We talk a lot about #SaaS, and I'd like to present a framework I use to evaluate these types of companies.

It's important for SaaS to recoup upfront costs thru ongoing subscriptions.

I'll walk through my process, using Veeva Systems $VEEV as an example.

docs.google.com/spreadsheets/d…

It's important for SaaS to recoup upfront costs thru ongoing subscriptions.

I'll walk through my process, using Veeva Systems $VEEV as an example.

docs.google.com/spreadsheets/d…

Specifically, we're looking for Customer Lifetime Value (LTV) to exceed the Customer Acquisition Cost (CAC).

We want to see customers pay enough & stick around to justify the upfront sales & ongoing R&D.

If LTV > CAC, the company is generating profits for its shareholders.

We want to see customers pay enough & stick around to justify the upfront sales & ongoing R&D.

If LTV > CAC, the company is generating profits for its shareholders.

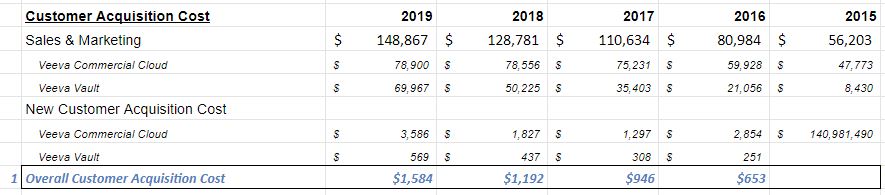

Veeva $VEEV spent $148m last year on Sales & Mktg to acquire 94 new customers.

So on average, its Customer Acquisition Cost (1) is $1.584 million.

[Note that this isn't perfect. Much of that sales spend went to current customers; but it's the best data we have available.]

So on average, its Customer Acquisition Cost (1) is $1.584 million.

[Note that this isn't perfect. Much of that sales spend went to current customers; but it's the best data we have available.]

But those customers also require ongoing R&D and overhead to keep them happy.

Veeva $VEEV spent $158m on R&D and $86m last yr across its 719 clients

On average, that's an ongoing R&D and Overhead burden (2) of $341k per customer per year.

Veeva $VEEV spent $158m on R&D and $86m last yr across its 719 clients

On average, that's an ongoing R&D and Overhead burden (2) of $341k per customer per year.

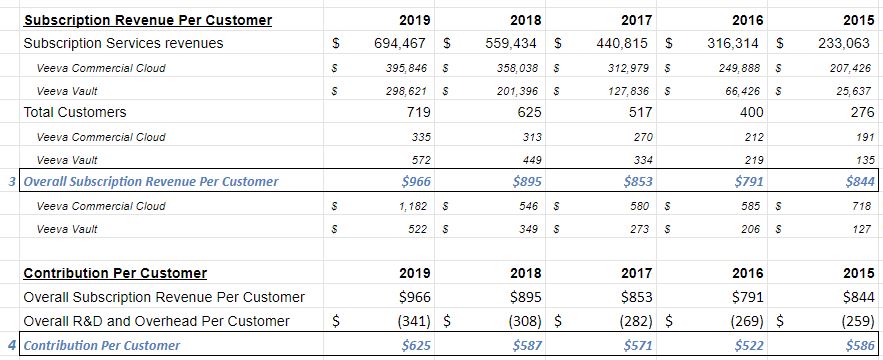

Veeva generated $694m in subscription revenue last yr, which is an avg per customer (3) of $966k.

Backing out R&D and Overhead, the "average" Contribution Per Customer (4) is $625k/yr.

Note: this doesn't include $VEEV's Professional Services revenue, which is also profitable.

Backing out R&D and Overhead, the "average" Contribution Per Customer (4) is $625k/yr.

Note: this doesn't include $VEEV's Professional Services revenue, which is also profitable.

We now make a few assumptions on customer churn rate & the discount rate to bring future subs to the present.

Using a Churn Rate of 4% & a Discount Rate of 10.5%, I derive a Customer LTV (5) of $5.46 million.

[There's sensitivity; if we double Churn to 8%, LTV becomes $4.2m]

Using a Churn Rate of 4% & a Discount Rate of 10.5%, I derive a Customer LTV (5) of $5.46 million.

[There's sensitivity; if we double Churn to 8%, LTV becomes $4.2m]

Now to the bottom line (almost done, I promise):

Subtracting that $1.58m acquisition cost from the $5.46m LTV gives a *Net Customer LTV* of $3.87m (6).

That's fantastic! Veeva's $VEEV avg customer is worth $3.8 million in present value, *even after* taking out all of the costs!

Subtracting that $1.58m acquisition cost from the $5.46m LTV gives a *Net Customer LTV* of $3.87m (6).

That's fantastic! Veeva's $VEEV avg customer is worth $3.8 million in present value, *even after* taking out all of the costs!

The moral of the story is unit economics really matters for #SaaS.

Not all growth is profitable & not all SaaS comps will be around in 10 yrs.

But look for quality. Compelling products create switching costs, which lead to high retention rates & yrs of recurring subscriptions.

Not all growth is profitable & not all SaaS comps will be around in 10 yrs.

But look for quality. Compelling products create switching costs, which lead to high retention rates & yrs of recurring subscriptions.

There are tons of additional resources, such as @RamBhupatiraju's link to SaaS 2.0 metrics & @TMFStoffel's great piece about how to invest in SaaS.

I've included both below. And my DMs are open, if you have specific questions.

I've included both below. And my DMs are open, if you have specific questions.

Alternate versions:

- If we use *Sub Gross Profit* rather than Sub Rev, Net Customer LTV is $2.4m

- If we also include Prof Svcs & use the Combined Gross Profit, Net CLTV is $2.9m

- If we only use Sub Gross Profit & apply 15% Churn (most conservative!), Net CLTV is still $900k

- If we use *Sub Gross Profit* rather than Sub Rev, Net Customer LTV is $2.4m

- If we also include Prof Svcs & use the Combined Gross Profit, Net CLTV is $2.9m

- If we only use Sub Gross Profit & apply 15% Churn (most conservative!), Net CLTV is still $900k