,

9 tweets,

4 min read

Read on Twitter

Indeed wonderful graphs: China is far more integrated into the global trading network than the global banking network.

Personally think that is a good thing, too many risks inside China.

But also don't think it immunizes China from all responsibility for the crisis

(1/x)

Personally think that is a good thing, too many risks inside China.

But also don't think it immunizes China from all responsibility for the crisis

(1/x)

China tightly controlled bank flows before the crisis. That isn't the place to look for China's pre-crisis financial integration with the world.

The real question is how China's large bond purchases impacted global markets, and the decisions taken by global banks.

(2/x)

The real question is how China's large bond purchases impacted global markets, and the decisions taken by global banks.

(2/x)

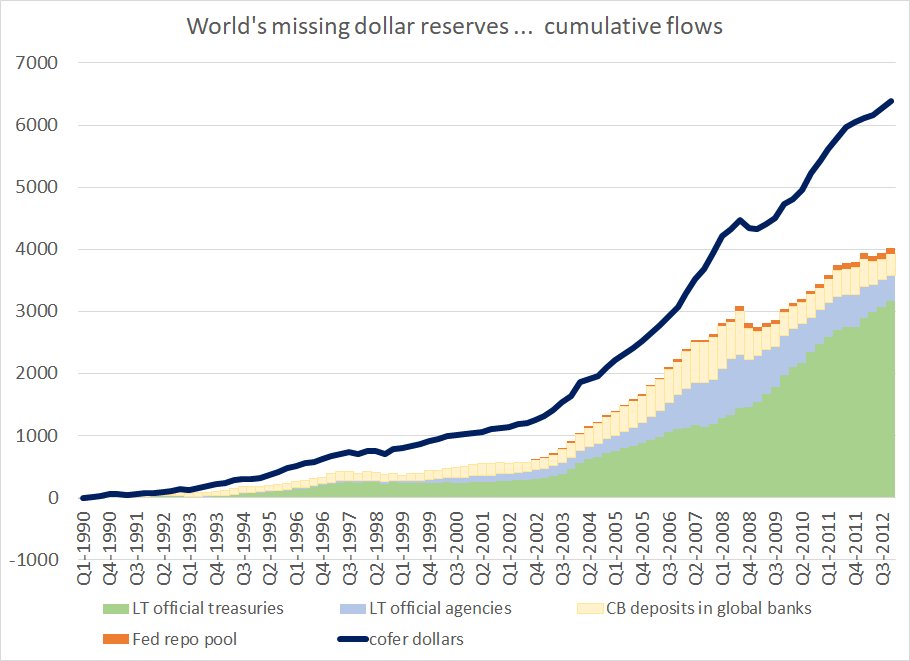

The distortion came because dollar reserve growth (at the time) far exceeded Treasury issuance. And China bears some responsibility for the global rise in reserves b/c other EMs didn't want to appreciate v China.

(3/x)

(3/x)

That's when Treasuries really where in short supply v global reserves --

Some of the demand was met by Agencies, but when Agency issuance was restrained, China's flows created incentives for the creation of synthetic safety.

(4/x)

Some of the demand was met by Agencies, but when Agency issuance was restrained, China's flows created incentives for the creation of synthetic safety.

(4/x)

And a lot of the excess demand for dollar assets from reserve managers spilled into global funding markets for banks. Not necessarily from China directly, but from someone. Agencies and CB deposits account for a large share of the "visible" growth in reserve assets.

(5/x)

(5/x)

even if you take the view (as I do) that the official US data likely undercounts true purchases of Treasuries and Agencies v CBs (and by private actors who raise USD via swaps with reserve managers), there was a big run up in CB funding for global banks

(6/x)

(6/x)

bottom line: China's impact on the global financial system was indirect. Need to ask why cross border bank flows surged at the same time as reserve growth globally surged, and what (if anything) connects them ...

(7/x)

cfr.org/blog/three-sud…

(7/x)

cfr.org/blog/three-sud…

I have a paper on all this coming soon (I hope!)

the scale of the flows (official and private) in the 03 to 07 period really stands out, and I don't think it is totally unrelated to the simultaneous surge in Chinese and EM reserve growth.

(8/x)

the scale of the flows (official and private) in the 03 to 07 period really stands out, and I don't think it is totally unrelated to the simultaneous surge in Chinese and EM reserve growth.

(8/x)

Last point.

While cross border links to Chinese banks are still small absolutely, they have increased significantly in the last 10ys. China's BoP data suggests China's banks have become significant net funders to the world in the last 5ys.

Nothing stays constant.

While cross border links to Chinese banks are still small absolutely, they have increased significantly in the last 10ys. China's BoP data suggests China's banks have become significant net funders to the world in the last 5ys.

Nothing stays constant.