A company's value is driven by one thing: risk adjusted cash flows

This depends mainly on:

-Growth

-ROIC

-Cost of capital

Outperformance requires anticipating revisions to cash flow estimates. If high returns (& growth) are maintained, there are likely to be revisions higher

This depends mainly on:

-Growth

-ROIC

-Cost of capital

Outperformance requires anticipating revisions to cash flow estimates. If high returns (& growth) are maintained, there are likely to be revisions higher

To understand this deeply, it’s important to disaggregate cash flow into growth & ROIC, to see how they're linked

Growth=ROIC x Investment Rate

Cash Flow=Earnings x (1–Reinvestment rate)

Rearranged, Investment rate=Growth/ROIC

Cash flow=earnings x (1–Growth/ROIC)

Growth=ROIC x Investment Rate

Cash Flow=Earnings x (1–Reinvestment rate)

Rearranged, Investment rate=Growth/ROIC

Cash flow=earnings x (1–Growth/ROIC)

This has important implications. Let’s take an example.

Imagine if a company has very attractive growth opportunities over a 5 year period. Say it can grow at 20% annually. But this growth requires quite a bit of investment (in working capital and capex for instance)

Imagine if a company has very attractive growth opportunities over a 5 year period. Say it can grow at 20% annually. But this growth requires quite a bit of investment (in working capital and capex for instance)

The returns on the investment, however, are attractive. Say, 20%. The investment must be made every year for 5 years (and then the reinvestment rate declines from 100% to 50%, as growth slows to 10%). Initially, it’s FCF will thus be depressed

It’ll be much lower than, say, if a company were growing at only 10% with similar returns (ie reinvesting only 50% from the start). But the value of the former will be higher because of the impact on long term cash flows, ie beyond the 5 years

If you’re screening on FCF yield, or focusing only on the next 2-3 years, you’ll likely miss the opportunity.

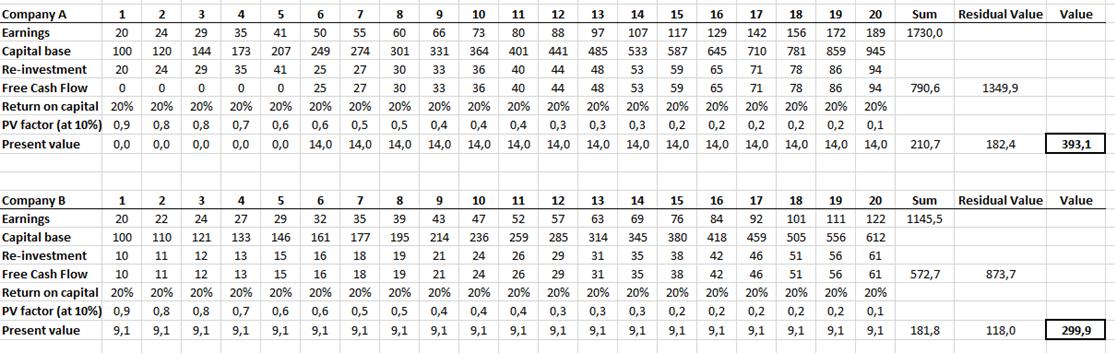

Here’s the previously mentioned example illustrated over a 20 year period (with a 10% WACC and a 3% residual growth rate)

Here’s the previously mentioned example illustrated over a 20 year period (with a 10% WACC and a 3% residual growth rate)

At the onset (or during the early years), Company B might appear to be more valuable. Why?

Because its growth is more consistent (and is expected to continue to be consistent…for example a consumer staples company), and it’s more cash generative

Because its growth is more consistent (and is expected to continue to be consistent…for example a consumer staples company), and it’s more cash generative

How many investors at yr 1-2 using typical DCF (going out 5 yrs) would estimate that company A is worth 30% more than B? Typical arguments might be: doesn’t generate cash now & won’t over coming yrs, very hard to forecast beyond, earnings growth will slow after initial period...

Please note that I realize this example is simplified & perhaps a bit extreme, & that finding companies that can maintain 20% ROIC for 20 years is somewhat rare (same for 10% earnings growth). But that doesn’t change the fact that this is what you should be looking for

Also, if you want to understand why intrinsic value grows…take away years 11-20 in the model. You’ll have the same residual growth rate with the same WACC, & will have a higher present value factor (because it’s only 10 years). But the intrinsic value is far lower

Why? Because there is higher growth in FCF in years 11-20 than the residual, and the present value factor doesn’t offset it. This should illustrate the importance of finding companies that can earn high returns for 20-30 years

Preferably, they can invest large amounts of capital at those high returns, but even if they can’t, as long as they realize it and act accordingly, it can still lead to a good outcome

The next question becomes: what allows companies to maintain high returns on capital for an extended period? Is this common? Can it be predicted?

That’ll be for another thread

That’ll be for another thread