,

10 tweets,

4 min read

Read on Twitter

On 3rd July, the CBN in its bid to improve lending to the real sector; mandated all Banks to maintain a Loan to Deposit Ratio (LDR) of 60% by Sept 30. Failure to do so will result in a levy of additional CRR equal to 50% of the lending shortfall of the target LDR.

A Short Thread

A Short Thread

Why did the CBN take this move?

Because it wanted to encourage lending to the SMEs, Retail, Mortgage and Consumer sectors of the economy. Data shows that while loans to Oil & Gas sector has been increasing, loans to other sectors has been decreasing or stagnant.

Because it wanted to encourage lending to the SMEs, Retail, Mortgage and Consumer sectors of the economy. Data shows that while loans to Oil & Gas sector has been increasing, loans to other sectors has been decreasing or stagnant.

For instance, between 2014 and 2018, loans and advances to Oil & Gas and Finance increased by 29% and 17% respectively, while that of trade and general commerce decreased by 13%. Real Estate remained stagnant.

The case of SMEs is even worse because loans as a percentage of total credit decreased by 98.9% from 27.04% in 1992 to 0.29% in 2018. A look at these stats will clearly explain why the real sector have been struggling. There is clearly a lack of sufficient credit for funding.

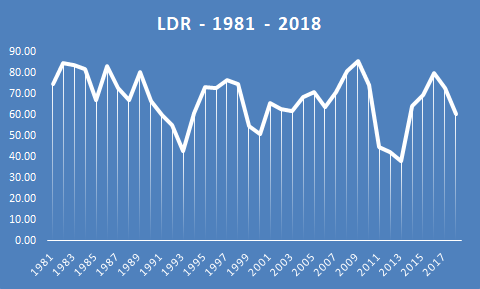

Historically, from 1980 - 2018 (a period of 38 years) the LDR has averaged around 67% for the banking sector against a prescribed maximum of 80%. Ranging from a low of 38% in 2013 to a high of 86% in 2009. However, in the last 5 years it has hovered around the 70% mark.

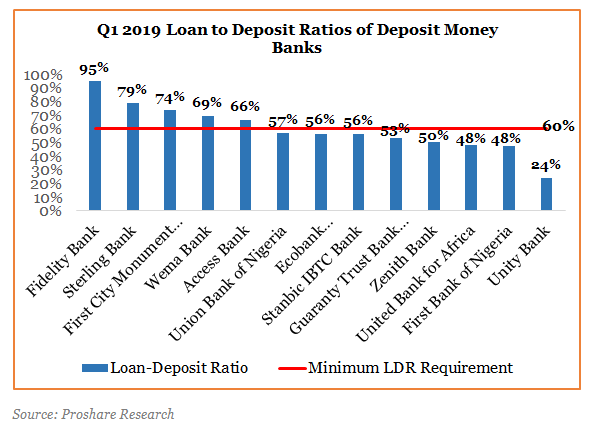

According to @proshare as at Q1:2019, only 5 banks were above the 60% LDR mark with Fidelity Bank leading the pack at 95% followed by Sterling Bank (79%), FCMB (74%), Wema (69%) and Access Bank (66%). The others have up to 30th Sept to meet up with the new LDR requirement.

Overall, 67% of banks are below the LDR, while only 33% are above. From Q1:2019 figures, we can estimate that the CBN is going to unlock abt N1.7 Trillion of credit into the real sector by Oct 2019.

How is the CBN anticipating this will happen?

1) A reduction in debt securities

How is the CBN anticipating this will happen?

1) A reduction in debt securities

2. An increase in (higher risk) loans to the real sector

The CBN anticipates that if the banks reduce their investment in debt securities, they'll have no choice to find other means to generate income from those additional funds. The banks notwithstanding are not without options

The CBN anticipates that if the banks reduce their investment in debt securities, they'll have no choice to find other means to generate income from those additional funds. The banks notwithstanding are not without options

Nevertheless, moving from a risk free investment portfolio to high risk/high yield one poses financial credit risk for the banks. The possibility of higher Non-Performing Loans (NPLs) is a real possibility. Aggressive loan growth could also impact Capital Adequacy Ratio.

In-short, this is a move that has the potential of creating more problems for banks. While at the same time, it is a move that has the potential of creating growth for the real sector and hence for the economy which will increase the GDP. At this point, it is fingers crossed.