1/ THREAD: WELP. Iowa Governor Kim Reynolds has basically just signed the death warrant for at least a few hundred Iowans with expensive pre-existing conditions. Some of them may have no choice but to leave the state or stay and die. Here’s why: acasignups.net/18/03/28/medic…

2/ In recent weeks, the Iowa state House and Senate passed a bill, which was just signed into law today by the Governor, which would allow the state Farm Bureau to open up non-ACA-compliant “health plans” (NOT legally defined as “insurance”) to ANYONE.

3/ The only reason these plans are legal to sell is because they aren’t legally defined as “health insurance” in the first place. That means they aren’t subject to ACA regulations. That means they can once again deny coverage (or charge thru the nose) people w/pre-existing conds.

4/ It also means they don’t have to cover the 10 Essential Health Benefits required by the ACA like maternity care, mental health care, hospitalization, surgery, prescription drugs…you know, stuff you’d expect to be covered by “health insurance”. Because again…not insurance.

5/ Basically, these plans are no more actual “health insurance” than a golf cart is an “automobile”. They may have some similar features—4 wheels, an engine, a steering wheel, seats—but that’s where the similarities end.

6/ A golf cart may be fine for driving around the range…on a sunny day. In warm weather. At slow speeds. On mostly flat grass. But it’s pretty much useless in any other condition.

7/ Now, golf carts are much less expensive than street-legal automobiles. A typical golf cart costs perhaps $5,000 or so, far less than even a small economy car like a Chevy Spark which runs around $13,000. Some people may think they only need a golf cart for now. Fine.

8/ I’ll come back to the golf cart thing soon. Meanwhile, what does this mean for the Individual Health Insurance market in Iowa? Well, if you earn less than 400% of the poverty line—around $48K/year for an individual or $98K for a family of 4, you qualify for ACA subsides.

9/ And if you earn less than *200%* of the poverty line ($24K individual or $49K for a fam of 4), you qualify for *heavy* ACA subsidies. But those subsidies are only available for ACTUAL HEALTH INSURANCE POLICIES sold on the exchange.

10/ OK, so here’s what should happen starting in 2019: Iowa’s an expansion state, so if you earn <138% FPL you qualify for Medicaid, yay. If you earn 138-200% FPL, you get heavy ACA subsidies, yay. No problems for these folks. They’ll mostly stick with the ACA exchange plans.

11/ However, from 200-400% FPL, the subsidies start to drop off. These folks might stay around if they have expensive problems…but if they’re healthy they’ll likely be enticed to drop out and go for the golf cart plan instead, trusting that they’ll stay healthy.

12/ The real problem is for those OVER 400% FPL—these folks get NO financial help at all, and ACA policies are *already* too expensive for them (in large part due to a whole mess of deliberate sabotage efforts by Trump last year). The obvious solution is to remove that 400% cap.

13/ Instead, Iowa has chosen to go the opposite route: They’re choosing to take a problem which was already kind of bad in 2016, which Trump deliberately made far worse in 2017, and make it even WORSE in 2018-2019.

14/ Here’s why: Many healthy people earning, say, 300-400% FPL, along with pretty much EVERY healthy person earning >400% FPL, will flee the exchanges for the dirt-cheap golf cart plans. This will cause the following:

15/ When those healthy people drop out, the only ones left on ACA plans will be really expensive to treat, turning exchange plans into a de facto High Risk Pool. Premiums will skyrocket, but ACA subsidies will climb to match, so SUBSIDIZED enrollees will pay about the same.

16/ So, if you have pre-existing conditions (or even if you don’t) and earn under 400% FPL, you’ll have a safe haven. And if you earn over 400% FPL and are *currently healthy*, you can get one of these dirt-cheap golf cart plans. Problem solved, right? Well…

17/ The problem is…what if you earn over 400% FPL but have a pre-existing condition? Or, alternately, what if you earn over 400% and are currently healthy but *develop* a condition which isn’t covered by the golf cart plan? Well…now you have a big problem.

18/ You can’t get an exchange plan which covers your needs because you can’t afford to pay full price without subsidies, which you don’t qualify for. However, you can’t get (or use) one of the golf cart plans because you’ll be denied coverage or it won’t cover what you need.

19/ So your choices are now limited to a) Try to get a job with a company which includes actual full health insurance benefits; b) Move out of Iowa; or c) Suffer and die.

But let’s go back to the golf cart metaphor. Ted Cruz and other Republicans have often claimed that Obamacare “forces people to buy Lambourghinis”, but that’s not true. There’s plenty of far cheaper cars. HOWEVER, every car DOES include certain mandatory features required by law.

21/ Every street-legal automobile…from the lowliest Ford Festiva to the priciest Cadillac Escalade, has to include doors, seatbelts, airbags, a crumple zone, etc etc. They have to meet certain minimum safety standards. They have to meet minimum emissions/efficiency standards.

22/ But here’s the thing—not only are Iowa’s new plans “golf carts”…they’re not even subject to the same types of *legal protections* that golf carts are. Why? Because they aren’t considered insurance, and therefore aren’t regulated by the insurance department.

24/ With actual health insurance, you may have to fight with your insurance company to get them to pay your claim, which sucks, but at least you HAVE the law on your side. With golf cart plans…nope. Sorry. Your state insurance dept’s hands are tied.

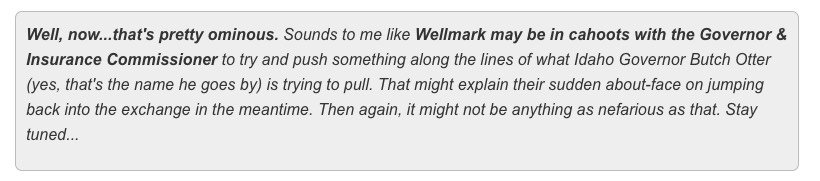

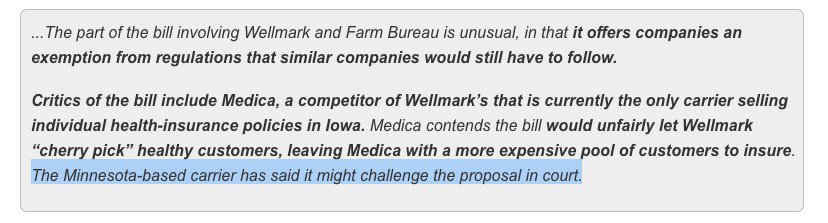

25/ Oh, and there’s another twist: Last year Wellmark, a huge Iowa carrier, announced they were dropping out of the ACA exchange, leaving Medica as the only carrier offering ACA policies. Wellmark recently announced they’re jumping back in next year: acasignups.net/18/02/12/iowa-…

26/ I noted at the time that it seemed kind of suspicious:

27/ Sure enough…the new “golf cart plans” will be offered by…Wellmark. Which means that Wellmark will get to have the best of both worlds—they’ll get heavy gov’t subsidies for sick/expensive ACA enrollees *and* corner the market on healthy/cheap Golf Cart enrollees.

28/ But what about Medica? Well, they can still offer ACA policies if they want to, and could no doubt jack up their rates for 2019 to keep from losing their shirts…but guess when the golf cart plans are scheduled to start being offered? JULY 1st. legis.iowa.gov/docs/publicati…

29 Assuming the exodus starts in July, Medica could very well see several thousand of their current healthy ACA enrollees flee halfway through the year. However, Medica won’t be allowed to jack up their premiums to cover the loss until January 2019.

30/ Since Medica is legally required to stick with their 2018 premiums thru 12/31/18, that means there also won’t be any additional tax credits/subsidies until 2019 either. Oh yeah—and most people wait until the 4th quarter of the year to have expensive medical treatments…

31/ …because they want to get it in before New Year’s before their deductible is reset the following year. In short, Medica did Iowa a favor this year by agreeing to step in when Wellmark dropped out…and now Medica is likely to be screwed for their trouble.

32/ Don’t get me wrong, I’m not saying Medica is a saint or anything, I don’t know anything about them. I’m just saying that they’re pissed as hell about this and rightly so:

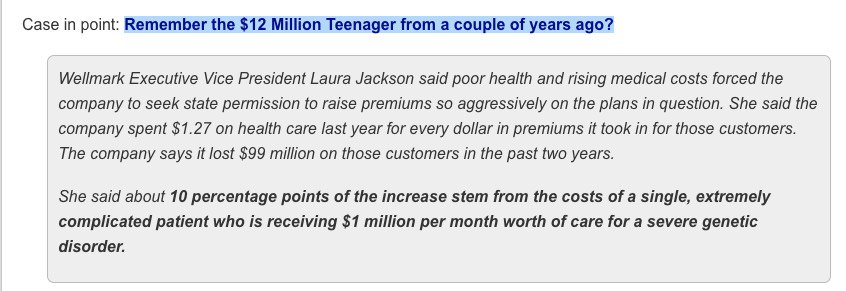

33/ And just in case you think Wellmark didn’t know EXACTLY what they were doing here, there was a perfect case study a few years ago: acasignups.net/16/09/28/updat…

34/ And again, just so I’m clear: The problem of jaw-dropping premium hikes for unsubsidized enrollees is REAL. I’m among those (it’s not as bad in Michigan as in Iowa, but it’s still tight). I’m not denying the *problem*, I’m criticizing the proposed *solution*…

35/ …because the “solution” being proposed here amounts to, in short, telling middle-class sick people to move the hell out of the state and become some other state’s problem.

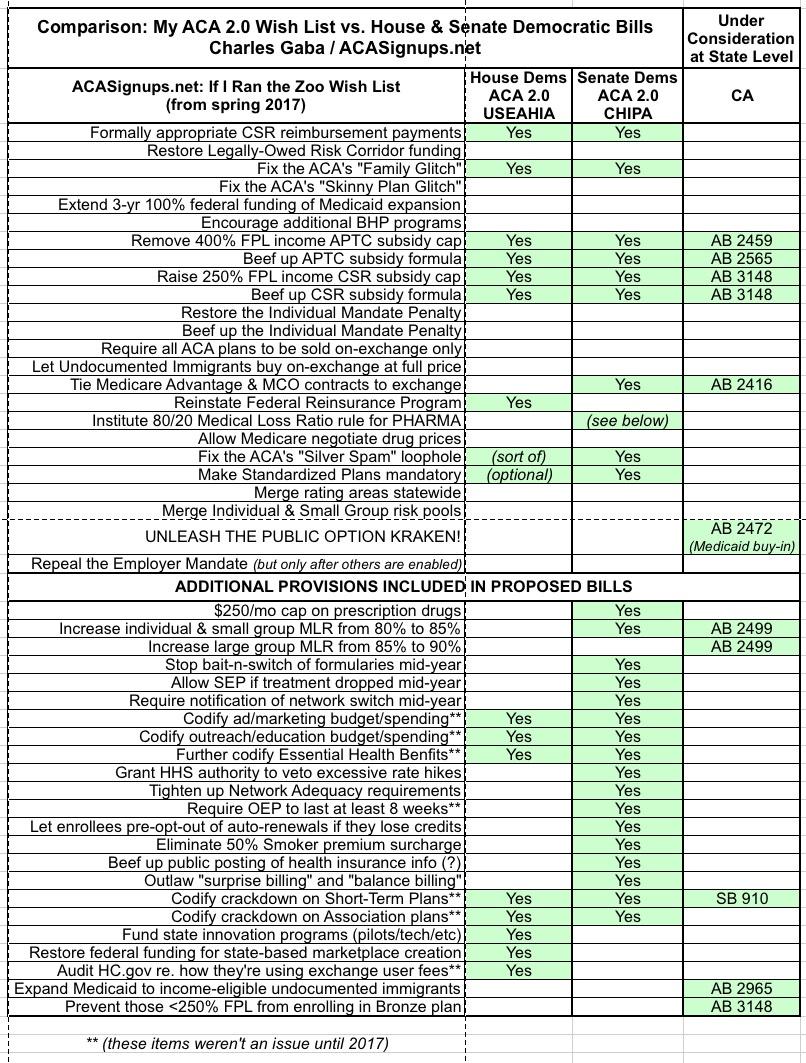

36/ The irony of all this is that there’s two bills on the table which could solve this problem WITHOUT kicking anyone to the curb: acasignups.net/18/03/31/calif…

37/ Even if you dropped 80% of these bills and stuck with these 4 items it would be a MASSIVE improvement over the current situation. Hell, even the first one (remove the 400% cap) would solve much of it.

38/ Anyway, that’s the situation in Iowa. If you find my work at ACASignups.net useful and can afford to do so, please consider supporting it, thanks! acasignups.net/18/03/15/help-… /END

P.S. Another good point made here: The ACA’s limited-time Open Enrollment Period remains in place, which means that if you’re on a Golf Cart Plan and suddenly need to switch to a full ACA plan mid-year, you’re screwed even if you can afford full price. a/

In other words, no, you can’t simply coast along on a Golf Cart Plan from Jan - June, then get diagnosed with cancer/etc and suddenly decide to enroll in an ACA plan in July. You have to wait until November for coverage starting in January. By which point you might be dead. b/b

P.P.S. For anyone wondering WHY the ACA restricts enrollment to a short time window, that’s exactly why: To prevent people from gaming the system by skipping out most of the year and only enrolling when they need it. Same reason most employers & Medicare have limited windows.

This is also why almost every state requires you to buy auto insurance to own a car and why you can’t get a home mortgage without homeowner’s insurance in place first.