1/ Thread with links to time-series autocorrelation research

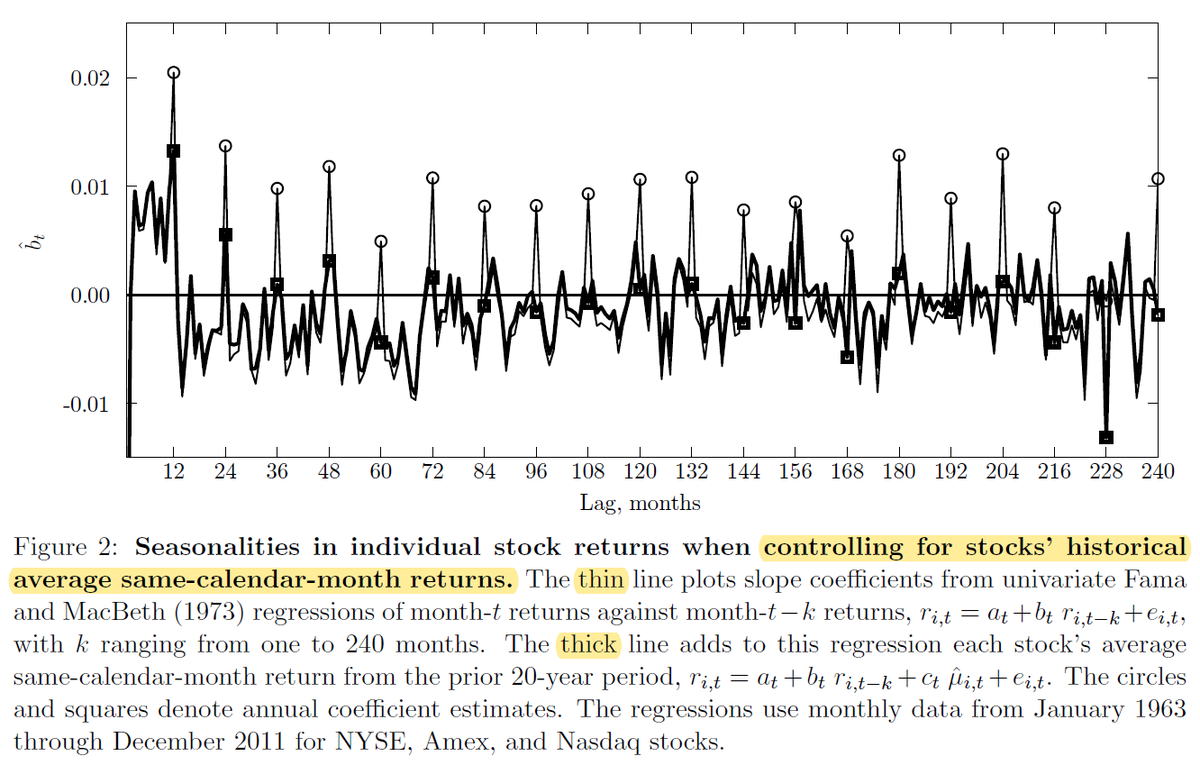

Return autocorrelations (individual stocks)

D’Souza, Srichanachaichok, Wang, Yao

Return autocorrelations (individual stocks)

D’Souza, Srichanachaichok, Wang, Yao

2/ Return autocorrelations for futures contracts

Moskowitz, Ooi, Pedersen

Moskowitz, Ooi, Pedersen

3/ Implied volatility autocorrelations

(Goyal and Saretto)

(Goyal and Saretto)

4/ *Volatility* autocorrelations for equities and bonds:

Harvey, Hoyle, Korgaonkar, Rattray, Sargaison, and Hemert

Harvey, Hoyle, Korgaonkar, Rattray, Sargaison, and Hemert

5/ Return autocorrelations for the traditional assets, alternative assets, and factors tested in the AQR paper Trends Everywhere

Babu, Levine, Ooi, Pedersen, and Stamelos

Babu, Levine, Ooi, Pedersen, and Stamelos

6/ Return correlations for factors

Gupta and Kelly

"The monthly AR(1) coefficient for the excess market return is 0.07 during our sample.

"The average for our factors is 0.11, and 50 of them have a larger AR(1) coefficient than the market."

Gupta and Kelly

"The monthly AR(1) coefficient for the excess market return is 0.07 during our sample.

"The average for our factors is 0.11, and 50 of them have a larger AR(1) coefficient than the market."