,

14 tweets,

6 min read

Read on Twitter

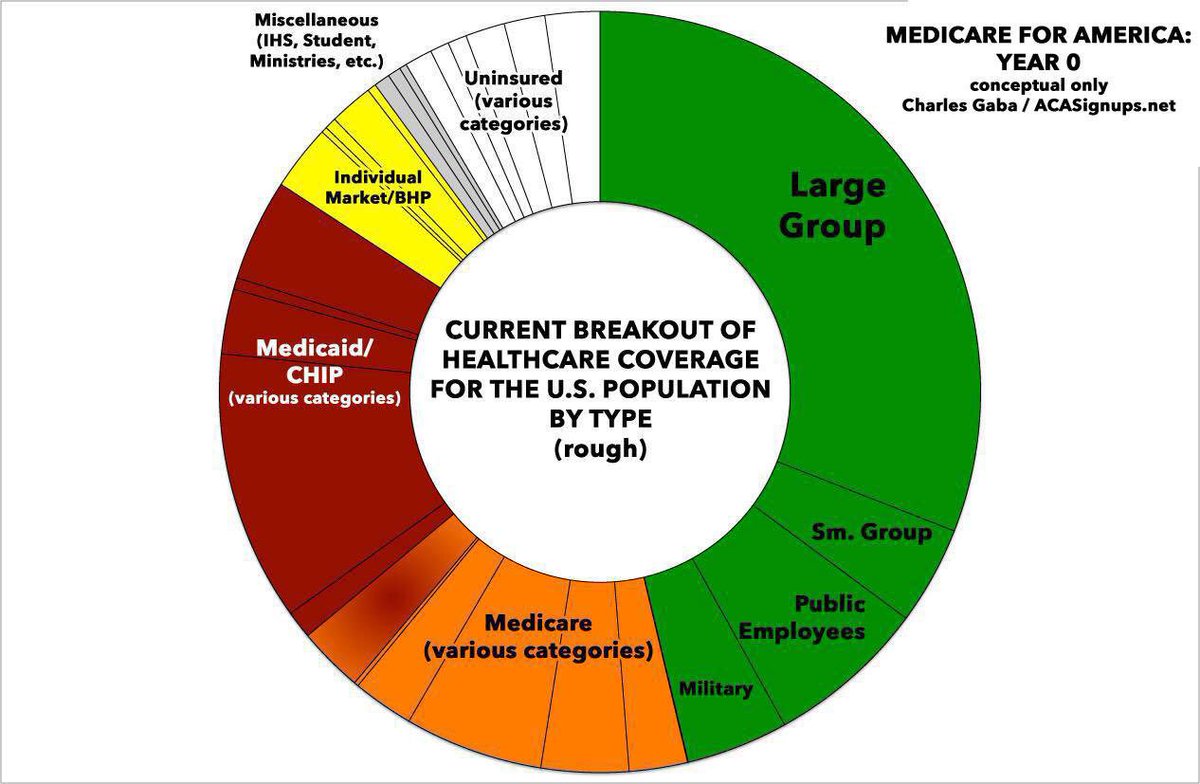

Here’s some crude graphics explaining how #Med4America would be phased in. First, here’s a rough breakout of the current healthcare/ health insurance coverage situation of the entire country today:

Nearly half the population is covered through their employer. Another third is covered by Medicare, Medicaid or CHIP. Around 5% is on ACA Indy market plans. Another 2% or so has miscellaneous coverage including junk policies, sharing ministries etc., and 10% have nothing at all.

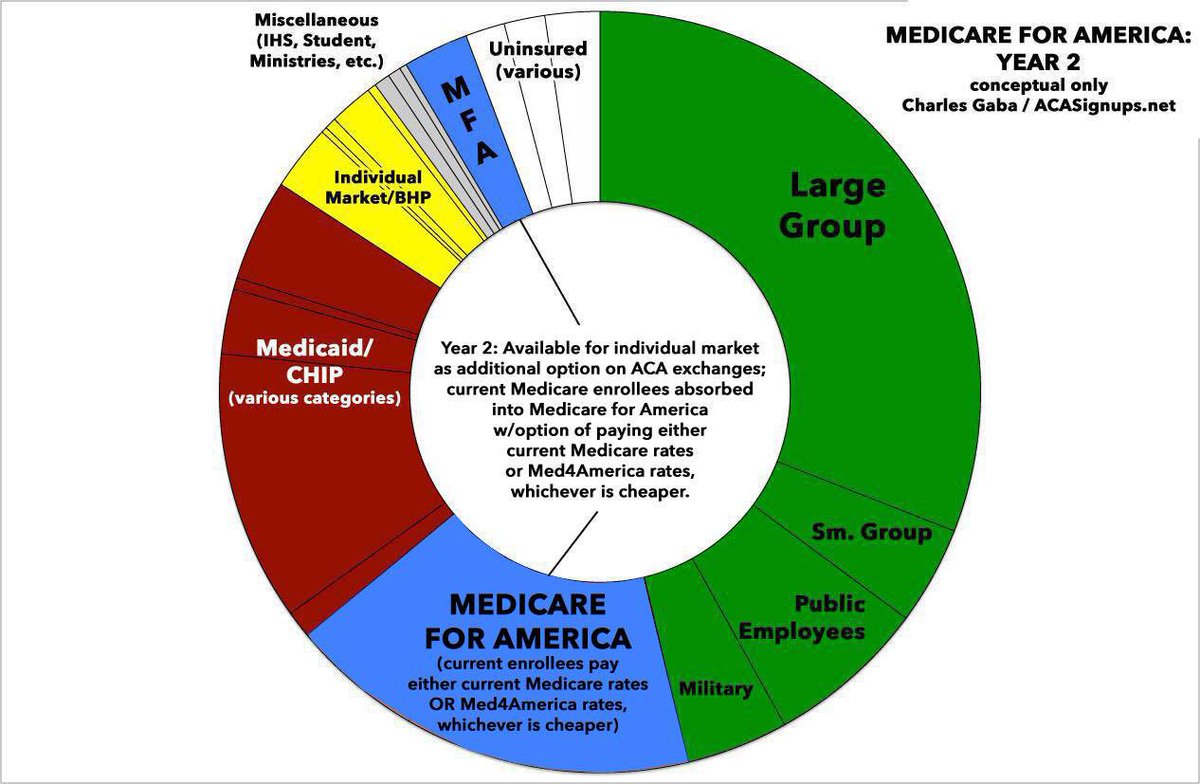

Here’s how #Med4America would be phased in. First, existing Medicare would be expanded to a FAR more comprehensive version (including dental, optical, long-term care, etc) while also being offered as a Public Option on the ACA exchange. Subsidies would be vastly expanded.

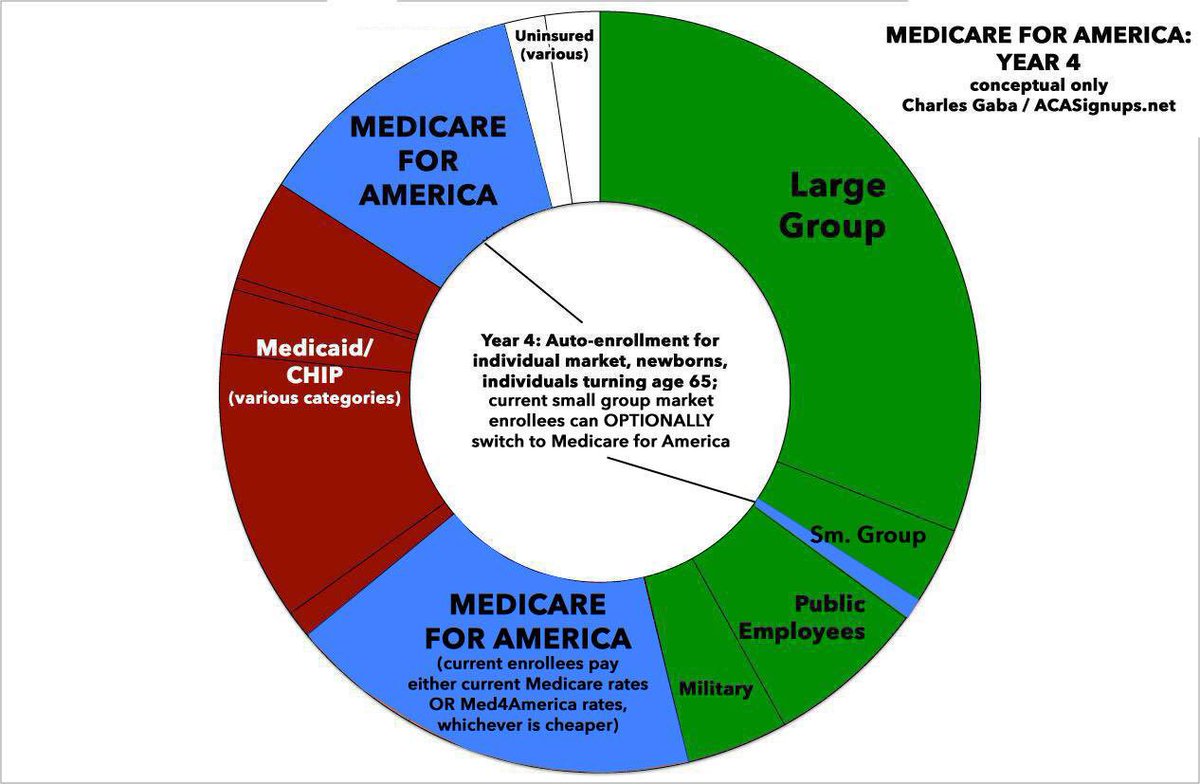

Then, #Med4America would replace the ENTIRE ACA individual market, while also being offered OPTIONALLY to small business employees who wanted to switch to it. In addition, all newly-eligible 65-year olds and newborn infants would be auto-enrolled.

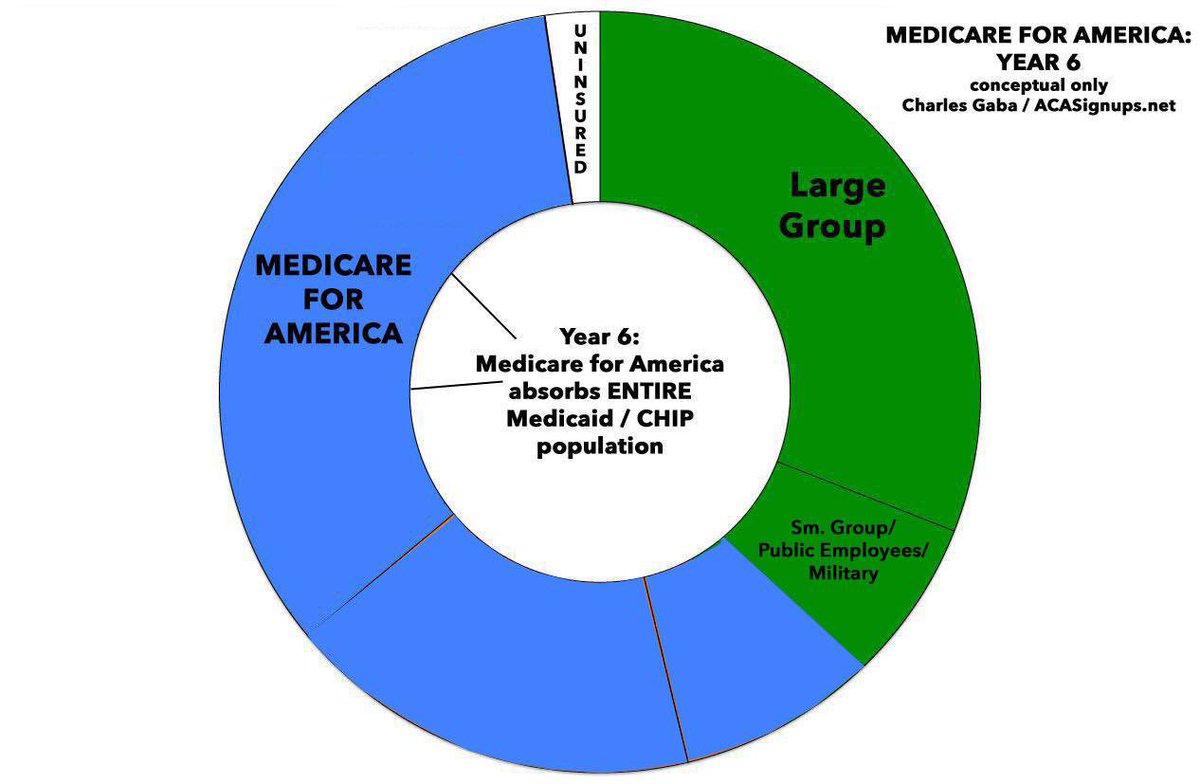

Next, #Med4America would take over Medicaid & CHIP enrollees. By this point roughly 60% of the population should be enrolled in the program.

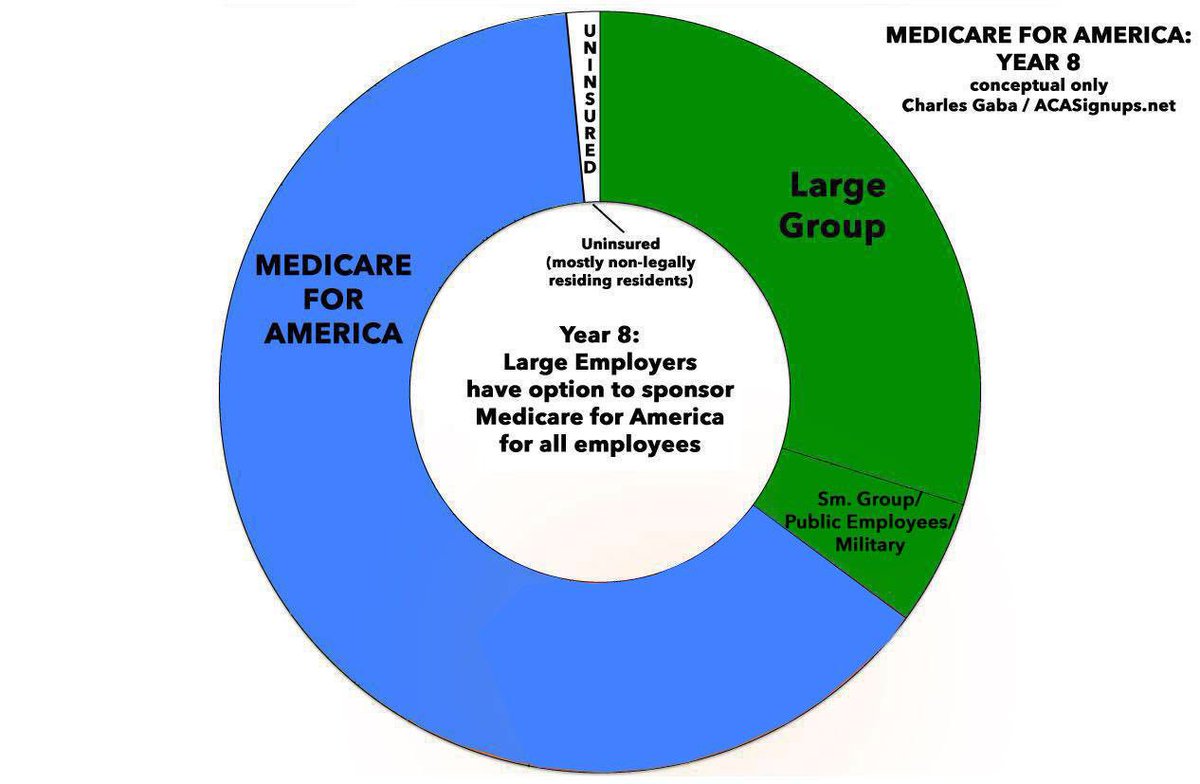

Finally, LARGE employers, who currently cover ~100 million people, would be allowed to OPTIONALLY switch to #Med4America OR could continue to offer private coverage but ONLY Gold level or higher (no junk!). ALTERNATELY, their employees could make the switch individually.

From that point on, it’d just be a matter of time. If the private employer market still made sense for some companies and their employees, fine. If not, they could switch. Meanwhile, the auto-enrolled newborns would gradually expand the #Med4America market share anyway.

As for costs: For those earning less than 200% FPL (~$24K/yr for a single adult, ~$50K for a family of 4), it WOULD effectively be 100% “pure” single payer...zero premiums, deductibles or co-pays. After that it’d be a sliding scale.

Under no circumstances would ANYONE have to pay more than 9.7% of their income in premiums, more than $500 in deductible or more than $5,000 in total out of pocket costs.

The main thing is that it would walk the line between making the program mandatory vs optional. It’d be mandatory for the half of the population least likely to object but optional for the half most likely to.

How it’d be paid for:

—sunset the GOP tax bill

—5% surtax on AGI (w/capital gains) over $500,000

—increasing the Medicare payroll tax

—increase net investment income tax

—increase excise taxes on tobacco, alcohol & sugary drinks

—8% payroll tax for employers which switch to it

—sunset the GOP tax bill

—5% surtax on AGI (w/capital gains) over $500,000

—increasing the Medicare payroll tax

—increase net investment income tax

—increase excise taxes on tobacco, alcohol & sugary drinks

—8% payroll tax for employers which switch to it

Anyway, more details here. The specifics will likely be tweaked, of course, but this should cover the general structure pretty well.

acasignups.net/19/02/05/updat…

acasignups.net/19/02/05/updat…

As an aside: If you find my work of value and would like to support it, please donate either once or monthly here!

acasignups.net/donate

acasignups.net/donate