,

29 tweets,

12 min read

Read on Twitter

Here in the United States, banks are required to meet the credit needs of the communities where they do business, under the Community Reinvestment Act of 1977. Penalties for violating the act can include temporarily freezing a bank's asset growth or denying all merger requests.

Some consider the law to be the last great policy of the Civil Rights era, in line with the Civil Rights Act (1964), Voting Rights Act (1965), Fair Housing Act (1968), Equal Credit Opportunity Act (1974). Notice the gradual expansion from political rights to economic rights?

The Community Reinvestment Act or CRA went beyond merely outlawing "redlining" -- the practice of banks avoiding making loans to certain neighborhoods with a clear racial pattern as a result of systematic policies and real estate industry practices. nybooks.com/articles/2018/…

The law stipulated *affirmative* obligations for banks to meet credit needs of all communities where they do business, especially low-income communities. It was race-neutral on paper, but in spirit & practice there has always been a racial dimension to "low-income communities."

Power concedes nothing without a demand. It was community organizers like Gale Cincotta and others on the West Side of Chicago and their allies who are credited with getting the CRA legislation passed nytimes.com/2001/08/17/us/…

There are some exceptions to this rule, but the banking industry by and large has long-held deep opposition to the law. Banking industry lobbyists have pushed tropes like "the CRA forces banks to make risky loans to low-income borrowers, leading to financial crises"...

...when in fact, evidence to the contrary has been found and touted as of

2019: fuqua.duke.edu/duke-fuqua-ins…

2015: federalreserve.gov/econresdata/no…

2010: communitycapital.unc.edu/research/cra-d…

2008: reuters.com/article/usa-fe…

2008: money.usnews.com/money/blogs/th…

The CRA DOES NOT cause financial crises. Full stop.

2019: fuqua.duke.edu/duke-fuqua-ins…

2015: federalreserve.gov/econresdata/no…

2010: communitycapital.unc.edu/research/cra-d…

2008: reuters.com/article/usa-fe…

2008: money.usnews.com/money/blogs/th…

The CRA DOES NOT cause financial crises. Full stop.

& that's not even the half of it. @USOCC is one of the main federal agencies tasked with enforcing the CRA. The current head of that agency was previously CEO of a bank accused of violating the Fair Housing Act & CRA. Now he wants to water down the CRA porter.house.gov/sites/porter.h…

But it is true that the CRA regulations need some work. Historically, 98 percent of banks get a passing grade ("Satisfactory" or "Outstanding") on their CRA exams.

I don't know about you, but I have never, ever come across a community where banks are meeting all credit needs.

I don't know about you, but I have never, ever come across a community where banks are meeting all credit needs.

For more than a decade after the CRA passed, regulators didn't even require banks to make their CRA examinations public.

If you're like me, you get a little excited when the @FDICgov sends out its quarterly list of banks examined under the CRA in the past three months.

If you're like me, you get a little excited when the @FDICgov sends out its quarterly list of banks examined under the CRA in the past three months.

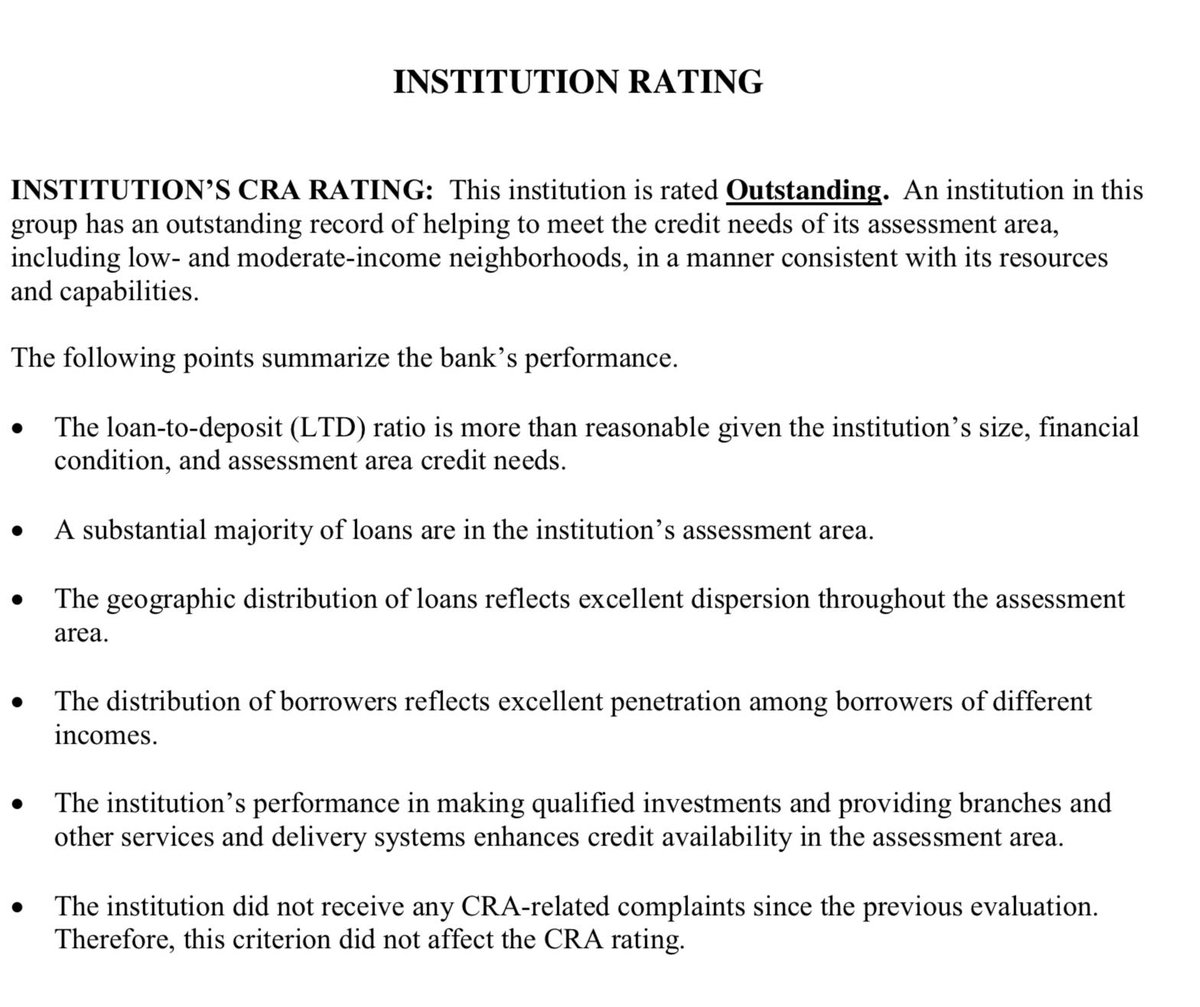

Let's walk through an excellent example of a bank that got the highest rating, "Outstanding," on its CRA exam completed last quarter, @springbankny, the only bank based in the South Bronx. Here's the document: www5.fdic.gov/CRAPES/2018/58…

Over the years, regulators have worked with the banking industry and community advocates to hash out a somewhat standardized process for determining community needs and evaluating banks for meeting those needs. ncrc.org/wp-content/upl…

The standard process allows banks to define their own service areas — "the places where they do business." Here's how Spring Bank defined its services area and the demographics of that area.

& then there's the distribution of businesses by size within the service area.

Examiners check to see whether the bank's lending is WAY out of line w/pop. distribution by income or biz size, to see if the bank is blatantly ignoring anyone. (NOTE: race is left out of evaluation)

Examiners check to see whether the bank's lending is WAY out of line w/pop. distribution by income or biz size, to see if the bank is blatantly ignoring anyone. (NOTE: race is left out of evaluation)

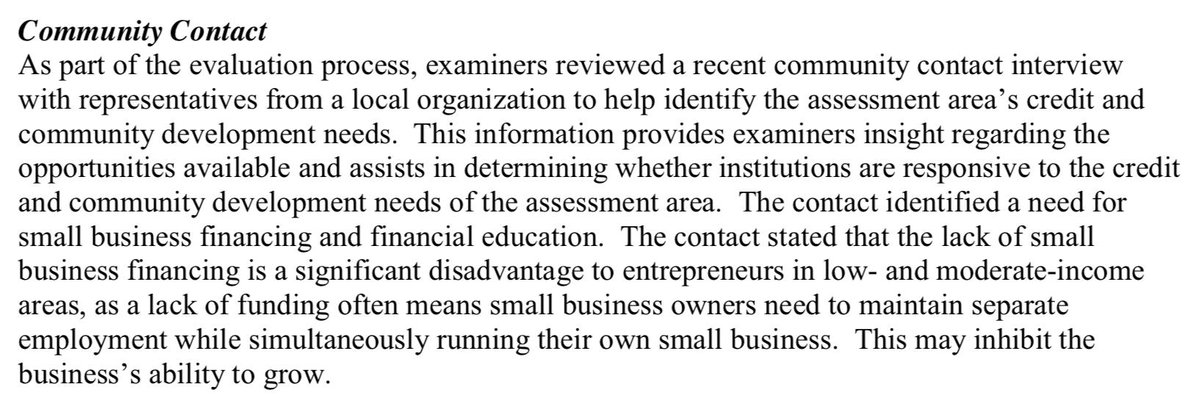

& then, perhaps most interesting, the CRA examiners, who work in the local office of the federal regulator (in this case

@FDICgov) where the bank is headquartered, also reach out to "community contacts" whose feedback remains anonymous.

@FDICgov) where the bank is headquartered, also reach out to "community contacts" whose feedback remains anonymous.

And here's a big problem/opportunity moment with this law. You might be thinking, the regulator only spoke with one organization? This is the South Effing Bronx. New York City. You can't walk down the street without running into two or three community-based groups. What gives?

It's not the bank's fault. The CRA gives communities the right to comment on bank CRA examinations and even on the ~200 bank merger applications a year. But, like voting, you need to show up to exercise that right. Could regulators do a better job reaching out? Sure they could.

But communities can also help themselves by knowing exactly when banks serving them are going to be under the CRA examination microscope. You can also sign up to get the examination schedules delivered to your inbox on the regular. fdic.gov/regulations/co…

ANYWAY back to @springbankny's CRA exam and dig into some of the data available.

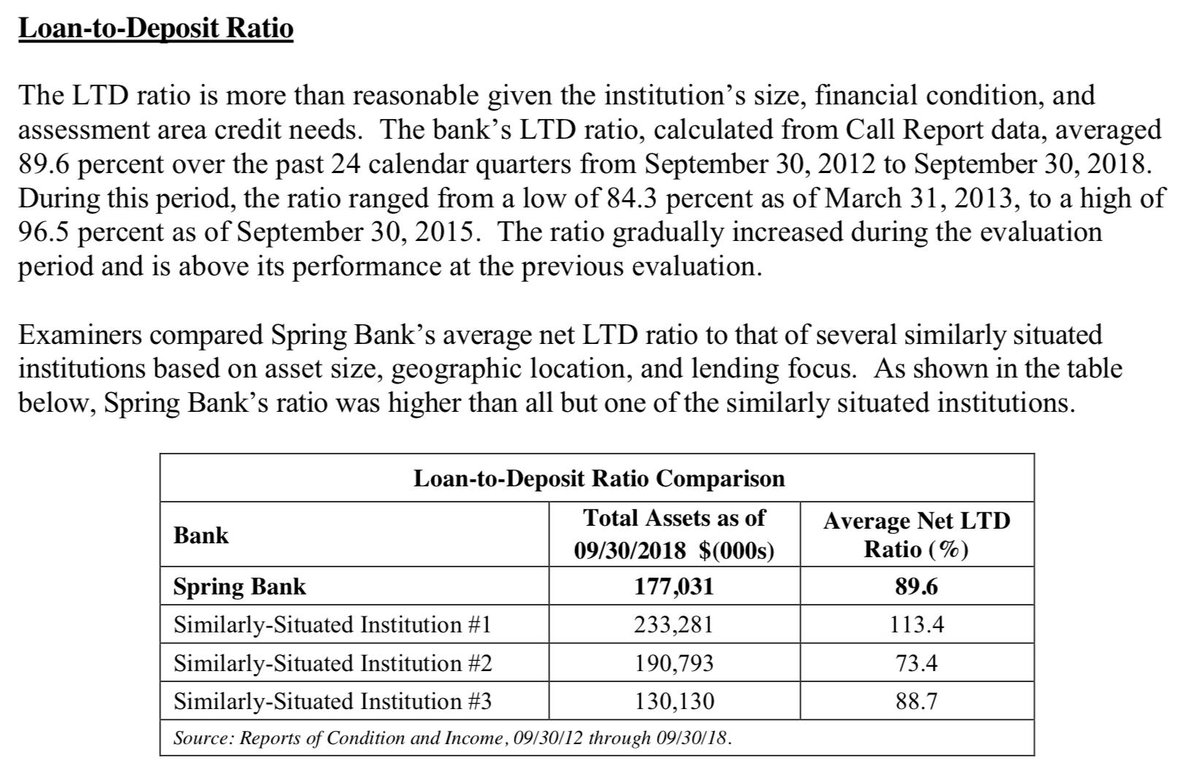

Let's start with something comprehensive, the bank's loan-to-deposit ratio. Examiners want to know what proportion of deposits are being loaned out instead of placed in more exotic investments.

Let's start with something comprehensive, the bank's loan-to-deposit ratio. Examiners want to know what proportion of deposits are being loaned out instead of placed in more exotic investments.

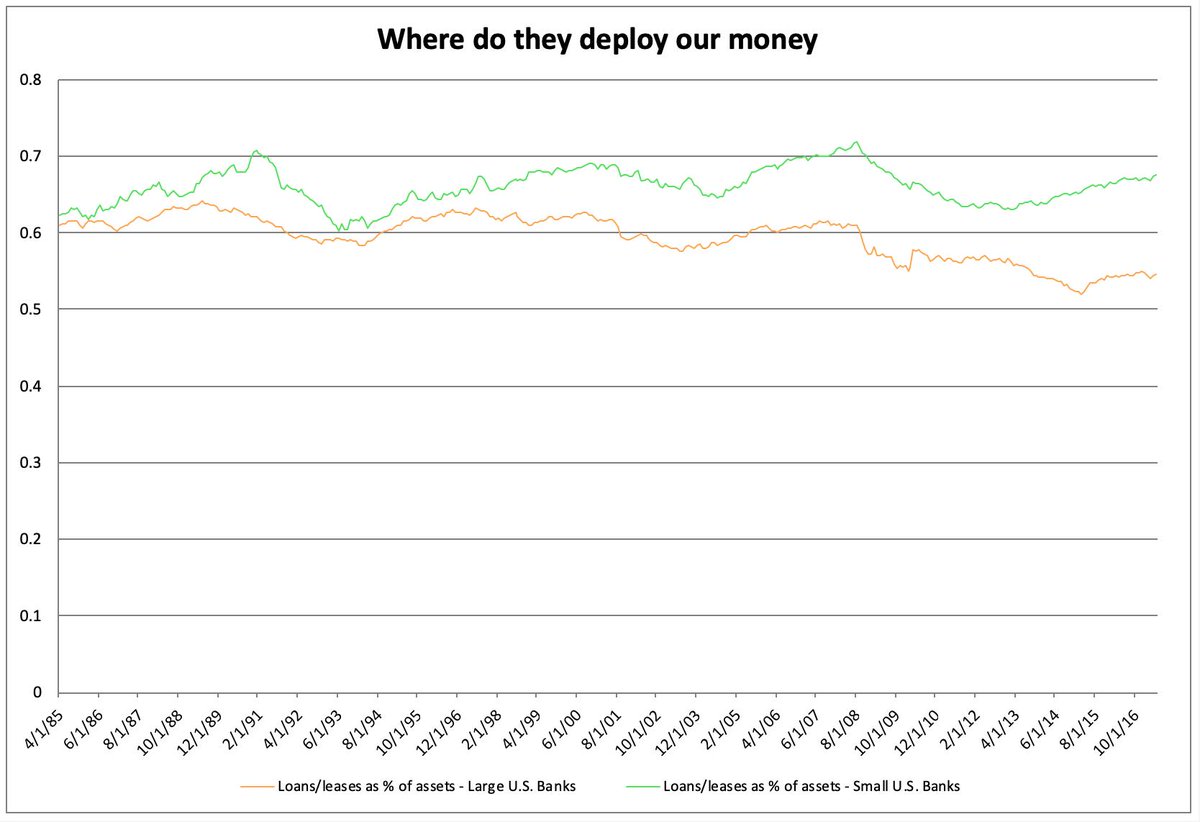

Some context: big U.S. banks (defined as the top 25 largest banks by asset size) currently show a loan-to-deposit ratio in the mid 50%s. The rest ("small" banks) show a ratio of around 67%. (Source: fred.stlouisfed.org)

At Spring Bank, that ratio is 89%.

89 percent!!!!

At Spring Bank, that ratio is 89%.

89 percent!!!!

Okay moving on. Here's home loans by income level. The examiners conveniently rehash the pop. dist. by income alongside lending. The South Bronx being mostly larger rentals, the examiners looked at lending to such buildings for renovations or acquisition by new landlords.

As the examiners note below the chart, the pattern is pretty good.

Not noted here, the increase in residential lending to moderate-income tracts may reflect demographic changes around the buildings where Spring Bank is financing repairs or renovations. (i.e. gentrification)

Not noted here, the increase in residential lending to moderate-income tracts may reflect demographic changes around the buildings where Spring Bank is financing repairs or renovations. (i.e. gentrification)

& here's small business loans, by geographic distribution according to income levels. Once again as the examiners note, the pattern is pretty good. Spring Bank is lending to businesses located in the areas that are most historically disinvested. That said...

...it's not guaranteed that the loans to businesses in low-income census tracts are going to businesses whose owners live in those census tracts or if they're owned by, say, big corporations or maybe they're tech startups founded by wealthy though well-meaning outsiders.

The Dodd-Frank Act included a provision requiring for banks to provide data to the public that would make such an analysis possible, but that regulators have yet to finalize regulations and enforce that requirement. nextcity.org/daily/entry/sm…

So without that data, what can we know about whether @springbankny is really reaching small business owners who actually live in low-income area? For now, we can at least report on the bank's strategy & practices intended to meet their needs: nextcity.org/daily/entry/sm…

@springbankny & that wraps up this edition of how to hold banks accountable for stewarding your city's or your community's or your country's deposits.

@springbankny Also happy Friday, y'all. Btw I'm going on vacation next week to see the Grand Canyon for the first time. ✌✌✌

@threadreaderapp unroll