1/ Return Seasonalities (Keloharju, Linnainmaa, Nyberg)

* Stocks, L/S factors, commodities, and country indices have seasonality

* Factor seasonalities are comparable in size to factors themselves

* Stock seasonality may originate from factor seasonality

papers.ssrn.com/sol3/papers.cf…

* Stocks, L/S factors, commodities, and country indices have seasonality

* Factor seasonalities are comparable in size to factors themselves

* Stock seasonality may originate from factor seasonality

papers.ssrn.com/sol3/papers.cf…

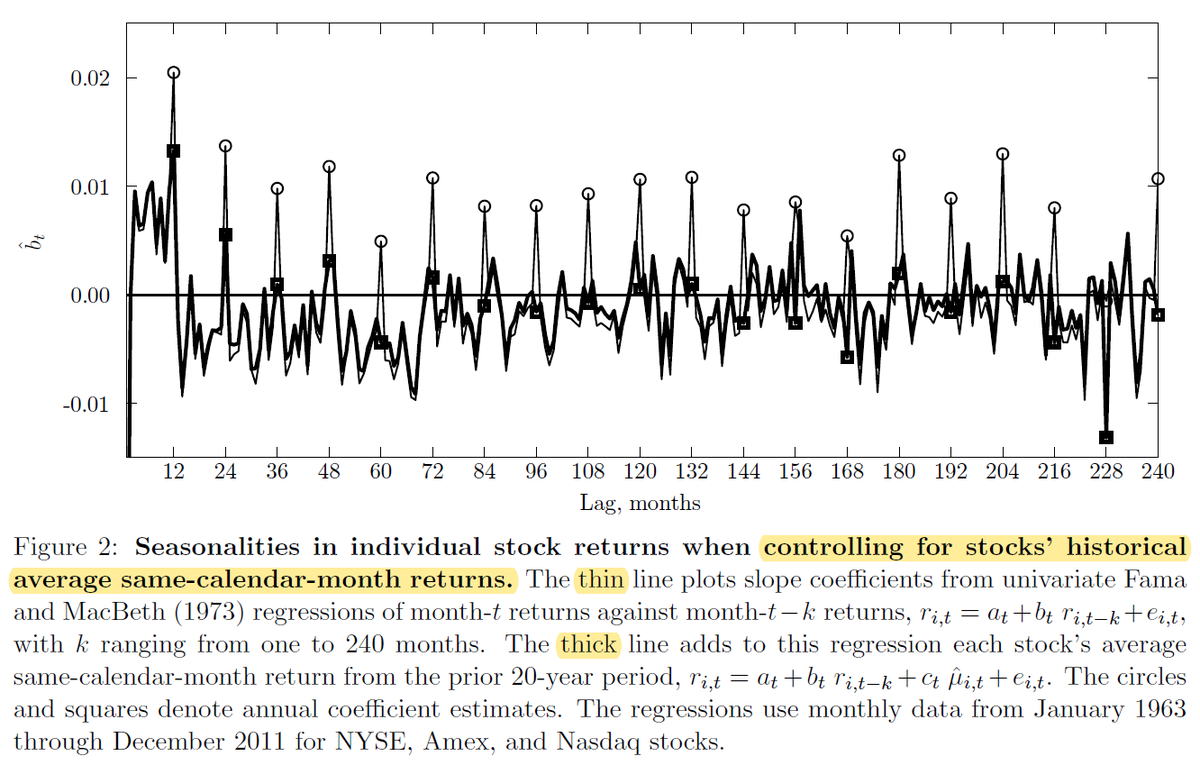

2/ "Positive peaks disrupt long-term reversals at every annual lag.

"This pattern, documented for many countries, disappears when regressions include stock-calendar month effects.

"Stocks do not 'repeat' shocks from the past; expected returns vary from calendar month to month."

"This pattern, documented for many countries, disappears when regressions include stock-calendar month effects.

"Stocks do not 'repeat' shocks from the past; expected returns vary from calendar month to month."

3/ "The average same-calendar-month return is a powerful signal of a stock's expected return in that month.

"Importantly, our results are specific to controlling for stock-*calendar month* variation in expected returns."

"Importantly, our results are specific to controlling for stock-*calendar month* variation in expected returns."

4/ "The surprising result is that this argument does not hold for *any* of the other portfolios [other than momentum]. The amount of seasonal variation in expected returns is so large that it completely swamps the unconditional differences."

5/ "Seasonalities in [factors] are as impressive as those in individual stocks.

"If the seasonalities in stock returns stem from seasonal variations in risk premiums, then a sort of stocks by their historical same-month returns groups stocks with similar factor loadings."

"If the seasonalities in stock returns stem from seasonal variations in risk premiums, then a sort of stocks by their historical same-month returns groups stocks with similar factor loadings."

6/ "Even though the seasonalities in stocks emanate from multiple risk factors, in time-series regressions a seasonality strategy constructed from a relatively small set of [factor] portfolios already explains half the profits of the individual-stock seasonality strategy."

7/ "Size, value, D/P, mkt β, and industry explain a total of 48% (SE = 10%) of the seasonalities in individual stock returns in the full sample.

"Given that our regressions control only for the *salient* variables correlated with seasonalities, 48% is a conservative estimate."

"Given that our regressions control only for the *salient* variables correlated with seasonalities, 48% is a conservative estimate."

8/ "Characteristics explain the seasonal patterns better at long lags than at short lags.

"Controlling for industry and size eliminates about half of the systematic risk associated with the strategy, leaving the remaining half to all other sources of systematic risk."

"Controlling for industry and size eliminates about half of the systematic risk associated with the strategy, leaving the remaining half to all other sources of systematic risk."

9/ More recently, Ehsani and Linnainmaa have found that stock momentum may originate from factor momentum.

Thinking of stocks as bundles of factor exposures might lead to other interesting findings as well.

Thinking of stocks as bundles of factor exposures might lead to other interesting findings as well.

10/ "Return seasonalities are highly significant in joint tests of 14 anomalies.

"Some anomaly strategies display seasonalities even though their unconditional average returns are not sig. ≠ zero." (size and Ohlson's O-score)

*Cross-sectional* factor seasonality works as well.

"Some anomaly strategies display seasonalities even though their unconditional average returns are not sig. ≠ zero." (size and Ohlson's O-score)

*Cross-sectional* factor seasonality works as well.

11/ Size is a particularly interesting case. It's "real" when its seasonality is considered (this paper).

Factor momentum also brings size back to life:

Quality does it too:

So the death of size may not be an open-and-shut case.

Factor momentum also brings size back to life:

Quality does it too:

So the death of size may not be an open-and-shut case.

12/ The authors bring up an interesting point about time-series and cross-sectional seasonality being different (p. 22). For seasonality, both exist, but that didn't *have* to be true.

Goyal and Jegadeesh examine similar questions for TS and CS momentum:

Goyal and Jegadeesh examine similar questions for TS and CS momentum:

13/ Seasonality returns don't seem to be explained by macroeconomic risk.

Unlike other anomalies, "seasonality in individual stock returns is *stronger* following periods of low sentiment. The avg difference between high and low sentiment is stat. indistinguishable from zero."

Unlike other anomalies, "seasonality in individual stock returns is *stronger* following periods of low sentiment. The avg difference between high and low sentiment is stat. indistinguishable from zero."

14/ "Seasonalities permeate the entire cross-section of U.S. stock returns. The patterns for other anomalies (momentum, net issuances, asset growth) are less robust."

A L/S strategy that trades seasonalities in commodities works as well as a one that does so for country indices.

A L/S strategy that trades seasonalities in commodities works as well as a one that does so for country indices.

15/ Day-of-the-week seasonalities also seem to exist:

16/ "Correlations between seasonality strategies are low, even within the U.S. market. Momentum strategies in those corners are profitable as well, but their corr. are much higher."

This leads to diversification benefits, esp. because seasonalities can be traded in large stocks.

This leads to diversification benefits, esp. because seasonalities can be traded in large stocks.