

Cesare asks:

- Is this really a cash windfall?

- (Strong) incentive to apply for Phase II if successful in Phase I?

- Magnitudes? (Looks like $150K grant raises winners’ employees’ wages ~3% 🤷♂️)

- More detail on apparent implicit back-loading contracts? #FRA20

- Is this really a cash windfall?

- (Strong) incentive to apply for Phase II if successful in Phase I?

- Magnitudes? (Looks like $150K grant raises winners’ employees’ wages ~3% 🤷♂️)

- More detail on apparent implicit back-loading contracts? #FRA20

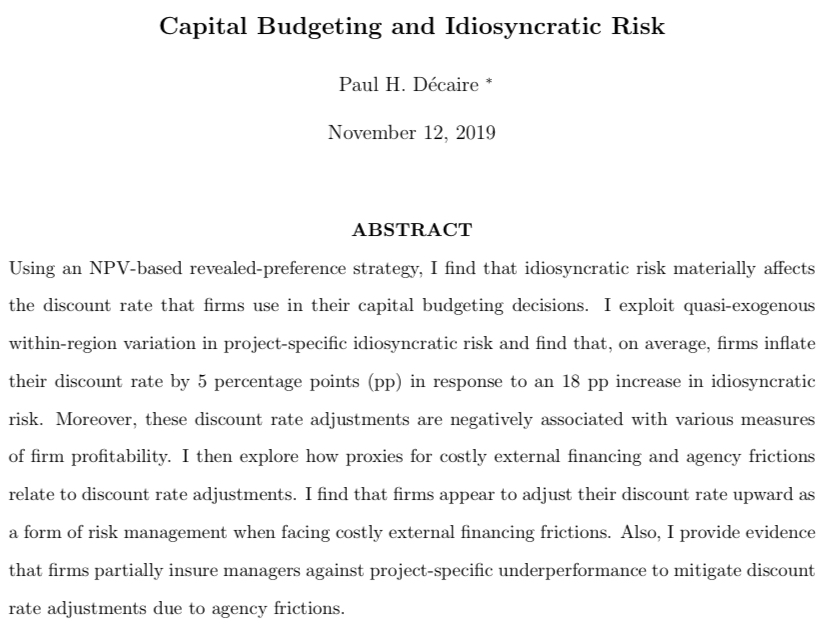

PAPER 2. James Weston presents 🚨Wharton JMC🚨 Paul Décaire’s “Capital Budgeting and Idiosyncratic Risk.”

paulhdecaire.com

Do managers pad their discount rates? YES

Is it a big deal? NOT CLEAR

Cost of capital = Rf + 𝛽×MRP + stuff?

#FRA20

paulhdecaire.com

Do managers pad their discount rates? YES

Is it a big deal? NOT CLEAR

Cost of capital = Rf + 𝛽×MRP + stuff?

#FRA20

Paper looks at 115K vertical gas wells with (largely) exogenous variation in (mostly) idiosyncratic risk. For each project, measure

1. NPV (⇒ bounds on R depending whether project done or not)

2. Idiosyncratic risk #FRA20

1. NPV (⇒ bounds on R depending whether project done or not)

2. Idiosyncratic risk #FRA20

PD finds

1. Firms inflate discount rates ~7.9% (not percentage points; 12% → 13%)

2. Firms that “pad” are worse

3. Stronger for firms where it’s hard to raise money

4. Padding is related to idiosyncratic risk (though JW asks whether measure could be capturing skewness) #FRA20

1. Firms inflate discount rates ~7.9% (not percentage points; 12% → 13%)

2. Firms that “pad” are worse

3. Stronger for firms where it’s hard to raise money

4. Padding is related to idiosyncratic risk (though JW asks whether measure could be capturing skewness) #FRA20

Note that Paul is 🚨on the job market🚨 paulhdecaire.com , and in addition to this very nice paper, has a great @RevOfFinStudies paper with Wharton’s Erik Gilje and @BabsonFinance’s @jerometaillard.

#FRA20

#FRA20

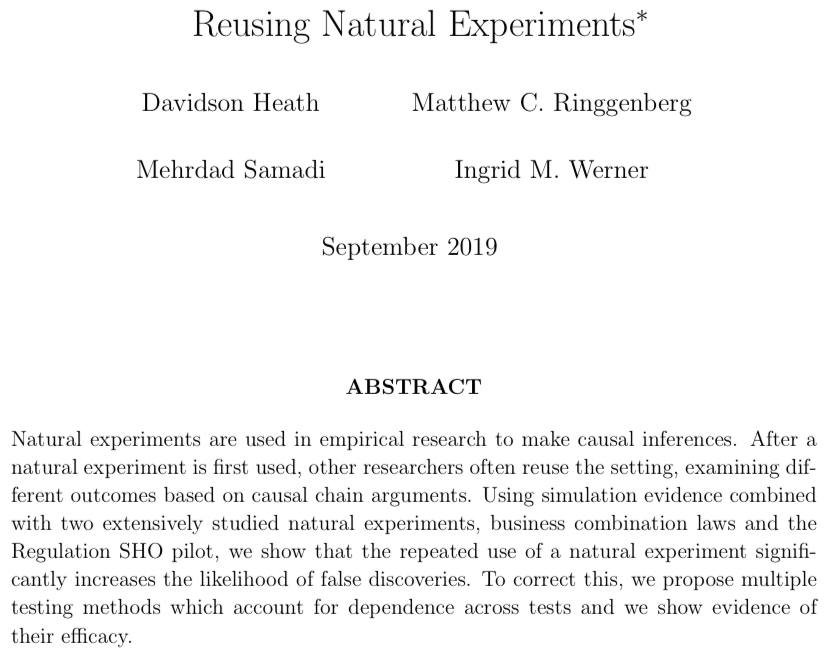

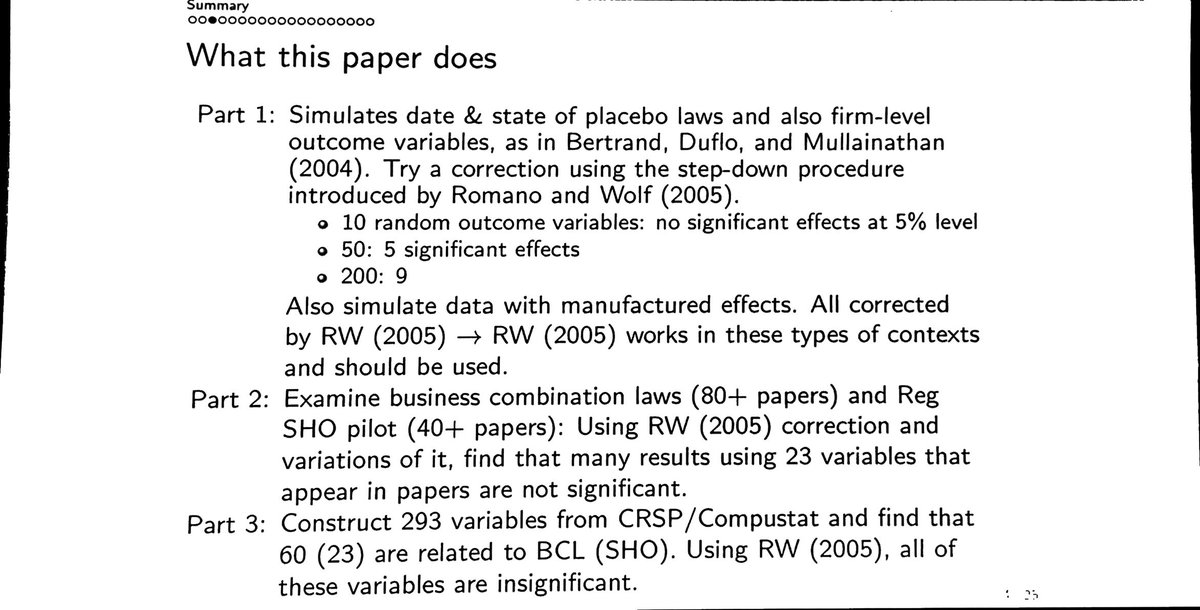

PAPER 3: @davidsontheath, Samadi, Ringgenberg, and Werner’s “Reusing Natural Experiments” is presented by Sophie Shive at @NDBusiness.

Excited to see this presented; I learned that “My relevance condition is your exclusion restrictino violation.” #FRA20

Excited to see this presented; I learned that “My relevance condition is your exclusion restrictino violation.” #FRA20

Issue is lots of papers using same natural experiments to examine different outcomes. HSRW show that Romano and Wolf (Econometrica 2005 onlinelibrary.wiley.com/doi/pdf/10.111…) correction works in simulated data. #FRA20

Considers actual published finance papers (on widely applied Regulation SHO and BC law experiments).

Considers

- RW (2005) random ordering, and then refinements where

- Outcomes are ordered by publication date or by

- Variables’ apparent causal chain #FRA20

Considers

- RW (2005) random ordering, and then refinements where

- Outcomes are ordered by publication date or by

- Variables’ apparent causal chain #FRA20

Paper’s prescriptions include:

1. Verify relevance and exclusion restrictions of main effects before examining higher order effects

2. Caution on reuse of natural experiments

3. Conduct multiple-comparison corrections using earlier papers in literature #FRA20

1. Verify relevance and exclusion restrictions of main effects before examining higher order effects

2. Caution on reuse of natural experiments

3. Conduct multiple-comparison corrections using earlier papers in literature #FRA20

Shive notes

- Goal is *not* replication existing papers (uses standardized data); goal is methodological

- Appropriate corrections differ for reuse across different outcomes in same data set vs. same experiment but different contexts

- [Some methodological suggestions]

#FRA20

- Goal is *not* replication existing papers (uses standardized data); goal is methodological

- Appropriate corrections differ for reuse across different outcomes in same data set vs. same experiment but different contexts

- [Some methodological suggestions]

#FRA20

.@davidsontheath: “We’re not trying to start a fight.” ☮️

@ctrzcinka: “You guys *should* start a fight. The first, fundamental rule of financial econometrics is that everyone is wrong.” 🥊 #FRA20

@ctrzcinka: “You guys *should* start a fight. The first, fundamental rule of financial econometrics is that everyone is wrong.” 🥊 #FRA20

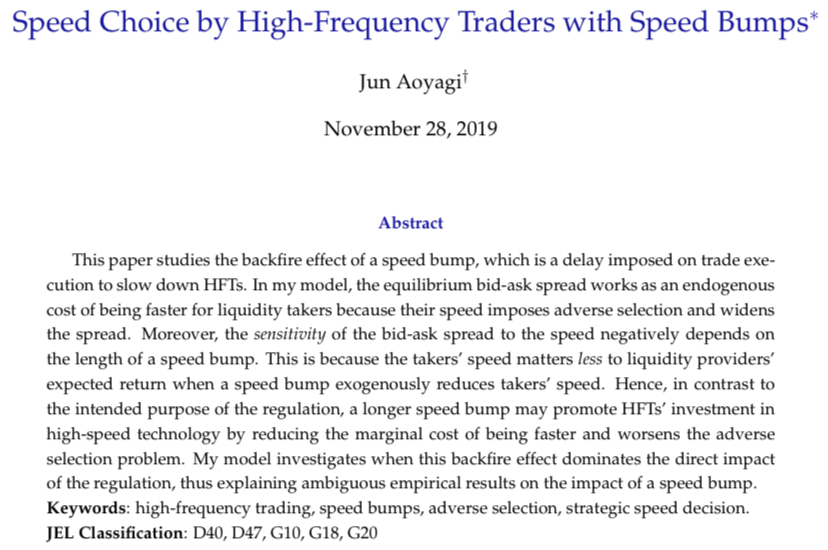

PAPER 4: Ohad Karan presents Jun Aoyagi’s “Speed Choice by High-Frequency Traders With Speed Bumps.”

Note Jun is a pre-market Econ PhD student at Berkeley, with (another paper) solo-authored R&R at JET. sites.google.com/site/junaoyagi…

#FRA20

Note Jun is a pre-market Econ PhD student at Berkeley, with (another paper) solo-authored R&R at JET. sites.google.com/site/junaoyagi…

#FRA20

Microstructure theory of sniping: Standing limit orders are essentially options, and are subject to adverse selection. One solution is to impose “speed bumps” (intentional delays in order execution).

How do speed bumps affect bid-ask spreads when HFT speed is endogenous? #FRA20

How do speed bumps affect bid-ask spreads when HFT speed is endogenous? #FRA20

(Just spent the coffee break hanging out with @julian_finecon; I think we’re as ready as we’re going to be.) #FRA20

HFTs choose speed endogenously, trading off that trading faster:

➕ Increases probability of successfully sniping

➖ Increases bid-ask spread, which reduces profit from sniping

➖ Has an (exogenous)

Solving the model...

⇒ Optimal speed is INCREASING in speed bump #FRA20

➕ Increases probability of successfully sniping

➖ Increases bid-ask spread, which reduces profit from sniping

➖ Has an (exogenous)

Solving the model...

⇒ Optimal speed is INCREASING in speed bump #FRA20

Model #2 (extension): Multiple HFTs competing as both market-makers (liquidity providers) and aspiring snipers (liquidity takers).

Model gives strategic complementarity.

Unlike benchmark model, longer speed bump widens spread. #FRA20

Model gives strategic complementarity.

Unlike benchmark model, longer speed bump widens spread. #FRA20

Model #3 (extension): Multiple HFTs and exogenous cost of speed (e.g., investment in tech and infrastrucure).

Introduces strategic substitution (similar to existing models) depending on parameters. #FRA20

Introduces strategic substitution (similar to existing models) depending on parameters. #FRA20

Kadan comments:

1. Implications. Welfare (liquidity traders vs. mkt makers vs. snipers)?

2. *Baseline* model: Speed bumps are irrelevent in equilibrium (speed, Pr[sniping], etc)! Per envelope theorem

3. BUT in competitive model, speed bumps DO matter (eg increased spreads) #FRA20

1. Implications. Welfare (liquidity traders vs. mkt makers vs. snipers)?

2. *Baseline* model: Speed bumps are irrelevent in equilibrium (speed, Pr[sniping], etc)! Per envelope theorem

3. BUT in competitive model, speed bumps DO matter (eg increased spreads) #FRA20

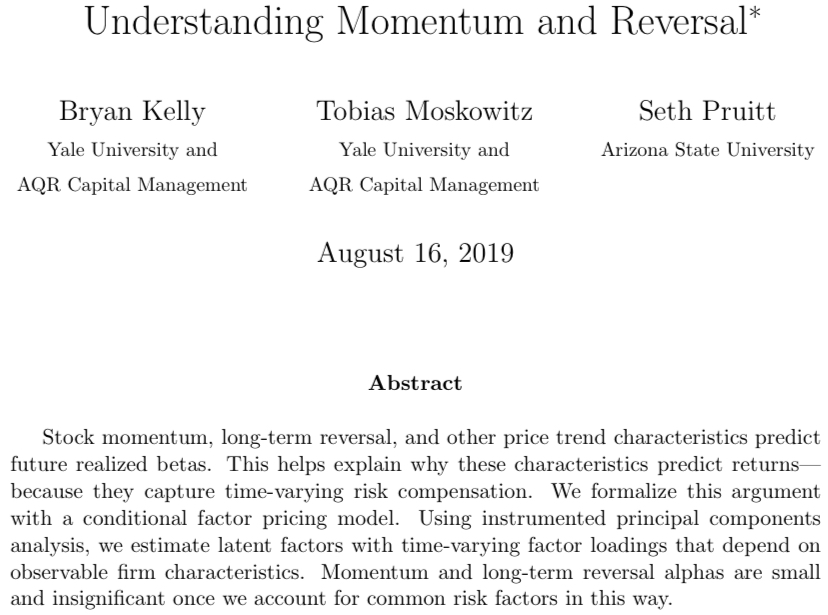

PAPER 5 (last of the day): Brian Kelly, Toby Moskowitz, and (my @WPCareySchool colleague and good friend) Seth Pruitt’s “Understanding Momentum and Reversal,” presented by Andrei Goncalves. #FRA20

Fama: “[Momentum] could be explained by risk, but if it’s risk, it changes much too quickly for me to capture it in any asset-pricing model.”

Mmntum seems to predict 𝛽. We can model link between 𝛽s and chars in conditional factor model (as in authors’ earlier IPCA work) #FRA20

Mmntum seems to predict 𝛽. We can model link between 𝛽s and chars in conditional factor model (as in authors’ earlier IPCA work) #FRA20

Conclusion: “Momentum and long-term reversals… [are] explained by conditional betas in a no-arbitrage factor model”

[Andrei notes that “Factor 3” from authors’ IPCA paper is ~0.5 correlated with momentum.] #FRA20

[Andrei notes that “Factor 3” from authors’ IPCA paper is ~0.5 correlated with momentum.] #FRA20

Andrei:

Glass half empty: We learned that arbitrageurs know about momentum so it is not a near-arbitrage opportunity.

Glass half full: We learned why momentum did not (and likely will not) disappear despite arbitrageurs knowing about it. #FRA20

Glass half empty: We learned that arbitrageurs know about momentum so it is not a near-arbitrage opportunity.

Glass half full: We learned why momentum did not (and likely will not) disappear despite arbitrageurs knowing about it. #FRA20

And… we’re back for the second day of #FRA20! If you’d like to catch up on yesterday’s live-tweet thread, it started here:

Made me think of this recently-replayed episode from @deathsexmoney (one of my favorite podcasts🎙) interviewing @Uber drivers about why they started working there. (I’m sorry… selling independent contracting services using their platform 😉) #FRA20

Gig economy curtail individuals’ reliance following job separations on (1) UI and (2) consumer credit [utilization and delinquencies].

Is this labor demand, or an “insurance”-like option? #FRA20

Is this labor demand, or an “insurance”-like option? #FRA20

Triple-diff using Equifax/credit bureau data

❶×❷ UberX staggered rollout across 163 CBSAs

❸ Car owners vs. non-owners

Isaac suggests complementarity with approach/results from Emilie Jackson’s JMP web.stanford.edu/~emilyj91/ #FRA20

❶×❷ UberX staggered rollout across 163 CBSAs

❸ Car owners vs. non-owners

Isaac suggests complementarity with approach/results from Emilie Jackson’s JMP web.stanford.edu/~emilyj91/ #FRA20

I’m curious: How much of this is really labor income, and how much is a mechanism for just cashing out automotive equity. Might be interesting to consider heterogeneity across states where e.g., auto title loans are more/less available. #FRA20

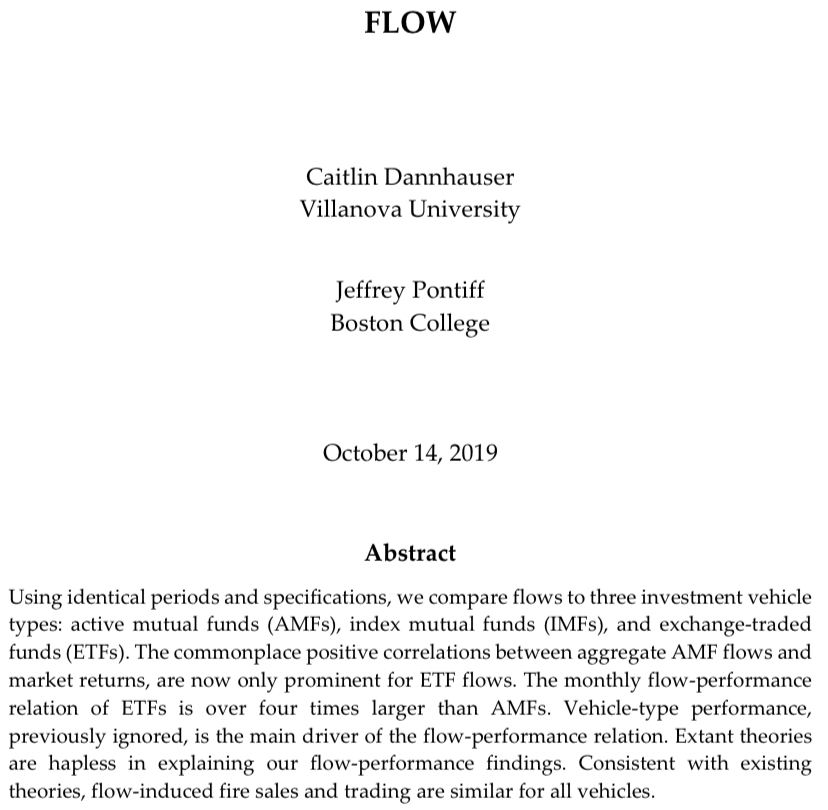

PAPER 7: @cdilldann and Jeff Pontiff’s “Flow,” presented by @csialm. One cool thing about this paper is we saw it in “early ideas” form at last year’s #FRA2018. #FRA20

Includes replications of large literature looking at predictors of fund flows (percentage change in AUM after taking out effect of returns) for aggregate active mutual funds, index funds, and ETFs; and individual funds by type (cf. Berk and Green 2004). #FRA20

(Why did it take me two days to realize that for some reason I set this thread hashtag for next year?)

#NotQuite2020Yet #FRA20

#NotQuite2020Yet #FRA20

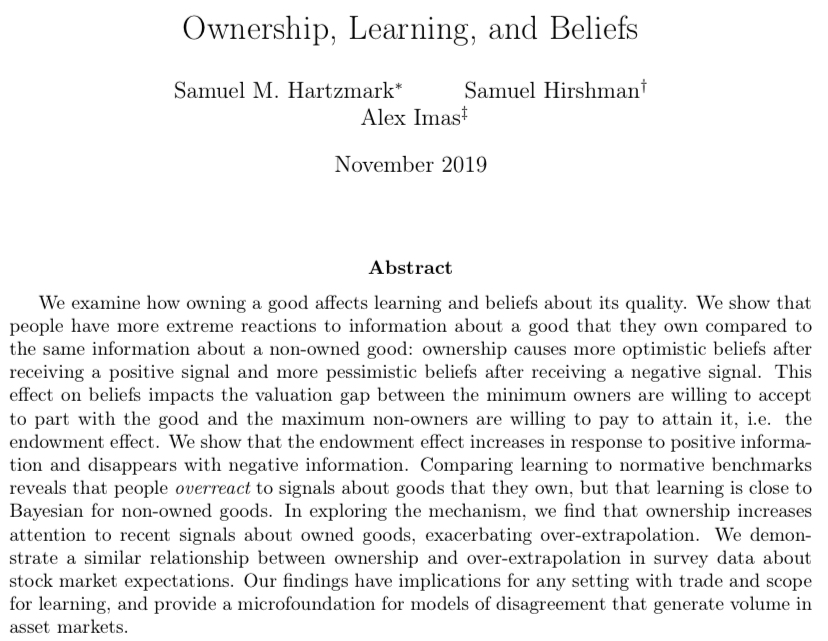

PAPER 8 (last before the “early ideas” session) is Gennaro Bernile presenting “Ownership, Learning, and Beliefs” by @SamHartzmark @HirshmanSam and @alexoimas.

SH did a nice thread on this a few months ago: #FRA20

SH did a nice thread on this a few months ago: #FRA20

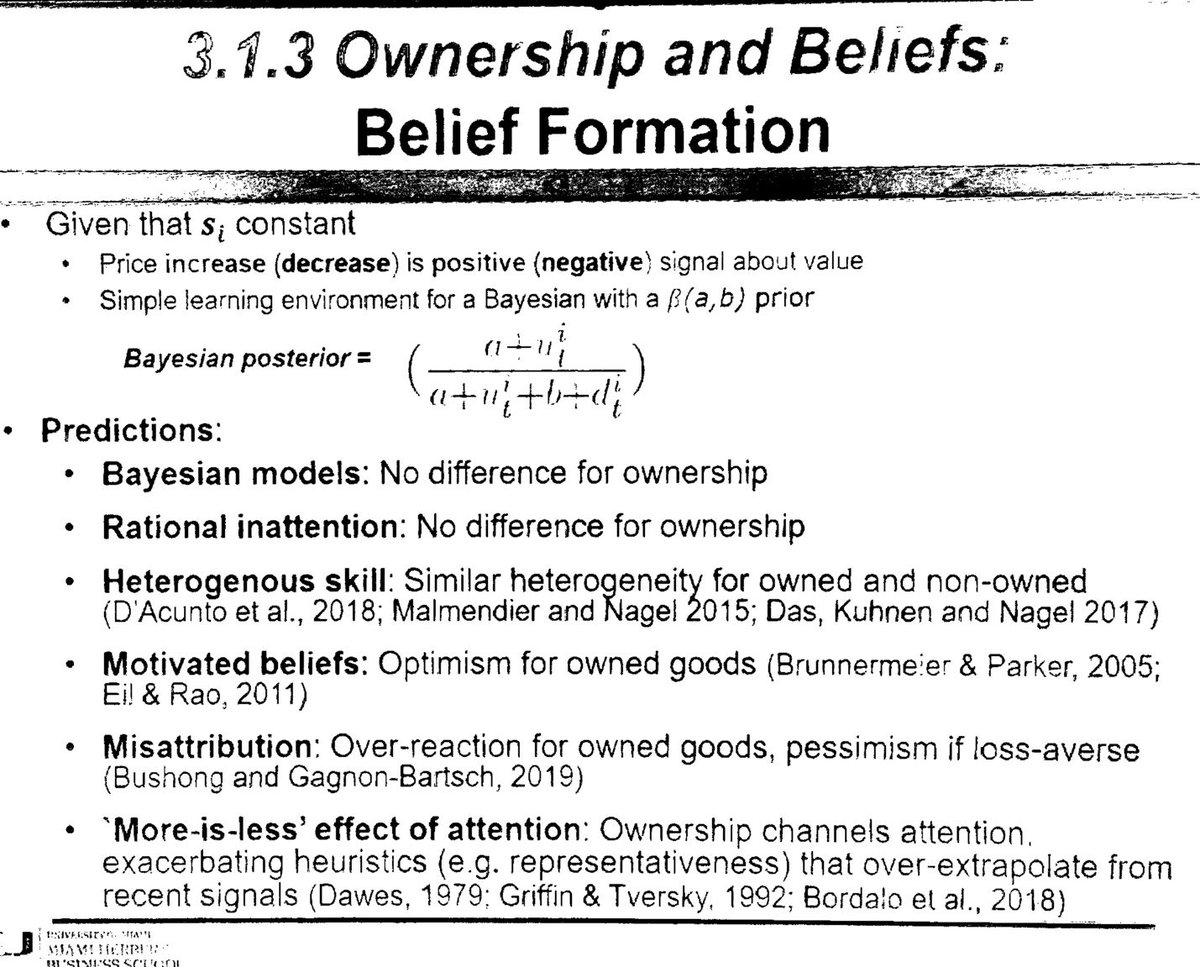

Q: Does ownership systematically affect beliefs about “quality” of what is owned?

Difficult to address without experiments (how to separate preferences from beliefs?)

GB characterizes as “first paper to look at endowment effect’s dynamics and cleanly tie EE to beliefs”👍 #FRA20

Difficult to address without experiments (how to separate preferences from beliefs?)

GB characterizes as “first paper to look at endowment effect’s dynamics and cleanly tie EE to beliefs”👍 #FRA20

Find

- Ownership leads to overreaction to informational signals (first paper looking at EE’s dynamics)

- Learning is close to Bayesian for non-owners

- Driven by attention: “Attention + Incorrect Mental Model = BAD”

- Survey evidence consistent with experiments and theory #FRA20

- Ownership leads to overreaction to informational signals (first paper looking at EE’s dynamics)

- Learning is close to Bayesian for non-owners

- Driven by attention: “Attention + Incorrect Mental Model = BAD”

- Survey evidence consistent with experiments and theory #FRA20

Experimental setup #1: Price of each of six goods evolves every period ∈ {-5%, +6%} with some fixed, unknown probability for each good.

Participants pick three of six goods, and then we see how beliefs evolve as function of (1) random realizations and (2) ownership. #FRA20

Participants pick three of six goods, and then we see how beliefs evolve as function of (1) random realizations and (2) ownership. #FRA20

Experimental setup #2: Classic endowment effect (some participants get USB power bank, “generic products with substantial heterogeneity in quality… scope for significant learning about product quality”)

Elicit WTP/WTA as (actual) Amazon ratings revealed. 🤯 #FRA20

Elicit WTP/WTA as (actual) Amazon ratings revealed. 🤯 #FRA20

(FRA coffee break had exactly what I needed to make it through the afternoon) #FRA20

After our break, we’ll hear five-minute presentations of six “early ideas.” I won’t tweet those, but one cool thing about FRA is the quantity and quality of anonymous feedback these presentations apparently produce for the presenters every year. #FRA20

Eating and drinking and having a great time, with a brief break for awards:

• Best discussant: James Weston

• Best poker player in finance: Todd Gormley

• Worst poker player in finance: Paul Décaire

• Best paper: Paul Décaire (a PhD student for the first time ever!!)

#FRA20

• Best discussant: James Weston

• Best poker player in finance: Todd Gormley

• Worst poker player in finance: Paul Décaire

• Best paper: Paul Décaire (a PhD student for the first time ever!!)

#FRA20