,

28 tweets,

8 min read

Read on Twitter

1/ PART 1 of 4

Let's talk about investing expectations.

Investors typically expect 10% returns on their portfolio. Most pension fund expect around 8%.

** Millennials expect 11.7% per year. And 20% of you expect 20%+ returns.

schroders.com/en/sysglobalas…

Let's talk about investing expectations.

Investors typically expect 10% returns on their portfolio. Most pension fund expect around 8%.

** Millennials expect 11.7% per year. And 20% of you expect 20%+ returns.

schroders.com/en/sysglobalas…

2/ We like to say that is people having…..somewhat unrealistic expectations...

3/ So why do people expect 10% returns?

Simply because that’s what US stocks have returned in the past.

Simply because that’s what US stocks have returned in the past.

4/ But does it make sense to expect stocks to return what they did in the past?

5/ Lets channel John Bogle with his 30 year old formula for stock return expectations

(@WSJ summary here wsj.com/articles/jack-…)

(@WSJ summary here wsj.com/articles/jack-…)

6/ While it looks complicated, the formula is simple:

Rt =D0 +Gt +∆P/Et

10 year annualized stock returns = dividend yield + dividend growth + change in valuations

Rt =D0 +Gt +∆P/Et

10 year annualized stock returns = dividend yield + dividend growth + change in valuations

7/ historically that has worked out to roughly:

10% = 4.8% + 4.9% + 0.3%

10% = 4.8% + 4.9% + 0.3%

8/ What about going forward? You can plug in today’s numbers. We’ll assume today’s dividend yield, and assume dividend growth the same as history, and no valuation changes.

6.9% = 2.0% + 4.9% + 0%

6.9% = 2.0% + 4.9% + 0%

9/ (Quick nerd alert: Dividend yield may seem artificially low due to the onset of buybacks over the past 30 years. However that has also resulted in higher dividend growth, but, we’ve also seen lower inflation than history so a bit of a wash)

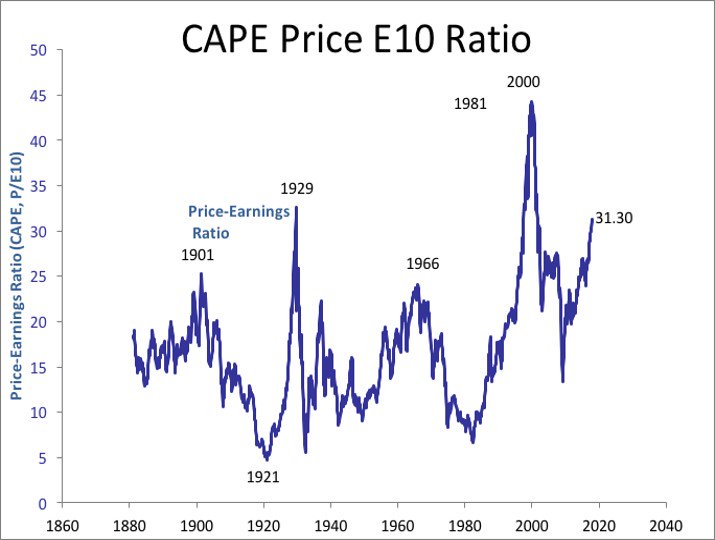

10/ But what about the valuation term? Y’all know I like using long term valuations like the 10-year PE (also known as the Shiller CAPE ratio). Here’s a historical chart from @RobertJShiller :

11/ Now, for some reason people’s brains start to meltdown where I bring up the CAPE ratio. This is their usual reaction.

12/ But most valuation metrics *should* agree, particularly at extremes, as they are blunt tools.

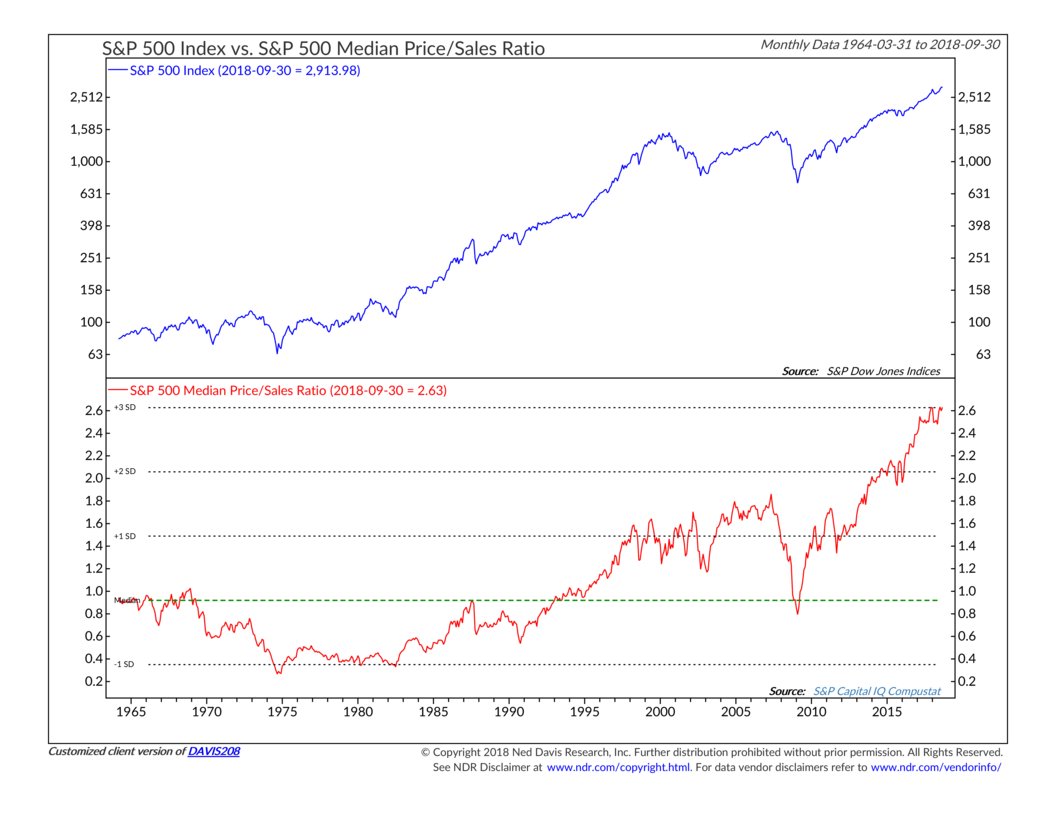

Here is a @NDR_Research chart that looks at median price-to-sales for the S&P 500, which currently is all time highs:

Here is a @NDR_Research chart that looks at median price-to-sales for the S&P 500, which currently is all time highs:

13/ But does value make a difference? If you examined the starting characteristics for the three best, and worst, starting points in history, you can get a little more color.

14/ The best had monster 10 year returns of ~20% per year (that’s @WarrenBuffett territory). Fat 5% yield and low 11 CAPE ratio to start the period. But note the period ended with valuations doubling resulting in a 9% per year tailwind of people willing to pay higher multiples.

15/ If you were unlucky and started investing at the worst possible times? Flat returns for a decade, lower starting yield, and a higher starting valuation that then halved over the period resulting in a big multiple compression headwind for a decade of -7%!

16/ Now, we always say you need to think in probabilistic terms. Understand what is most likely to happen but also account for what “could” happen. So, you can type in future valuation multiples 10 years out to estimate future returns.

17/ We'll use today's 2% dividend yield and historical growth rates.

If valuations just head back to normal (long term average of 17 and low inflation average of 21) you have stock returns of about 1-3% per year for a decade. Meh. Not negative, not a bubble, but not exciting…

If valuations just head back to normal (long term average of 17 and low inflation average of 21) you have stock returns of about 1-3% per year for a decade. Meh. Not negative, not a bubble, but not exciting…

18/ You should also prepare for the possibility that valuations may sail through the average to points we have seen before of CAPEs of 5 and 10 that would results in returns of -10% to -4% per year. Ugh. Nasty, but unlikely.

19/ You could also see valuations stay flat, and receive about 7% returns. But what if valuations go back to the highest they’ve ever been in the US (CAPE of 45 on Dec 1999)? Well that gets you to 10% annual returns.

20/ Notice the problem here. Investors expect 10% returns. For that to happen you either need unbelievable earnings and dividend growth, or you need valuations to go back to the highest they’ve ever been in history…JUST TO MEET EXPECTATIONS.

21/ Now we’ve seen higher valuations globally outside the US where some countries have hit 60 -90 CAPE ratios. Most famously Japan in the 1980s. But, that is even less likely, but still POSSIBLE.

22/ Most every other quantitative research shop like @AQRCapital , @RA_Insights, GMO etc also expect low returns. Resources here:

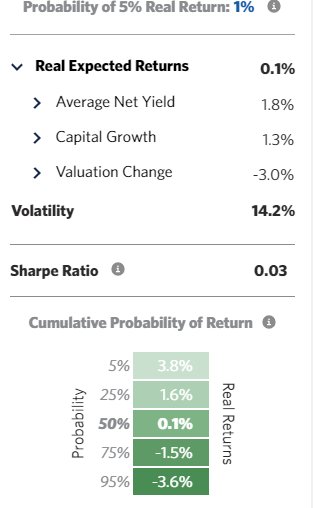

23/ @RA_Insights frames it nicely with this visual (note these are real returns after inflation). They estimate a 1% change of achieving historical 5% real returns....:

24/ While US stocks have more moving pieces, US government bonds should return approximately their yield for the next decade, or about 3%.

25/ So notice that if US stocks and US bonds are priced to return about 3%, that is a setup for major investor disappointment. You can’t even add 3% and 3% together to get 8-10% (that’s a joke btw).

26/ So what’s the solution? Perhaps?

(This joke was funnier in January).

(This joke was funnier in January).

27/ First, investors need to take their medicine. Lower your expectations, spend less, and save more (that’s not bad advice anyway)

28/ But we do have some ideas to improve upon this dreary scenario. In part 2/4 in this tweetstorm we’ll look at possible solutions to help….will post the next installment tomorrow...