1/ Portfolio Strategies for Volatility Investing (Campasano)

The degree of VIX futures contango "has been shown to hold predictive power over volatility returns. This study proposes a conditional strategy which allocates to market and volatility risk."

papers.ssrn.com/sol3/papers.cf…

The degree of VIX futures contango "has been shown to hold predictive power over volatility returns. This study proposes a conditional strategy which allocates to market and volatility risk."

papers.ssrn.com/sol3/papers.cf…

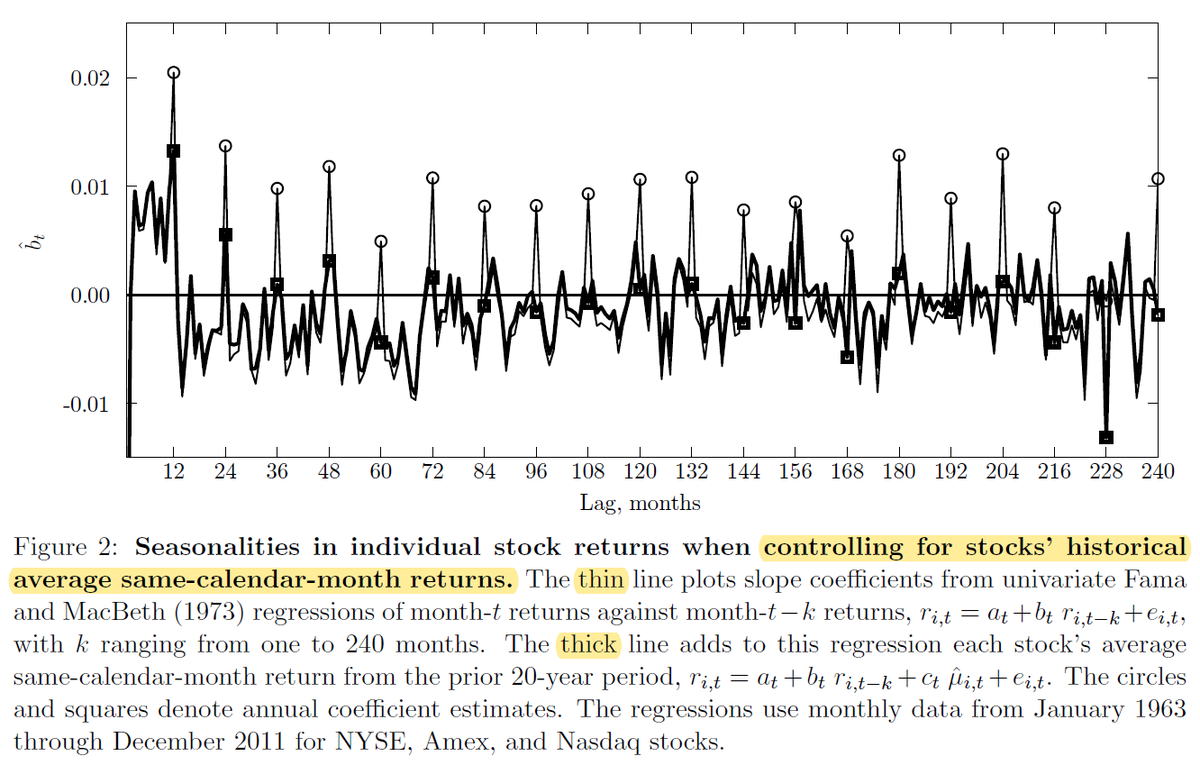

2/ "The futures curve is generally upward sloping [front two futures are in contango]. When volatility is low, the VIX premium is positive, while at higher levels of volatility, the premium is smaller or negative. The average VIX premium is positive for over 80% of the sample."

3/ "The constant-maturity VIX30 return is 2.53% when the premium is positive and -0.74% when negative. Across the entire sample, the daily return is -0.17%.

"A low (high) premium portends high (low) returns.... The VIX premium is predictive as to VIX futures returns."

"A low (high) premium portends high (low) returns.... The VIX premium is predictive as to VIX futures returns."

4/ This shouldn't come as a surprise: carry works basically everywhere because today's spot price is a better predictor of tomorrow's price than actual futures contract prices are.

(The expectation hypothesis fails for VIX futures as it does for bonds.)

(The expectation hypothesis fails for VIX futures as it does for bonds.)

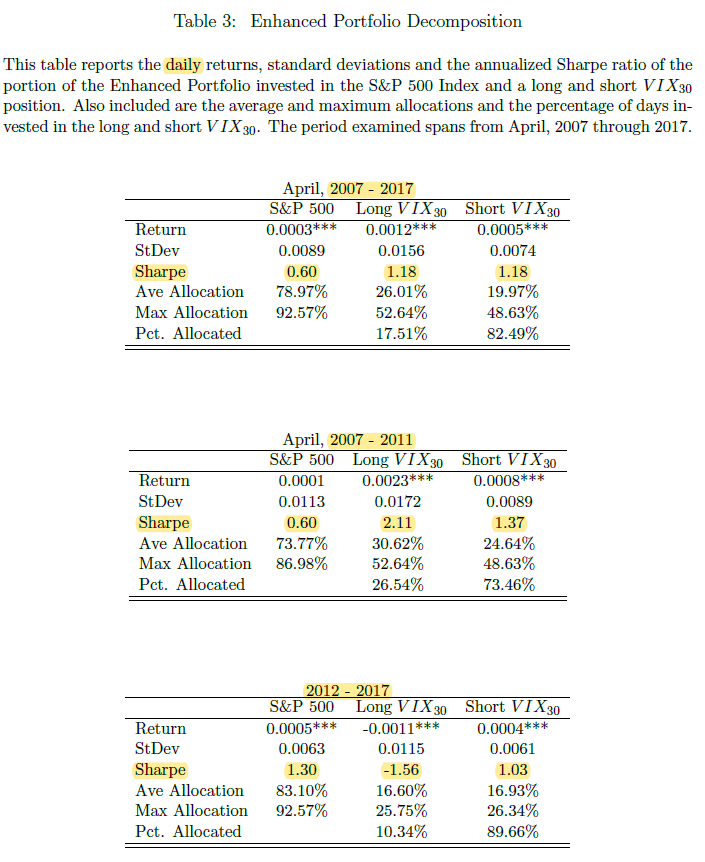

5/ The author constructs an Enhanced portfolio that allocates to the S&P 500 and to VIX30 using risk parity weights(out-of-sample volatility estimates).

Contango = short VIX30

Backwardation = long VIX30

Trading is delayed for a day after signals and volatility are calculated.

Contango = short VIX30

Backwardation = long VIX30

Trading is delayed for a day after signals and volatility are calculated.

6/ "While the performance of short VIX30 is fairly consistent across the two sub-samples, long VIX30 allocations posted positive returns during the first sub-sample but are unprofitable in the second."

7/ The Enhanced portfolio outperforms both the S&P 500 and various volatility-selling strategies in terms of tail metrics, Sharpe and Sortino ratios, and MPPM.

The outperformance is driven by long volatility allocations during the first half of the sample (2007-11).

The outperformance is driven by long volatility allocations during the first half of the sample (2007-11).

8/ "The performance during market and relative drawdowns echo the general return pattern of the Enhanced portfolio, outperforming the broad equity market during more difficult investment periods [higher market volatility] and mildly underperforming during more favorable periods."

9/ Three variants are also tested:

EnhancedLong uses only the backwardation signal and does not short volatility when the futures are in contango.

EnhancedShort uses only the contango signal.

Enhanced90 allocates 90% of the portfolio risk to the S&P 500 and 10% to L/S VIX30.

EnhancedLong uses only the backwardation signal and does not short volatility when the futures are in contango.

EnhancedShort uses only the contango signal.

Enhanced90 allocates 90% of the portfolio risk to the S&P 500 and 10% to L/S VIX30.

10/ Travis Johnson has a detailed treatment of the relationship between the implied volatility term structure and variance asset returns here: