Just settling into @Grocery_Story for my work-related holiday read. Fascinating and well-researched read on the evolution of the grocery retail business in North America. Will be posting my highlights here.

1902: Combining 2+ stages of product development (vertical integration) wasn’t entirely new in turn-of-the-century America, but Kroger’s introduction of in-house bakeries was the first instance of it in the grocery retail business, lowering the price of its bread from 6c to 2.5c

1916: The self-service model was revolutionary and enabled stores to lower their prices even further. Shoppers, who were spending a hefty one-third of their budget on food (compared to 7–9 percent today), 14 welcomed this innovation

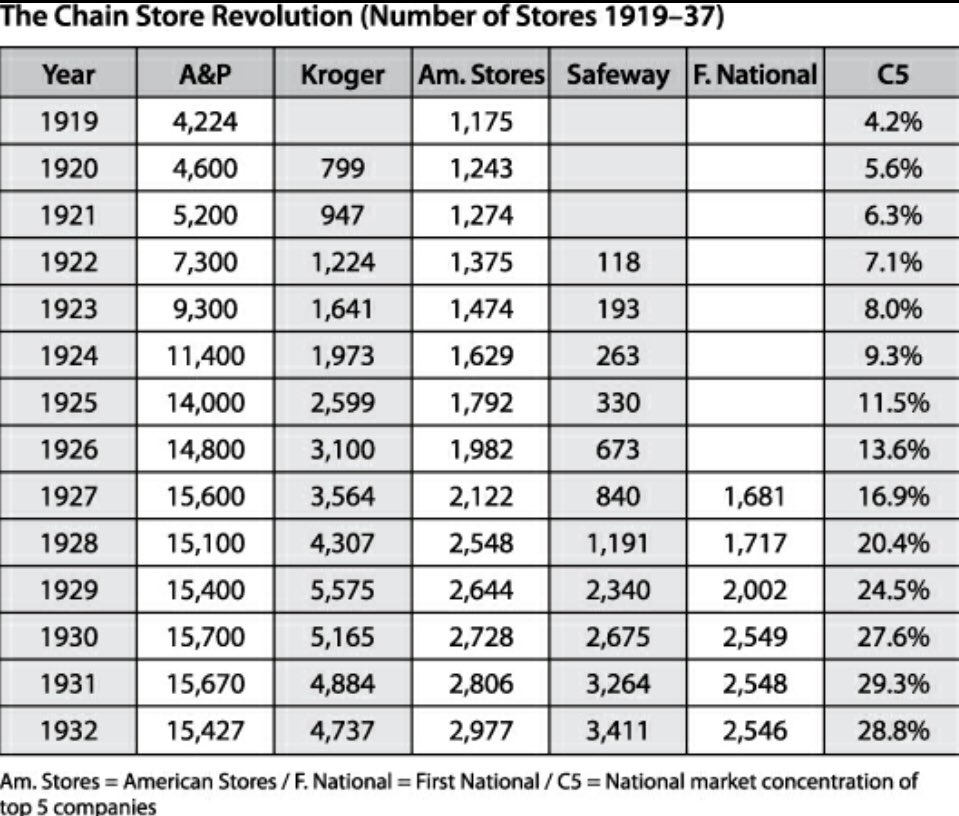

1930s: national chain stores emerge, market share of top 5 players reaches 30%

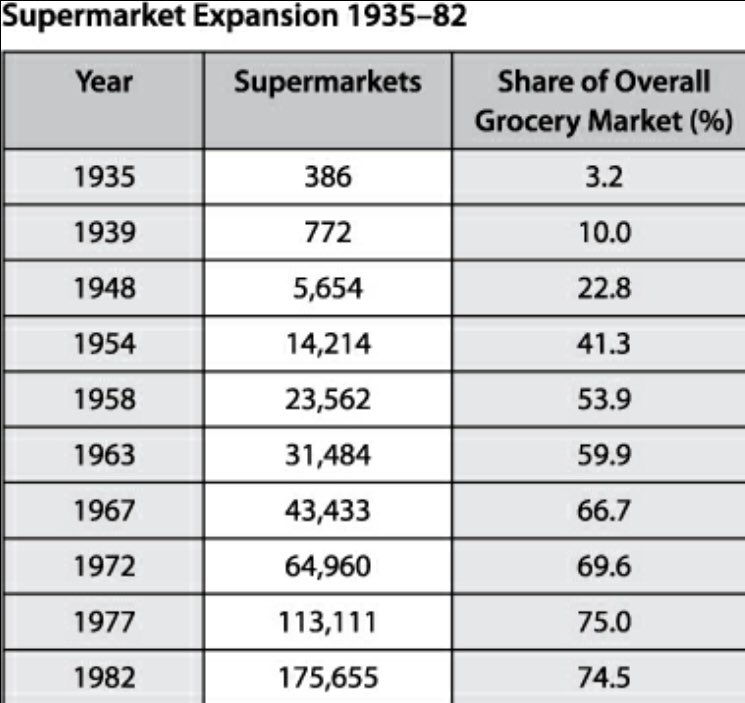

1935-1982 (the supermarket era): the number of supermarkets in America would grow from 386 to 26,640 (3.2% of the grocery market to 74.5%). With this growth would come the most aggressive era of antitrust enforcement in U.S. history.

1988: Walmart’s entry into the grocery business with the first supercenter sets off a wave of consolidation.

2016:

- the top 15 global supermarket companies are 30% of world supermarket sales

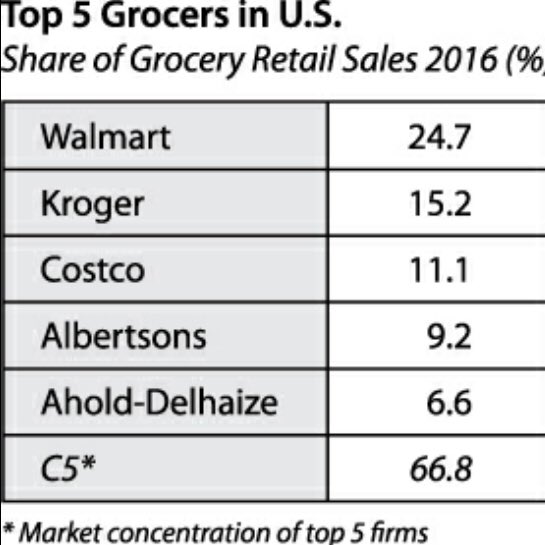

- US the top 5 food retailers today account for over 66% of national retail food sales

2016:

- the top 15 global supermarket companies are 30% of world supermarket sales

- US the top 5 food retailers today account for over 66% of national retail food sales

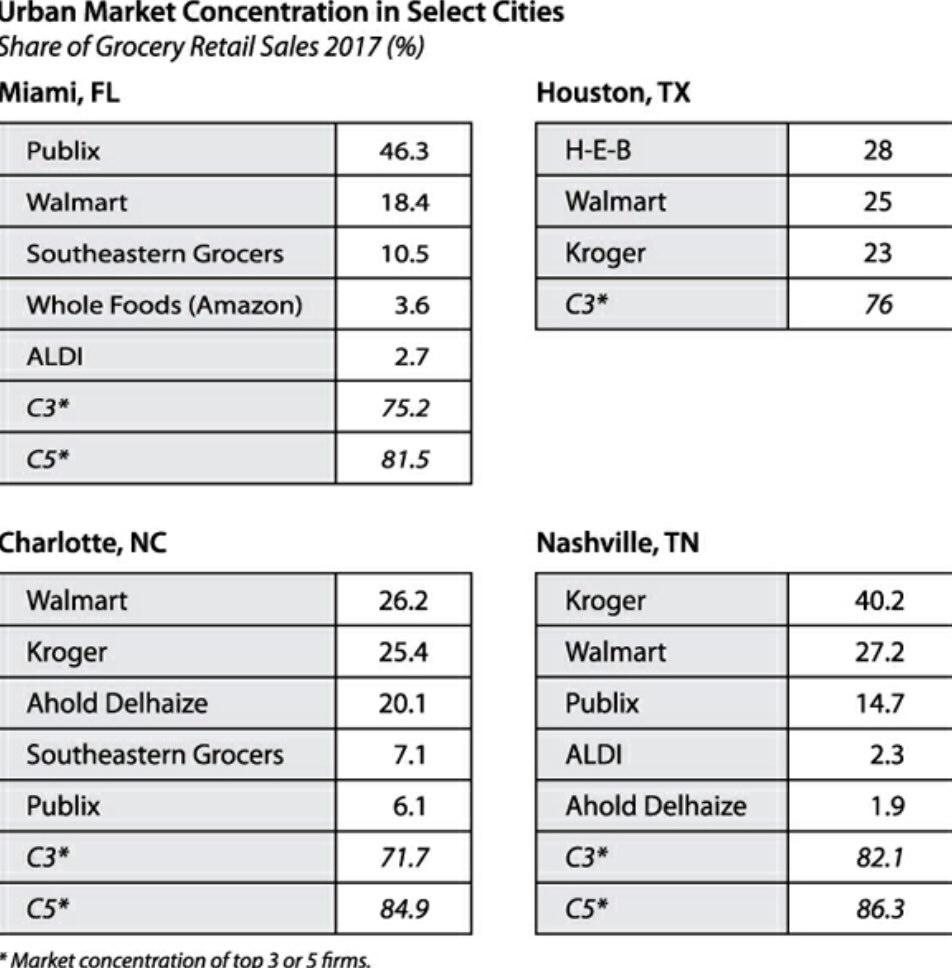

Local markets, where competitive dynamic manifests most directly in price, are often far more concentrated:

- in south Texas, H-E-B has 60% and H-E-B and Walmart together 87%

- C5 (concentration of top 5): Miami 81.5%, Charlotte: 84.5%, Nashville: 86.3%

- in south Texas, H-E-B has 60% and H-E-B and Walmart together 87%

- C5 (concentration of top 5): Miami 81.5%, Charlotte: 84.5%, Nashville: 86.3%

Key regulatory acts:

1. the Robinson-Patman Anti-Price Discrimination Act of 1936 ensured that a small neighborhood grocery store would have access to the same products at the same prices that were afforded to the largest grocery chains in the country

1. the Robinson-Patman Anti-Price Discrimination Act of 1936 ensured that a small neighborhood grocery store would have access to the same products at the same prices that were afforded to the largest grocery chains in the country

2. the Miller-Tydings Act of 1937: It protected the practice of retail price-maintenance, thereby allowing foodmakers to set a minimum price that their products would be sold at in stores

The effects of Robinson-Patman and Miller-Tydings were felt immediately. Chain stores no longer had a price advantage over their smaller competitors, and their market share decreased correspondingly. A&P was hit the hardest. For the first time in history, its profits were <2%

1980s: In the world of U.S. grocery retail everything changed in the early 1980s. The new Reagan administration’s “laissez-faire” approach resulted in far less regulatory action, while “reganomics” unleashed a wave of leveraged buyouts. In 1982 C4 was 17% climbing to 28% by 1999

Trade spend paid by CPGs to retailers, has 3 elements:

- Slotting Fees (get on the shelf)

- Contract Allowances (stay on the shelf)

- Promotional Allowance (get promoted)

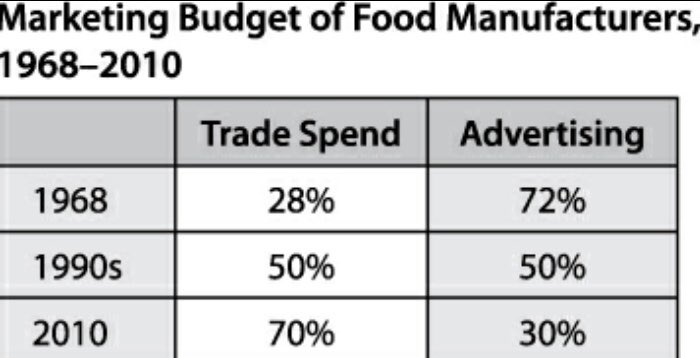

Overall, balance shifted significantly from ad to trade spend

- Slotting Fees (get on the shelf)

- Contract Allowances (stay on the shelf)

- Promotional Allowance (get promoted)

Overall, balance shifted significantly from ad to trade spend