Investing is the study of how people behave with money. It’s not the study of finance. And behavior is hard to teach, even to really smart people.

The finance industry talks too much about what to do, and not enough about what happens in your head when you try to do it.

The finance industry talks too much about what to do, and not enough about what happens in your head when you try to do it.

Summary of 20 flaws, biases, and causes of bad behavior that pop up often when people deal with money

1. Earned success and deserved failure fallacy: A tendency to underestimate the role of luck and risk, and a failure to recognize that luck and risk are different sides of the same coin.

People’s lives are a reflection of the experiences they’ve had and the people they’ve met, a lot of which are driven by luck and chance. One cannot believe in risk without believing in luck. They are both the idea that things happen that influence outcomes more than effort.

2. Cost avoidance syndrome: A failure to identify the true costs of a situation, with too much emphasis on financial costs while ignoring the emotional price that must be paid to win a reward.

Every money reward has a price beyond the financial fee you can see and count. Accepting that is critical. Scott Adams once wrote: “One of the best pieces of advice I’ve ever heard goes something like this: If you want success, figure out the price, then pay it.”

3. Rich man in the car paradox.

The paradox of wealth is that people tend to want it to signal to others that they should be liked and admired. But in reality those other people bypass admiring you, because they use your wealth solely as a benchmark for their own desire to be liked and admired.

4. A tendency to adjust to current circumstances in a way that makes forecasting your future desires and actions difficult, resulting in the inability to capture long-term compounding rewards that come from current decisions.

Things change. And it’s hard to make long-term decisions when your view of what you’ll want in the future is so liable to shift.

5. Anchored-to-your-own-history bias: Your personal experiences make up maybe 0.00000001% of what’s happened in the world but maybe 80% of how you think the world works.

“Current investment beliefs depend on the realizations experienced in the past.”

-The Great Depression scared a generation for the rest of their lives.

-If you were born in 1970 the stock market went up 10-fold.

Keep that quote in mind when debating people’s investing views.

-The Great Depression scared a generation for the rest of their lives.

-If you were born in 1970 the stock market went up 10-fold.

Keep that quote in mind when debating people’s investing views.

6. Historians are Prophets fallacy: Not seeing the irony that history is the study of surprises and changes while using it as a guide to the future. An overreliance on past data as a signal to future conditions in a field where innovation and change is the lifeblood of progress.

The most important driver of anything tied to money is the stories people tell themselves and the preferences they have for goods and services. Those things don’t tend to sit still. They change with culture and generation. And they’ll keep changing.

The mental trick we play on ourselves is an over-admiration of people who have been there, done that, when it comes to money. Experiencing specific events does not necessarily qualify you to know what will happen next. In fact it rarely does. Experience leads to overconfidence.

7. The seduction of pessimism in a world where optimism is the most reasonable stance.

We’ve evolved to treat threats as more urgent than opportunities. Buffett says, “In order to succeed, you must first survive.”

Real optimists don’t believe that everything will be great. That’s complacency. Optimism is a belief that the odds of a good outcome are in your favor over time, even when there will be setbacks along the way.

8. Underappreciating the power of compounding, driven by the tendency to intuitively think about exponential growth in linear terms.

If I ask you to calculate 8+8+8+8+8+8+8+8+8 in your head, you can do it in a few seconds (it’s 72). If I ask you to calculate 8x8x8x8x8x8x8x8x8, your head will explode (it’s 134,217,728).

The danger here is that when compounding isn’t intuitive, we often ignore its potential and focus on solving problems through other means. Not because we’re overthinking, but because we rarely stop to consider compounding potential.

Good investing isn’t necessarily about earning the highest returns, the highest returns tend to be one-off hits that kill your confidence when they end. It’s about earning pretty good returns that you can stick with for a long period of time. That’s when compounding runs wild.

9. Attachment to social proof in a field that demands contrarian thinking to achieve above-average results.

The Berkshire Hathaway annual meeting in Omaha attracts 40,000 people, all of whom consider themselves contrarians. People show up at 4 am to wait in line with thousands of other people to tell each other about their commitment to not following the crowd. Few see the irony.

Real contrarianism is when your views are so uncomfortable and belittled that they cause you to second guess whether they’re right. Very few people can do that. But of course that’s the case. Most people can’t be contrarian, by definition.

10. An appeal to academia in a field that is governed not by clean rules but loose and unpredictable trends.

Harry Markowitz won the Nobel Prize in economics for creating formulas that tell you exactly how much of your portfolio should be in stocks vs bonds depending on your ideal level of risk. A few years ago the WSJ asked him how, given his work, he invests his own money. He replied:

“I visualized my grief if the stock market went way up and I wasn’t in it – or if it went way down and I was completely in it. My intention was to minimize my future regret. So I split my contributions 50/50 between bonds and equities.”

There are many things in academic finance that are technically right but fail to describe how people actually act in the real world.

11. The social utility of money coming at the direct expense of growing money; wealth is what you don’t see.

If you see someone driving a $200,000 car, the only data point you have about their wealth is that they have $200,000 less than they did before they bought the car. Or they’re leasing the car, which truly offers no indication of wealth.

When most people say they want to be a millionaire, what they really mean is “I want to spend a million dollars,” which is literally the opposite of being a millionaire. This is especially true for young people.

12. A tendency toward action in a field where the first rule of compounding is to never interrupt it unnecessarily.

When volatility is guaranteed and normal, but is often treated as something that needs to be fixed, people take actions that ultimately just interrupts the execution of a good plan. “Don’t do anything,” are the most powerful words in finance.

13. Underestimating the need for room for error, not just financially but mentally and physically.

Spreadsheets can model the historic frequency of big declines. But they cannot model the feeling of coming home, looking at your kids, and wondering if you’ve made a huge mistake that will impact their lives.

14. A tendency to be influenced by the actions of other people who are playing a different financial game than you are.

Few things matter more with money than understanding your own time horizon and not being persuaded by the actions and behaviors of people playing different games.

This goes beyond investing. How you save, how you spend, what your business strategy is, how you think about money, when you retire, and how you think about risk may all be influenced by the actions and behaviors of people who are playing different games than you are.

Personal finance is deeply personal, and one of the hardest parts is learning from others while realizing that their goals and actions might be miles removed from what’s relevant to your own life.

15. An attachment to financial entertainment due to the fact that money is emotional, and emotions are revved up by argument, extreme views, flashing lights, and threats to your wellbeing.

Because finance is entertaining in a way other things – orthodontics, gardening, marine biology – are not. Money has competition, rules, upsets, wins, losses, heroes, villains, teams, and fans that makes it tantalizingly close to a sporting event.

But it’s even an addiction level up from that, because money is like a sporting event where you’re both the fan and the player, with outcomes affecting you both emotionally and directly.

Which is dangerous.

It helps, when making money decisions to constantly remind yourself that the purpose of investing is to maximize returns, not minimize boredom. Boring is perfectly fine.

It helps, when making money decisions to constantly remind yourself that the purpose of investing is to maximize returns, not minimize boredom. Boring is perfectly fine.

16. Optimism bias in risk-taking, or “Russian Roulette should statistically work” syndrome: An over attachment to favorable odds when the downside is unacceptable in any circumstance.

The idea is that you have to take risk to get ahead, but no risk that could wipe you out is ever worth taking. Leverage is the devil here. It pushes routine risks into something capable of producing ruin.

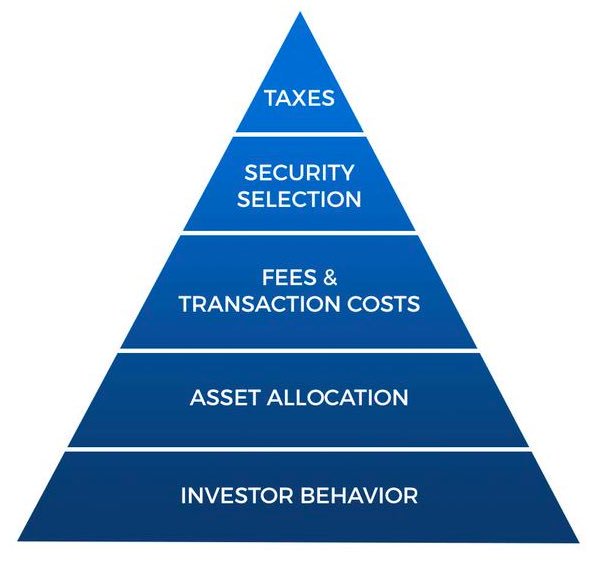

17. A preference for skills in a field where skills don’t matter if they aren’t matched with the right behavior.

There is a hierarchy of investor needs, and each topic here has to be mastered before the one above it matters:

18. Denial of inconsistencies between how you think the world should work and how the world actually works, driven by a desire to form a clean narrative of cause and effect despite the inherent complexities of everything involving money.

Everyone just believes what they want to believe, even when the evidence shows something else. Stories over statistics.

Accepting that everything involving money is driven by illogical emotions and has more moving parts than anyone can grasp is a good start to remembering that history is the study of things happening that people didn’t think would or could happen.

19. Political beliefs driving financial decisions, influenced by economics being a misbehaved cousin of politics.

The point is not that politics don’t influence the economy. But the reason this is such a sensitive topic is because the data often surprises people, which itself is a reason to realize that the correlation between politics and economics isn’t as clear as you’d think it is.

20. The three-month bubble: Extrapolating the recent past into the near future, and then overestimating the extent to which whatever you anticipate will happen in the near future will impact your future.

Believing that what just happened will keep happening shows up constantly in psychology. We like patterns and have short memories.

Every big financial win or loss is followed by mass expectations of more wins and losses.

Every big financial win or loss is followed by mass expectations of more wins and losses.

Summary: there is no easy path when it comes to investing.

If there’s a common denominator in these, it’s a preference for humility, adaptability, long time horizons, and skepticism of popularity around anything involving money. Be prepared to roll with the punches.

If there’s a common denominator in these, it’s a preference for humility, adaptability, long time horizons, and skepticism of popularity around anything involving money. Be prepared to roll with the punches.