How MercadoLibre is revolutionizing SME lending in Latin America with alternative data and ML

Thread reviewing the Bank of International Settlement's paper on Fintech & BigTech lending

bis.org/publ/work779.p…

⬇️⬇️⬇️

(1/15)

Thread reviewing the Bank of International Settlement's paper on Fintech & BigTech lending

bis.org/publ/work779.p…

⬇️⬇️⬇️

(1/15)

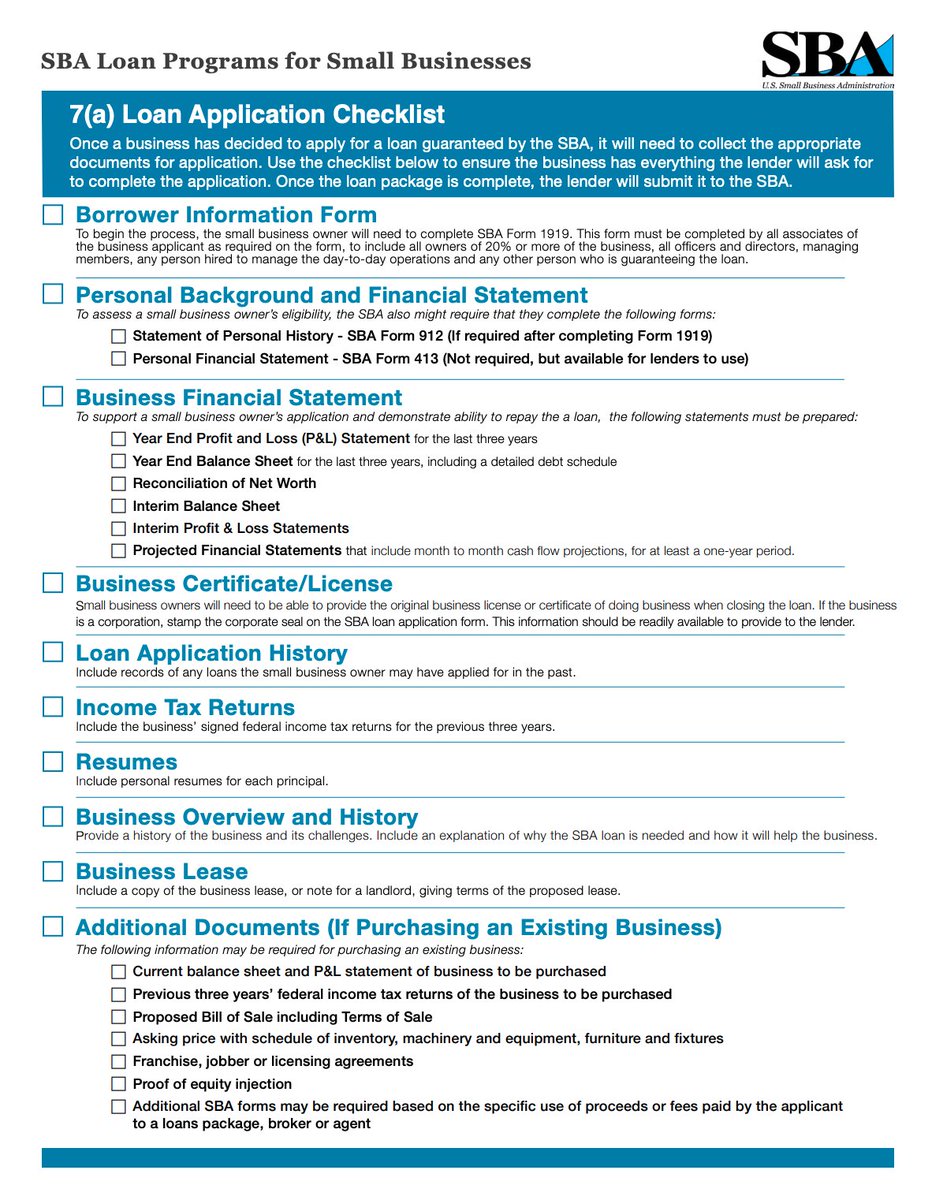

Lending was a cumbersome process for many SMBs before the likes of Square Capital, Stripe Capital, Shopify Capital etc

Check out this list of requirements by the US Small Business Administration to obtain a loan. Plan a few weeks to work that off

sba.gov/sites/default/…

(2/15

Check out this list of requirements by the US Small Business Administration to obtain a loan. Plan a few weeks to work that off

sba.gov/sites/default/…

(2/15

Square Capital and others revolutionized SMB lending in the US and other developed markets by underwriting loans using their merchants cash flow and applying machine learning to analyze millions of data points, often pro-actively selecting merchants who qualify for credit

(3/15)

(3/15)

Things still look different in developing markets. Loans are hard to obtain for many SMBs. They struggle to provide audited financial statements and overall lack formal documentation. But they often are customers of Fintech (e.g. payments) or e-commerce firms

(4/15)

(4/15)

Those firms can overcome strict requirements by exploiting the data SMBs produce by using their service. MercadoLibre can use transaction info (eg sales volume), reputation (eg claim ratio), network metrics (connection to other merchants) etc to assess credit worthiness

(5/15)

(5/15)

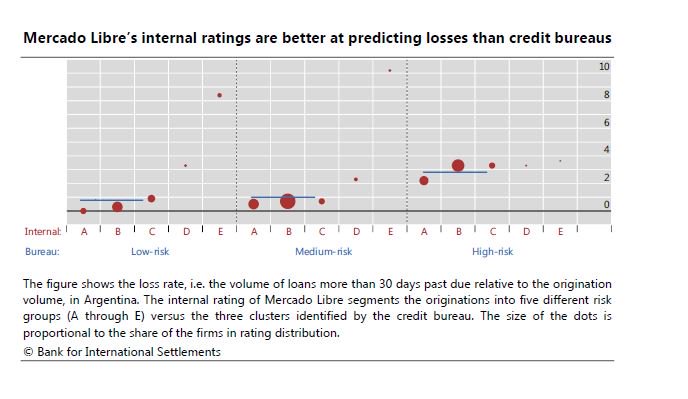

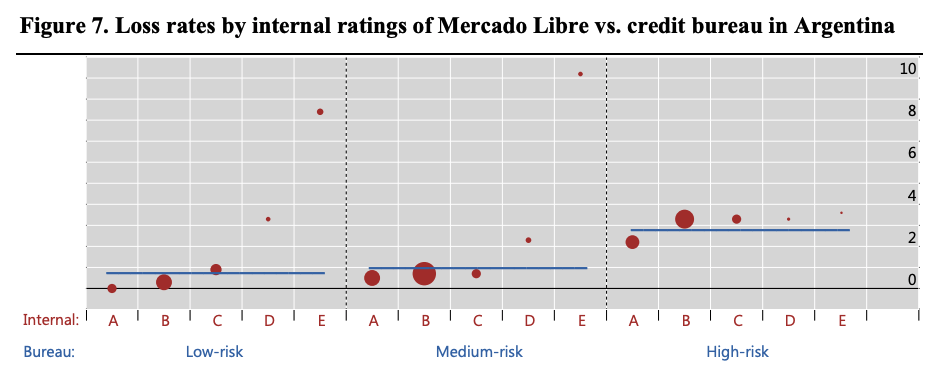

MercadoLibre seems to have gained a competitive advantage in identifying both high-risk borrowers and companies that otherwise would not qualify for credit.

See below MercadoLibre’s loan loss rate based both on credit bureau ratings and their internal A-E rating scale

(6/15)

See below MercadoLibre’s loan loss rate based both on credit bureau ratings and their internal A-E rating scale

(6/15)

As illustrated by the blue line, the average loss rate on loans that credit bureaus would have categorized as “High-risk” was 2.8% which, according to the authors, is “similar to the premium [small or medium enterprise] SME segment at traditional banks”.

(7/15)

(7/15)

In other words, MercadoLibre identified companies at low risk of default that traditional credit bureaus would have rated negative. According to the authors, such “High-risk” borrowers make up 30% of MercadoLibre’s portfolio and would not have received a loan otherwise.

(8/15)

(8/15)

Even more interesting, MercadoLibre identified high-risk borrowers whom the credit bureau classified incorrectly as “Low-risk” or “Medium-risk”, as shown by the outliers in category “E” within the bureau’s “Low-risk” and “Medium-risk” ratings.

(9/15)

(9/15)

➡️ MercadoLibre was able to identify risky borrowers the credit bureau simply and wrongly would have put in its low risk buckets. With MELI being able to fish out the 'best' risks, only bad risk borrowers may be left in the market - A potentially big problem for banks.

(10/15)

(10/15)

The authors also tested the thesis of MercadoLibre's credit assessment superiority more formally, using a ROC model.

Check out this introduction if you're interested. Also being not a data scientist, it's an interesting concept.

(11/15)

Check out this introduction if you're interested. Also being not a data scientist, it's an interesting concept.

(11/15)

They tested three models, one being MercadoLibre's ML approach. On the chart below, the false positives rate is plotted on the X-axis, the true positives on the Y. The model which maximizes the area under the curve minimizes false positives at different threshold levels.

(12/15)

(12/15)

MercadoLibre's ML model (blue curve) has the largest AUC (area under the curve. Don't confuse with AOC 🤡) and scores a higher predictive power than the credit bureau model, even when feeding the credit bureau model with additional MercadoLibre data (Model II).

(13/15)

(13/15)

Finally, the authors also found that merchants which received credit via MercadoLibre saw the number of offered products rise by 71-73% more in the following year than merchants that did not use credit. ..

(14/15)

(14/15)

.. Although it is unclear if this increase is due to the loan obtained by the merchant or if MercadoLibre primarily extends credit to merchants it expects to grow anyways.

Check out the full paper here:

bis.org/publ/work779.p…

(fin)

Check out the full paper here:

bis.org/publ/work779.p…

(fin)