,

27 tweets,

5 min read

Read on Twitter

Ok, I'll probably regret this, but given the poll results, I'm going to do a thread on why the inversion of the yield curve is seen as a potentially ominous sign and harbinger of eventual recession.

(Warning: I'm also going to make a few oversimplifications that bond market traders and MMT folks probably won't like, but such is life)

Ok, so here goes.

As you may have heard, the U.S. borrows a lot of money in the form of bond, which we refer to as Treasuries.

Treasuries are considered to be among the safest financial assets that exist in the world.

As you may have heard, the U.S. borrows a lot of money in the form of bond, which we refer to as Treasuries.

Treasuries are considered to be among the safest financial assets that exist in the world.

Now it's important to understand why they're considered to be "safe."

When you lend money, typically, there are two ways that that loan can go bad.

The first is that the borrower just doesn't pay you back...

When you lend money, typically, there are two ways that that loan can go bad.

The first is that the borrower just doesn't pay you back...

The second way you might regret making the loan is if the interest rate is too low, and inflation picks up. So say you lend to an entity at a rate of 5% per year. But inflation is at 10% per year, that's rough. You've locked your money into a money losing loan.

US Treasuries are considered to be safe, because the odds that the U.S. doesn't pay you back are virtually zero. There's essentially zero credit risk.

There is risk however from inflation. If you lend money to the government at 2%, you'll regret it if inflation goes to 4%, etc.

There is risk however from inflation. If you lend money to the government at 2%, you'll regret it if inflation goes to 4%, etc.

So when you lend money to the government, it's risk free only in the sense that there's no credit risk, and so you have just the risk of locking your money into a suboptimal investment. You'll get paid back, you'll just wish you had had your money in something else.

The U.S. government, like basically all governments as far as I know, borrows money across various maturities. It can sell bonds that pay back the lender in 3 months. It can sell bonds that pay back the lender in 5 years, 10 years, and longer.

Typically speaking, people demand more money to lend to the government for longer periods of time. That's because the future is highly uncertain. And if you're going to lock your money up for 10 years, you'll want to get paid more than if you lock your money up for just 1 year.

Think about it, who knows what's going to happen in the next 10 years? Maybe there will be a sudden bout of inflation. Maybe there will be an economic book like in the 1990s, and you'll wish you had your money in some other, higher-paying asset class. You just don't know.

The bottom line is that it's pretty easy to predict the short term (it'll probably look more or less like today) and it's hard to predict the far-out future. As such, typically people demand more compensation (a higher rate of interest) to lend money for the long term.

So that's the normal, intuitive state of affairs.

Now on a day to day basis, the price of bonds is always changing due to various things that happen.

For example, if good economic data comes out, people might perceive the future to be brighter. And they'll sell their bonds...

Now on a day to day basis, the price of bonds is always changing due to various things that happen.

For example, if good economic data comes out, people might perceive the future to be brighter. And they'll sell their bonds...

Remember, you might not want to have your money locked up in a safe asset during boom times. If things are good, you might dump your Treasuries. If enough people agree with your reassessment of the state of affairs, the yield on Treasuries will go up to entice new buyers.

Now let's try another scenario. Suppose a natural disaster hits in some part of the world where there's a lot of economic activity. People get nervous this will hit growth for a long time. People want safe assets that they know will pay them back. So they buy Treasuries.

In this scenario yields go down.

Or just suppose bad economic data comes out and people start to see the future as more grim. They see fewer growth opportunities. They see gluts of goods and falling prices. That also is likely to spur buying of safe assets and lower yields.

Or just suppose bad economic data comes out and people start to see the future as more grim. They see fewer growth opportunities. They see gluts of goods and falling prices. That also is likely to spur buying of safe assets and lower yields.

Now I'm eliding over an important fact, which is that the news catalyst doesn't axiomatically mean that yields have to rise or fall. What happens in reality is that the news is perceived as influencing the actions of the Federal Reserve.

So what happens is, if bad news comes out, people believe that that news will cause the Federal Reserve to hike rates less in the future than they previously had been expecting, and that's what causes long-term yields to fall.

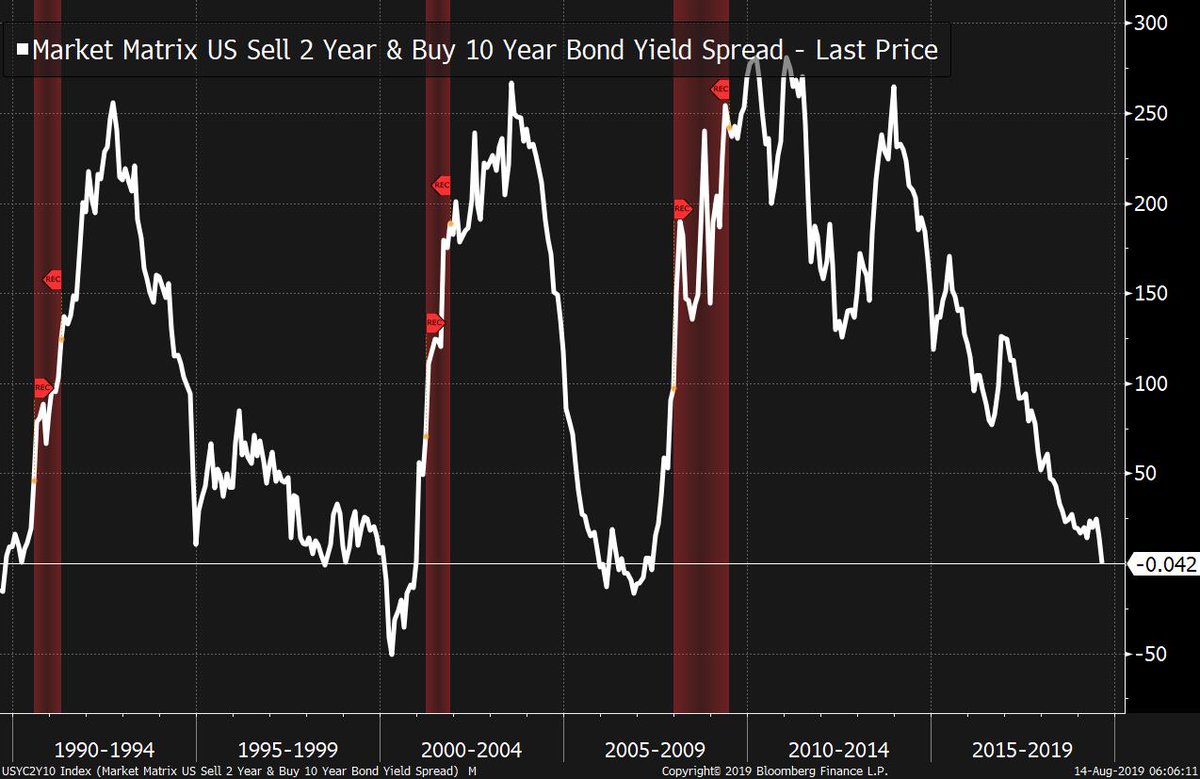

So this brings us to the inversion. As noted above, typically, investors will demand higher compensation for lending over a long period of time, due to the risks and opportunity costs of locking up their money.

But if the risks start to built. Economic data starts to slow. Fears mount about negative events happenig. Inflation starts to come in light and so on, this will have the effect of pushing down expectations of future Fed rate hikes, and push down yields.

Eventually, if you get to the point where the long-term rate falls below the short term rate (A convention is to compare the yield on the 10-year bond to the 2-year bond) and that signals that the market expects the Fed will be forced into a position where it must cut rates.

It's essentially the market predicting that enough bad things are happening that the Fed will be forced to cut.

It's also the market saying that the Fed's current monetary policy stance is overly restrictive, given conditions that are materializing in the real economy.

It's also the market saying that the Fed's current monetary policy stance is overly restrictive, given conditions that are materializing in the real economy.

In the past, this market signal -- that the Fed is overly restrictive and will be forced to cut rates -- has presaged an eventual recession, as indicated by the red bars.

So does the recent yield curve inversion necessarily signal recession?

Well, for one thing it's not inverted anymore, that happened very briefly yesterday, but it's not anymore.

Second, some argue that there are factors that make it different this time.

Well, for one thing it's not inverted anymore, that happened very briefly yesterday, but it's not anymore.

Second, some argue that there are factors that make it different this time.

For example, some argue that yields have been falling due to an unusual level of demand from pension funds or foreign buyers, and don't offer a real signal.

Also in the past, the inversion was more a direct result of the short end rising, as opposed to long-end falling.

Also in the past, the inversion was more a direct result of the short end rising, as opposed to long-end falling.

Furthermore, this has only happened a handful of times -- far from enough to signal any kind of statistical robustness.

Bottom line is that when you see rates at the long end fall below the short end, that historically has indicated market expectations that conditions will force the Fed to start cutting interest rates. And those conditions that force rate cuts tend to be correlated with recession.

Anyway, that's way over-simplified, and there are already people in my mentions calling me an idiot. But that's the basic concept of why an inversion is seen as ominous, why people are scrutinizing the Fed here, and why it heightens people's recession fears. /end