The Trump administration has issued regulations that pave the way for an expansion of "short-term" insurance plans that can last up to 36 months and don't follow any of the ACA's rules. A few thoughts to follow.

cms.gov/Newsroom/Media…

cms.gov/Newsroom/Media…

The short-term plans the Trump administration is expanding can deny coverage to people with pre-existing conditions, do not have to cover the ACA's essential benefits, and can cap coverage on an annual basis.

The Trump administration cannot eliminate the ACA's insurance rules. Instead, they are using short-term insurance plans to create a parallel market of insurance plans that do not have to follow any of the ACA's rules.

We reviewed short-term insurance plans on the market and found they often don't cover maternity, prescription drugs, substance abuse, or mental health. That was also the case for individual insurance plans before the ACA required these benefits.

kff.org/health-reform/…

kff.org/health-reform/…

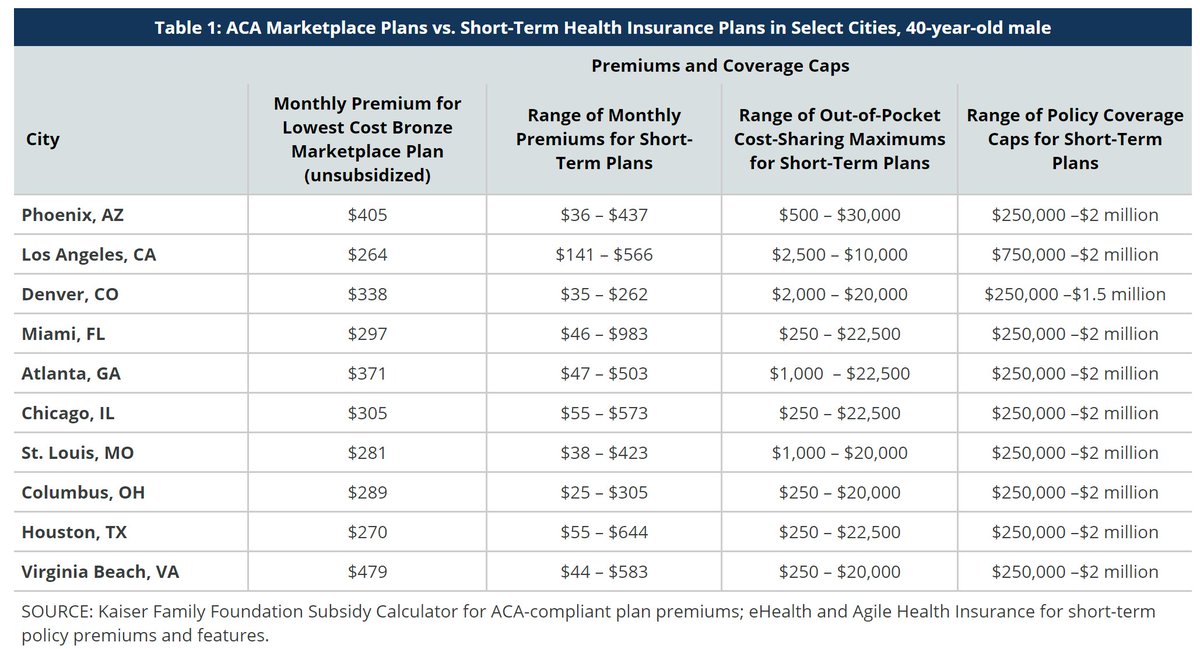

Short-term insurance plans have much lower premiums than ACA-regulated plans, because they exclude people with pre-existing conditions and don't have the same benefits. That could be attractive to people who buy their own insurance and are healthy.

kff.org/health-reform/…

kff.org/health-reform/…

Plans with ACA consumer protections will still exist. But, the premiums for those plans will rise as short-term plans cherry pick healthy people. ACA enrollees eligible for subsidies will be protected, but middle-class people with pre-existing conditions will feel the full brunt.

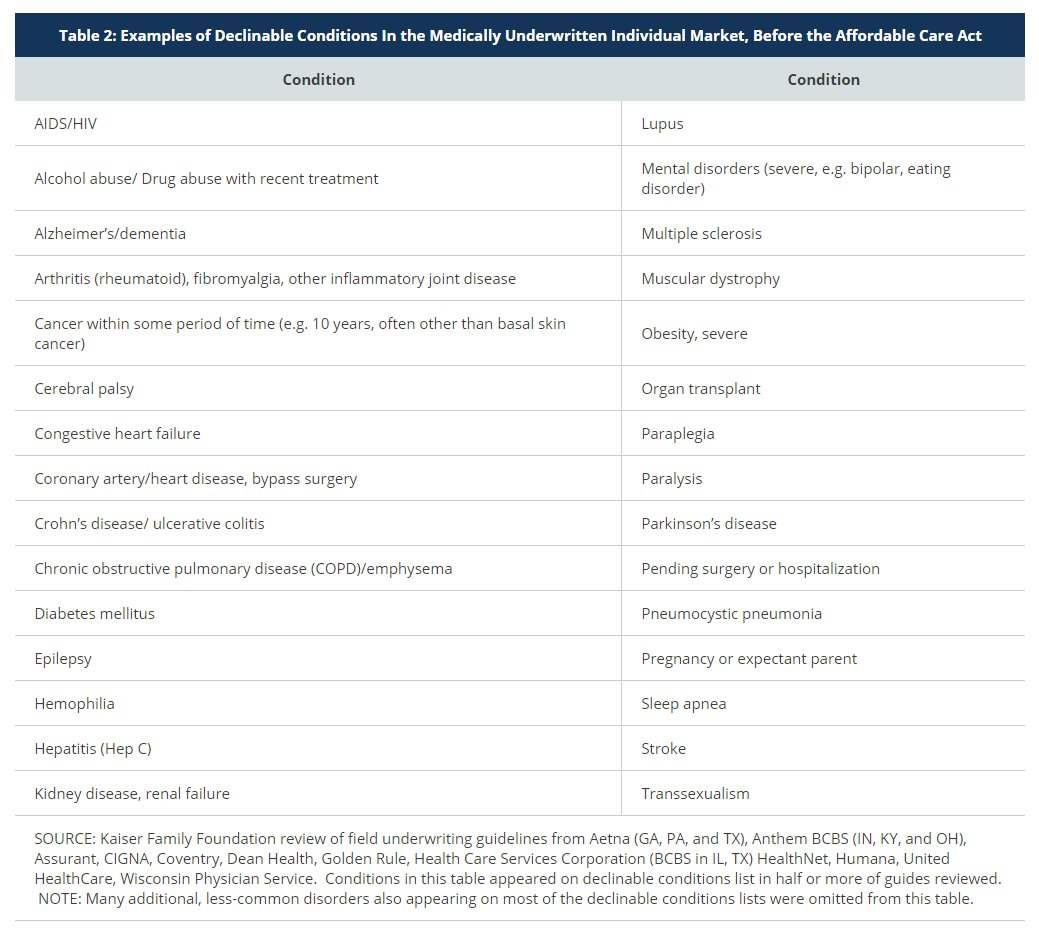

27% of non-elderly adults have a pre-existing condition that would have led to a denial of coverage before the ACA, or now under short-term insurance plans being expanded by the Trump administration.

kff.org/health-reform/…

kff.org/health-reform/…

Short-term insurance plans do not have to follow the ACA's loss ratio rule, which says that 80% of the premium go to medical claims and no more than 20% to administration and profit.

In short-term insurance plans, it's not uncommon for as much of the premium to go for profit, marketing, and overhead as for paying medical claims. Here's one example.

The Trump administration is allowing insurers to renew short-term insurance plans for up to 3 years. This offers some protection for people, but not as much as it might seem because it's at the discretion of insurance companies.

People who are healthy will likely be able to buy new short-term policies at renewal for a lower premium, while people who get sick will see bigger premium increases and might just switch back to ACA-regulated plans.

There are two reasons short-term plans will be more attractive next year.

1. They are not so short-term anymore with the new regulation.

2. There will no longer be an individual mandate penalty, which previously applied to people buying short-term plans.

1. They are not so short-term anymore with the new regulation.

2. There will no longer be an individual mandate penalty, which previously applied to people buying short-term plans.

One really important thing to remember about the new Trump administration short-term insurance plans: States can still regulate them, limit them, or prohibit them entirely.

Enrollment in ACA plans among people not eligible for subsidies has declined in response to recent premium increases. That will likely accelerate with the Trump administration's expansion of short-term plans, at least among people who are healthy.

kff.org/health-reform/…

kff.org/health-reform/…

As with everything in health policy, the new short-term regulation poses trade-offs: Lower premiums for healthy middle-class people not eligible for subsidies, but higher premiums for those with pre-existing conditions.

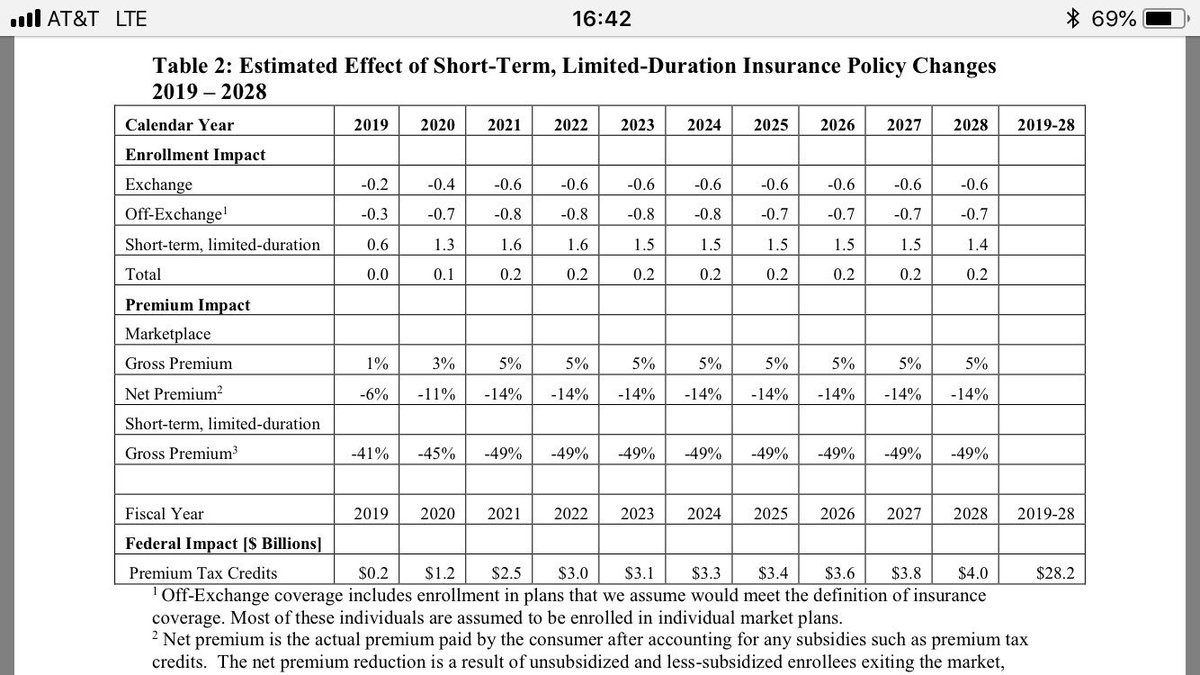

Because short-term plans will siphon off healthy people, ACA plans will be left with a sicker pool and higher premiums. This in turn will increase the federal cost of premium subsidies. The Trump administration estimates the increased federal cost will total $28.2 billion.

Short-term insurance plans will have lower premiums than ACA-regulated plans, as the Trump administration has said. That's because they'll exclude people with pre-existing conditions. The debate over the ACA seems to always come back to people pre-existing conditions.