1/ Tax Benefits of Separating Alpha from Beta (Liberman, Sialm, Sosner, Wang)

"The turnover of a strategy that separates α from β is concentrated on the long-short component and enables the deferral of capital gains on the passive market component."

papers.ssrn.com/sol3/papers.cf…

"The turnover of a strategy that separates α from β is concentrated on the long-short component and enables the deferral of capital gains on the passive market component."

papers.ssrn.com/sol3/papers.cf…

2/ Monte Carlo simulated returns from a multifactor distribution, 500 stocks

5-year reversal (no skip-year), momentum (skip-month)

2% avg returns with 4% volatility

20% long-term tax rate

35% short-term tax rate

HIFO

Losses carried forward (not used to offset short-term gains)

5-year reversal (no skip-year), momentum (skip-month)

2% avg returns with 4% volatility

20% long-term tax rate

35% short-term tax rate

HIFO

Losses carried forward (not used to offset short-term gains)

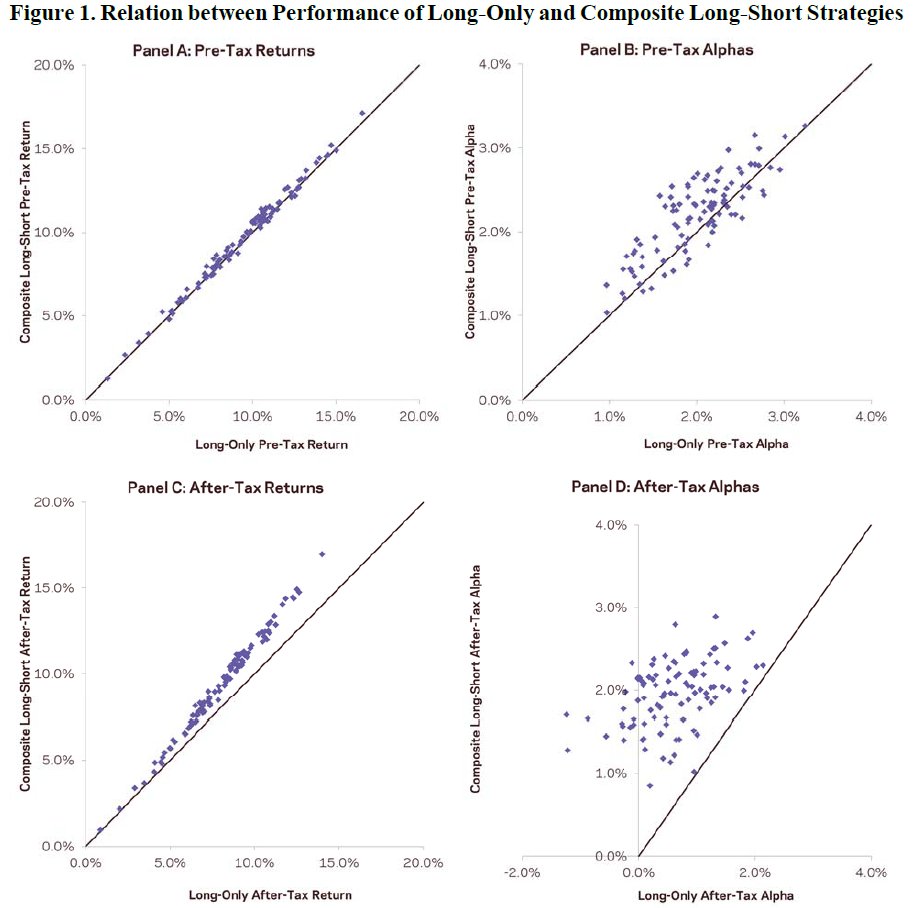

3/ "The composite strategy outperforms the long-only strategy in all 100 simulations after taxes."

(The lines shown are y=x. Dots that are above the lines represented simulations in which the composite L/S + passive index outperfomed the long-only alternative.)

(The lines shown are y=x. Dots that are above the lines represented simulations in which the composite L/S + passive index outperfomed the long-only alternative.)

4/ The composite strategy is slightly better before taxes because it doesn't neglect the information contained in short positions.

After taxes, the composite is much better: rebalancing factors (L/S) doesn't require realizing capital gains in the passive (market) portfolio.

After taxes, the composite is much better: rebalancing factors (L/S) doesn't require realizing capital gains in the passive (market) portfolio.

5/ When market returns are high, long-only has to realize capital gains when it rebalances.

The composite portfolio confines capital gain realizations to the L/S portion, leaving the passive portfolio alone.

("Leftover" losses are carried forward rather than harvested.)

The composite portfolio confines capital gain realizations to the L/S portion, leaving the passive portfolio alone.

("Leftover" losses are carried forward rather than harvested.)

6/ "The tax burden of the composite strategy is drastically smaller than that of the long-only strategy at all turnover levels. The maximum after-tax alpha (206 bps) for the composite is reached at a turnover of around 350%."

(This paper uses round-trip turnovers.)

(This paper uses round-trip turnovers.)

7/ The pre-tax information ratio is already higher for the composite strategy because it can short stocks to access the information in negatively ranked stocks.

The composite strategy's tax-efficient turnover increases its information ratio advantage when compared to long-only.

The composite strategy's tax-efficient turnover increases its information ratio advantage when compared to long-only.

8/ Higher turnover *and* higher market returns compound the problem for the long-only strategy, as it has to realize capital gains more often.

For the composite strategy, turnover is only exercised in the L/S portion, which is market-neutral and doesn't lead to higher taxes.

For the composite strategy, turnover is only exercised in the L/S portion, which is market-neutral and doesn't lead to higher taxes.

9/ Unlike the composite strategy, the long-only strategy has a tax burden even if factor returns are *negative* because the turnover induced by rebalancing leads to the realization of capital gains due to a general increase in the level of the stock market.

10/ These conclusions hold when the authors change assumptions about factor volatility and the correlation between value and momentum (one advantage of being able to use simulated results).

11/ Momentum is more tax-efficient than value due to the former's tendency to liquidate poor performers early. (Its pre-tax performance is worse because of the turnover constraint.)

Short-term reversal has *no* benefit after taxes (and before costs!) unless it can be done L/S.

Short-term reversal has *no* benefit after taxes (and before costs!) unless it can be done L/S.

12/ Increasing turnover has a greater benefit for momentum than it does for value.

There's also a multifactor diversification benefit:

Value+momentum after-tax information ratio, composite strategy (Table 2): 0.84

Value only (Table A.2): 0.36

Momentum only: 0.43

There's also a multifactor diversification benefit:

Value+momentum after-tax information ratio, composite strategy (Table 2): 0.84

Value only (Table A.2): 0.36

Momentum only: 0.43

13/ The conclusions hold under a broad range of tax scenarios, including for the L/S satellite mutual fund (assuming all gains are ordinary income and carry-forward losses are disallowed). (!)

If short-term losses are allowed to offset short-term gains from other strategies...

If short-term losses are allowed to offset short-term gains from other strategies...

14/ we now get a tax *benefit* of +0.3% for the composite strategy.... even though the L/S satellite strategy is tax-agnostic.

Two of the authors find similar results in an earlier paper:

+0.3% tax benefit (tax-agnostic)

+6.1% tax benefit (tax aware)

Two of the authors find similar results in an earlier paper:

+0.3% tax benefit (tax-agnostic)

+6.1% tax benefit (tax aware)

15/ These benefits assume that all of the short-term losses can be used to offset short-term gains from other trading strategies. (This may include harvesting a long-term gain in order to raise the tax basis so they can harvest a short-term loss later.)

16/ Loss harvesting may be more effective in volatile markets, which may help cushion a portfolio and potentially add some postive skewness to returns (Goldberg, Hand, Cai):

17/ Terminating an underperforming long-only manager is likely to lead to capital gains realizations because of the upward thrust of the market. This may cause investors to get "locked in" to these managers for tax reasons.

A satellite L/S manager doesn't lead to this problem.

A satellite L/S manager doesn't lead to this problem.

18/ Liquidating the portfolio (including the passive market component, which leads to the "bump" at the end) leads to higher final portfolio values for the composite strategy whether short-term losses can be used to offset short-term gains or whether the losses are lost forever.

19/ The authors re-run the simulations after including costs:

55bps fee for long-only

10bps passive + 2/20 active (volatility-scaled) + 100bps financing for composite

20bps round-trip transactions

Costs are higher for composite but not enough to overwhelm the tax benefits.

55bps fee for long-only

10bps passive + 2/20 active (volatility-scaled) + 100bps financing for composite

20bps round-trip transactions

Costs are higher for composite but not enough to overwhelm the tax benefits.

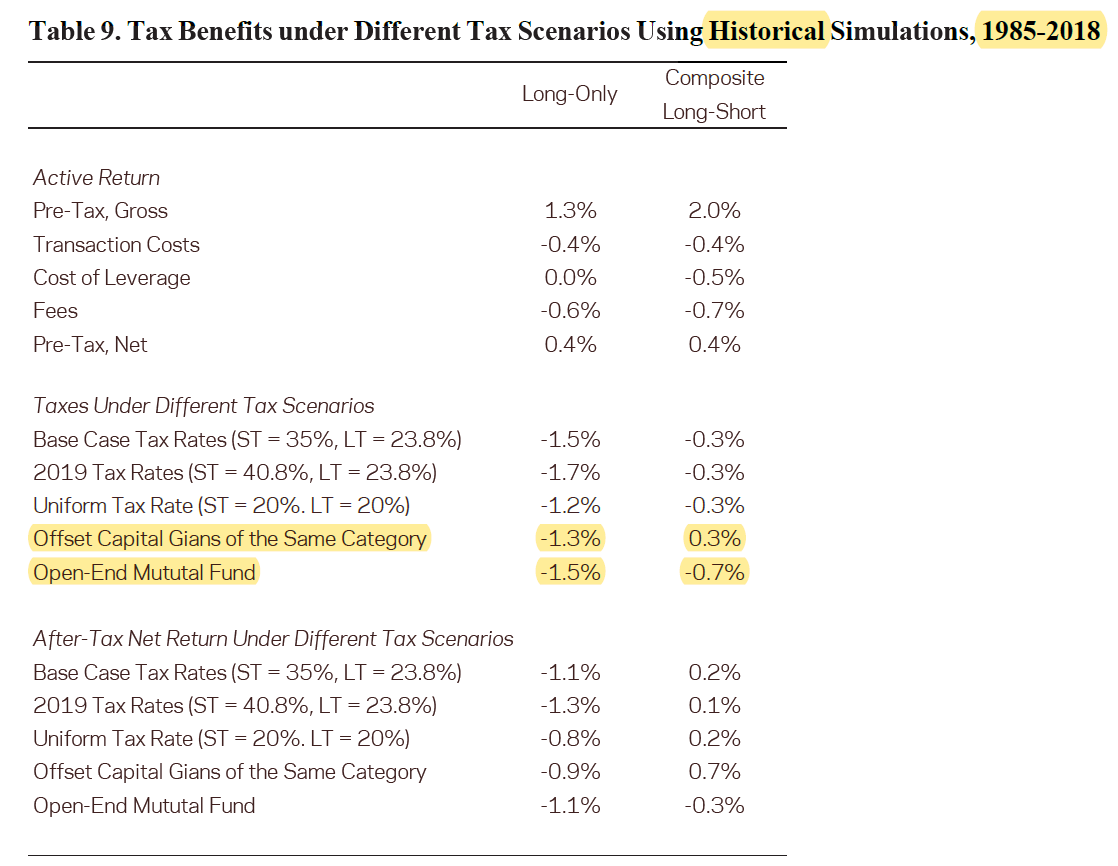

20/ The conclusions hold for real data (1985-2018).

The tax burden of the composite strategy is reduced to zero when an optimization that includes tax awareness is used to manage the portfolio.

(Losses are carried forward rather than being used to offset short-term gains)

The tax burden of the composite strategy is reduced to zero when an optimization that includes tax awareness is used to manage the portfolio.

(Losses are carried forward rather than being used to offset short-term gains)

21/ Relaxed-constraint (150/50) appears to offer almost as many tax benefits as core+satellite, but the authors suggest that conclusion may not hold if manager has to be replaced (resulting in portfolio liquidation).

It may also be easier to find L/S than 150/50 managers.

It may also be easier to find L/S than 150/50 managers.

22/ Conclusions using real data line up with conclusions using simulated data.

The composite strategy has a higher pre-tax return, higher costs, and much lower tax burden.

The +0.3% tax benefit (when short-term losses can offset short-term gains) is also present with real data.

The composite strategy has a higher pre-tax return, higher costs, and much lower tax burden.

The +0.3% tax benefit (when short-term losses can offset short-term gains) is also present with real data.

23/ Similarly, relative tax benefits (core+satellite > long-only) increase with market return and with turnover.

Most of the strategies in this paper assume tax-agnostic managers and can conceivably be applied by any investor willing to shift from long-only to core+satellite.

Most of the strategies in this paper assume tax-agnostic managers and can conceivably be applied by any investor willing to shift from long-only to core+satellite.