On high PE ratios or non-profitability of SaaS + other young growth companies -

Most of the hyper-growth companies in my portfolio either have (a) no earnings or (b) they are trading at triple digit PE ratios.

Before dismissing these businesses as potential investments,...

Most of the hyper-growth companies in my portfolio either have (a) no earnings or (b) they are trading at triple digit PE ratios.

Before dismissing these businesses as potential investments,...

2)...one might want to ascertain why these companies are still unprofitable and more importantly, why is the market willing to own them at such rich valuations.

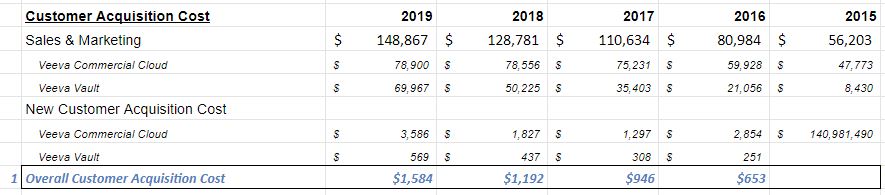

The reality is that these businesses are currently spending 30-40% of their revenues on Sales & Marketing...

The reality is that these businesses are currently spending 30-40% of their revenues on Sales & Marketing...

3) ... and they are doing so because they have figured out that the lifetime value of the acquired customers is way higher than the cost of acquisition of such customers.

So, they are spending cash hand over fist (and why not?) to grab as many customers as they possibly can...

So, they are spending cash hand over fist (and why not?) to grab as many customers as they possibly can...

4) In the case of SaaS, the gross margin of most of these companies is north of 70% and in order to become profitable, all they need to do is stop the spend on Sales & Marketing.

This will make them profitable right now but given the large TAMs and long growth runways, this...

This will make them profitable right now but given the large TAMs and long growth runways, this...

5)...will be a mistake.

Whether it is e commerce, fintech/payments or SaaS, these industries are very sticky (due to network effects, scale etc) so it makes perfect sense that the leading companies in this space are currently spending a lot of money to lock-in as many...

Whether it is e commerce, fintech/payments or SaaS, these industries are very sticky (due to network effects, scale etc) so it makes perfect sense that the leading companies in this space are currently spending a lot of money to lock-in as many...

6)...customers as they possibly can.

As long as the gross margins stay stable, these businesses demonstrate operating leverage (losses shrinking as % of revenue) and they are near FCF breakeven or FCF +ve, near-term lack of profitability isn't a concern IMHO.

As long as the gross margins stay stable, these businesses demonstrate operating leverage (losses shrinking as % of revenue) and they are near FCF breakeven or FCF +ve, near-term lack of profitability isn't a concern IMHO.

7) I may be wrong about this but in my view, e commerce marketplaces, fintech/payments and SaaS business models are very durable and they aren't very vulnerable to the ebbs and flows of the broad economy.

After all, these industries aren't relying on new demand creation,...

After all, these industries aren't relying on new demand creation,...

8) ...they are stealing existing demand from legacy operators. This is why despite a sluggish global economy, these businesses in my portfolio are growing by 30/40/50...or even 100%+ per annum.

Given their unheard of growth rates, it is hardly surprising that these companies..

Given their unheard of growth rates, it is hardly surprising that these companies..

9)...are selling at high valuations, especially when compared to the broad market.

As an investor in these companies, I'm comfortable with the current heavy cash outlays + losses so long as these businesses don't rely on the kindness of strangers

(external capital).

As an investor in these companies, I'm comfortable with the current heavy cash outlays + losses so long as these businesses don't rely on the kindness of strangers

(external capital).

10) So, these are some of the reasons why I've invested almost my entire capital in these high growth, unprofitable and 'overvalued' businesses.