,

45 tweets,

18 min read

Read on Twitter

Uber S-1 thoughts:

-AWS for transportation is its final form

-It's a modern day temp agency; driver churn is 3-5x below industry avg

-Eats cities profitable in 4-6 quarters, aggressive expansion impacted 2H‘18, 40% of users are new to Uber, and is a wedge into last mile delivery

-AWS for transportation is its final form

-It's a modern day temp agency; driver churn is 3-5x below industry avg

-Eats cities profitable in 4-6 quarters, aggressive expansion impacted 2H‘18, 40% of users are new to Uber, and is a wedge into last mile delivery

If you’re reading this, I’m assuming you’ve read other Uber S-1 takes. We all knew Uber was burning cash, but a lack of cohort data (both drivers and riders), and its core business metrics collapsing to end 2018, was surprising.

Like most US companies, the US and developed Europe are likely Uber’s cash cows, but international revenue helps cover overhead, and can be incremental cash flow.

This a great deep dive comparing Uber and Lyft’s US vs International numbers:

This a great deep dive comparing Uber and Lyft’s US vs International numbers:

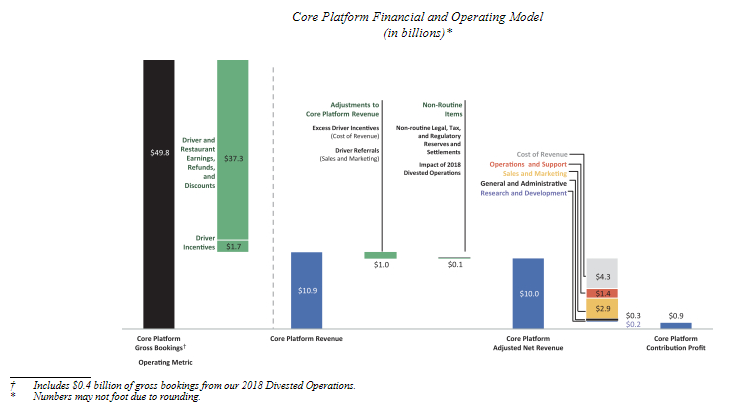

Here's a visual Uber gave to show how its core product (excluding a chunk of overhead costs) was profitable in 2018.

This "we're profitable if you exclude overhead" metric is common for companies in Uber's position of growing fast and looking to tap the capital markets.

This "we're profitable if you exclude overhead" metric is common for companies in Uber's position of growing fast and looking to tap the capital markets.

These “Core Platform Adjusted Net Revenue" and Contribution Margin numbers, which basically show Uber’s aggregate unit economics (excluding excessive, temporary payments spent to on-board new drivers, as determined by Uber), paint a picture of its business nose-diving to end 2018

What happened to Uber's metrics in 2H'18?

Without cohort metrics, I combined historical disclosures with the S-1 (orange are extrapolations).

We see how Rides and Eats expanded over time, and specifically accelerated through 2018.

(will respond to this tweet wit sources)

Without cohort metrics, I combined historical disclosures with the S-1 (orange are extrapolations).

We see how Rides and Eats expanded over time, and specifically accelerated through 2018.

(will respond to this tweet wit sources)

Graphing the data:

- Uber Eats expanded from 200 to 500 cities in 2018, and nearly 2x’ed from 280 to 500 in Q3/Q4 2018

- It takes 4-6 quarters for new Eats cities to become profitable

- Eats gets Uber into new markets (where ride hailing is currently regulated/uneconomical)

- Uber Eats expanded from 200 to 500 cities in 2018, and nearly 2x’ed from 280 to 500 in Q3/Q4 2018

- It takes 4-6 quarters for new Eats cities to become profitable

- Eats gets Uber into new markets (where ride hailing is currently regulated/uneconomical)

Numbers from old press don't back out divestitures, so lower historical numbers further emphasize:

Uber Eats rapid expansion in 2H ‘18 had a material impact, new Eats cities are profitable in 12-18 months, and the trend suggests 150-180 cities were profitable at the end of 2018.

Uber Eats rapid expansion in 2H ‘18 had a material impact, new Eats cities are profitable in 12-18 months, and the trend suggests 150-180 cities were profitable at the end of 2018.

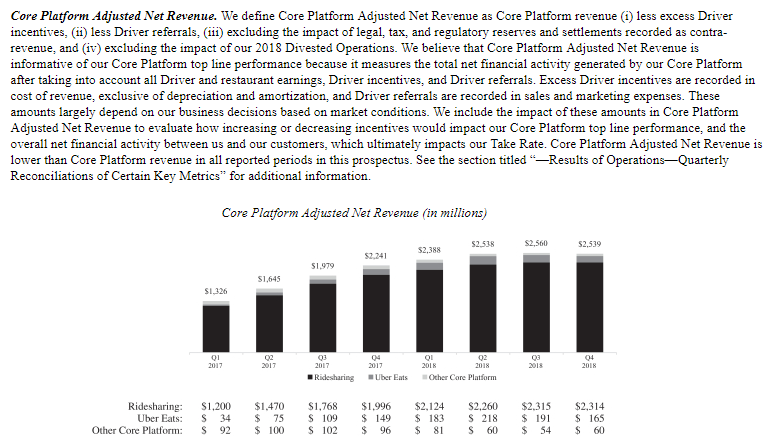

Here’s an example Uber provides showing how new cities impact its financials, specifically by depressing "adjusted net revenue":

As gross bookings increases $10, net revenue actually decreases $1 (a negative take rate) as it temporarily overpays to build up a network of drivers.

As gross bookings increases $10, net revenue actually decreases $1 (a negative take rate) as it temporarily overpays to build up a network of drivers.

This reconciliation of contribution profit by quarter (key metric), which shrunk as growth spending ramped up to end 2018, highlights that if you take out self-driving R&D and other one-time/non-cash expenses, Uber only lost $61M in Q1 2018 (even as it opened new cities).

Why did Uber burn so much cash in 2H 2018?

"We decreased CAC by burning cash faster. We acquired more users in 2 weeks than if we burned the same amount of cash over 6 months"

medium.com/swlh/whats-so-…

"We decreased CAC by burning cash faster. We acquired more users in 2 weeks than if we burned the same amount of cash over 6 months"

medium.com/swlh/whats-so-…

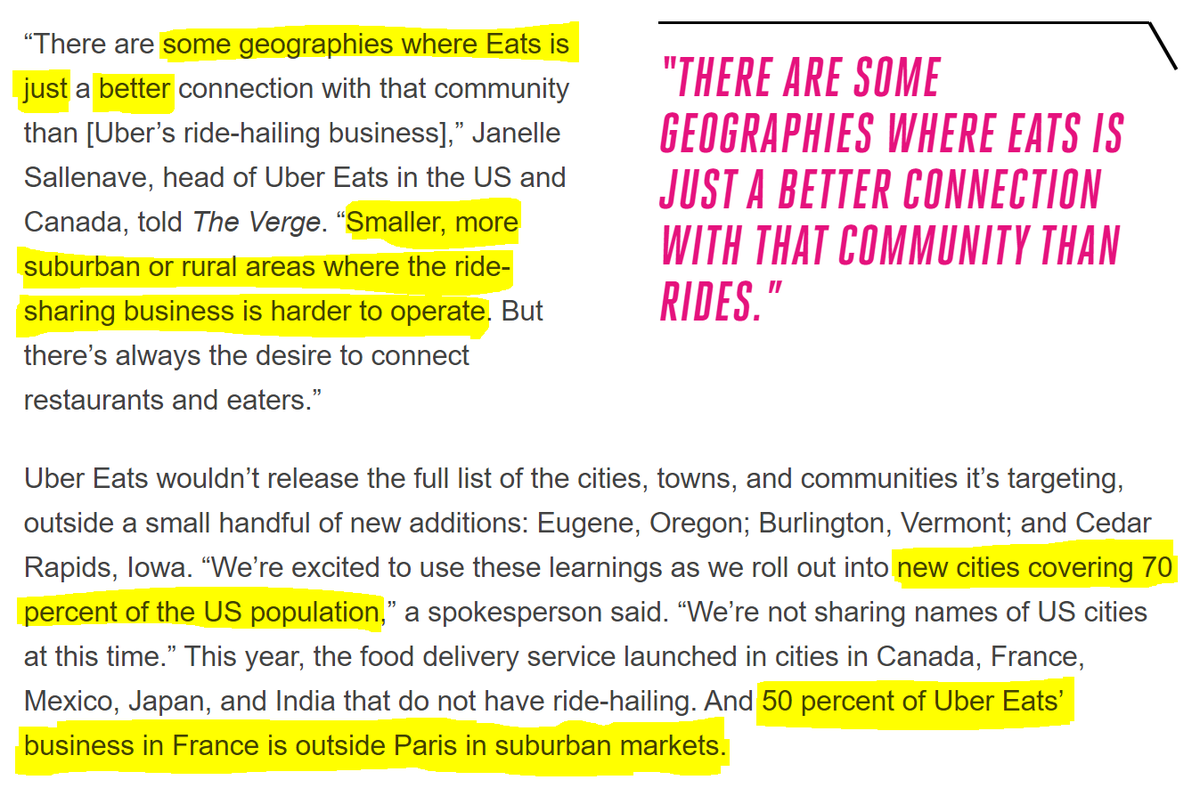

Data ripped from Uber’s site on April 14th hints Eats impact heavily skewed towards North America and Europe. Both likely have higher order sizes/margins, and take rates should stabilize/improve as expansion slows (EU may have room to run as ride hailing is heavily regulated)

Uber has said some Eats cities new (40% of Eats users are new to Uber). These not only cost more to open, but also further increase Uber’s footprint for further product expansion (rides, micromobility, grocery/e-comm delivery, etc).

theverge.com/2018/10/23/180…

theverge.com/2018/10/23/180…

We also have to consider how “cloud kitchens” designed and optimized for higher delivery volume and order pick-ups, not dining in, could change delivery economics, even creating a flywheel

-Lower pricing

-More demand

-Increased volume

-Lower pricing, etc

bloomberg.com/news/articles/…

-Lower pricing

-More demand

-Increased volume

-Lower pricing, etc

bloomberg.com/news/articles/…

Uber claims Eats covers 70% of the US population. 82% of Americans live in cities, implying Eats reaches 85% of the urban US population. This coverage sets a stage for Uber to eventually expand its last mile delivery network into groceries, ecommerce, etc

Beyond cloud kitchens, Uber could capitalize on its last-mile delivery network by building grocery stores designed from the ground-up for delivery, partner with other retailers for delivery, or even build full-stack third party ecom fulfillment warehouses

Logistics was ultimately how Amazon won the initial e-commerce wave, and last mile delivery networks built on top of ride hail, meal, and grocery delivery apps (which a consumer could use 5-10x per day) are an interesting way to win the next leg.

As Rides and Eats plateau, Uber's next leg of cash burn could be on micromobility.

Uber had $10M in bikes/scooters to end 2018, and Q1 earnings will show us how big that arsenal has become in preparation for potential hyper-scale over the next few years.

Uber had $10M in bikes/scooters to end 2018, and Q1 earnings will show us how big that arsenal has become in preparation for potential hyper-scale over the next few years.

Uber estimates that 46% of trips taken globally are under three miles, which means it’s likely we see Uber start to cannibalize its own sub-3 mile ride hails with micromobility, or what it refers to as “New Mobility”.

New Mobility likely has lower revenues, but it eliminates Uber’s highest expense - drivers - and expected improvements in micromobility unit economics as vehicle durability improves could bring Uber the higher margins long-promised by self-driving cars.

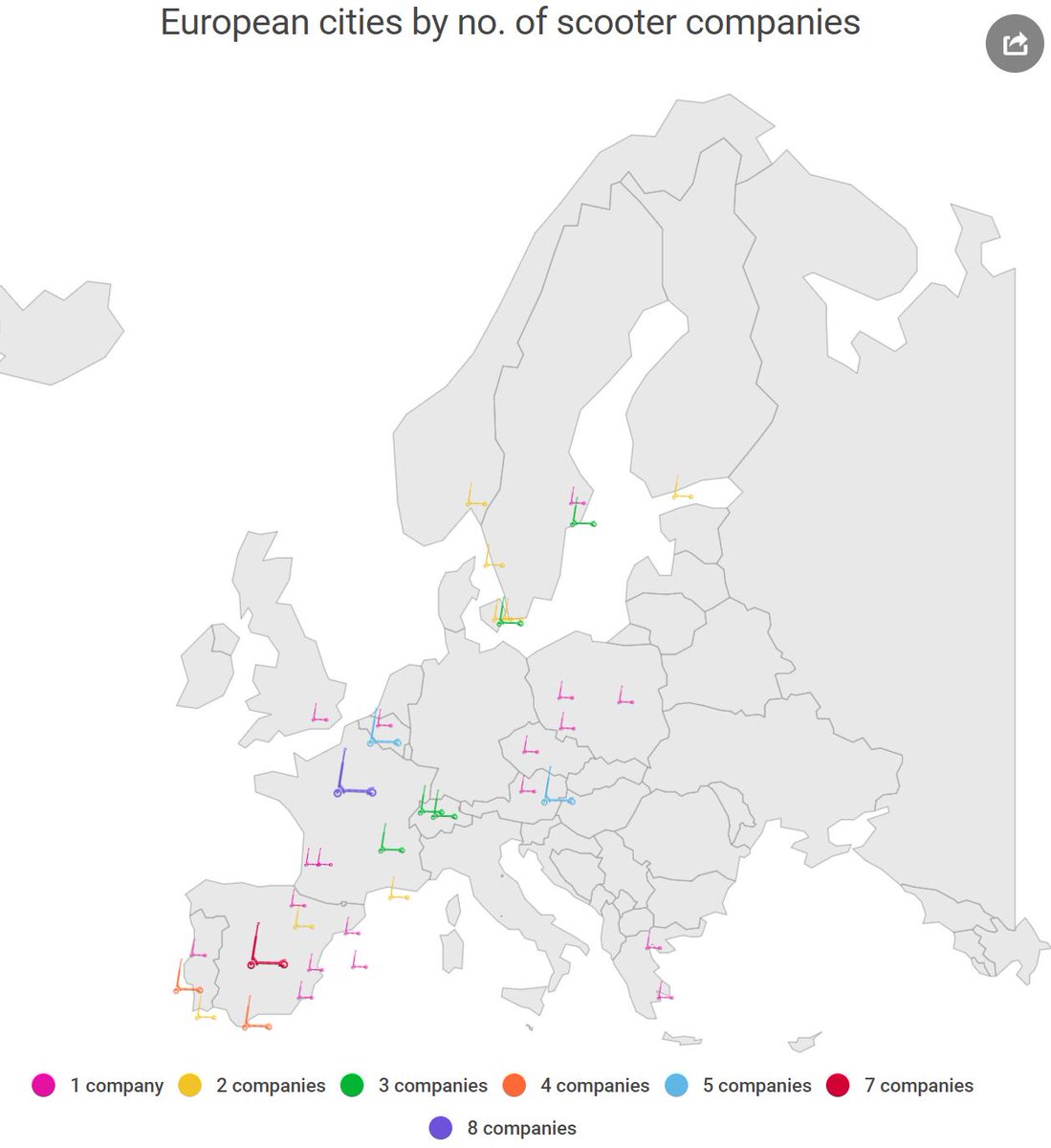

Uber will use its existing app install base, ops infrastructure, regulatory framework, and contractor network in 800 cities to deploy its JUMP micromobility services globally (currently in 22 cities), with the pace of growth likely limited by regulations.

Uber has a huge lead with operations in at least 147 European cities (likely more), compared to the 36 cities with scooters, period, in this map of European scooter companies

sifted.eu/articles/scoot…

sifted.eu/articles/scoot…

Uber will have more capital - $7.5B of cash/AR end of 2018, raising ~$10B in IPO, $1B from AV investment, + SoftBank as a backstop - than all its serious competitors, combined

(to illustrate, with $18.5B in cash + publicly traded equity {aka monopoly money}, Uber could buy Lyft)

(to illustrate, with $18.5B in cash + publicly traded equity {aka monopoly money}, Uber could buy Lyft)

Uber also has another edge: booking different mobility solutions (car, bike, scooter, public transit, etc) through one app, even at zero margins, gives it the clearest picture of city traffic patterns and which trips are being replaced by each modality.

The long-term bull case for Uber is that society shifts to app-first, on-demand transportation (it’s TAM is literally "total miles traveled"); where it's more affordable and convenient to pay-per-trip than pay the high fixed costs of personally owning a (perhaps multiple) vehicle

App-first transportation is more like a heating bill (varies on usage) and less like a mortgage (fixed cost no matter how used). It also breaks usage into friendlier $10-20 increments, not $500/mo or $25k upfront payments, and matches the habits of Gen Z.

wsj.com/articles/drivi…

wsj.com/articles/drivi…

There’s a case to be made that 30 minute meal delivery is cheaper and faster than buying groceries, paying higher housing costs related to a kitchen (or a car, garage and parking costs if Uber is your mobility service), and spending time prepping food.

The risk of a competitor coming in with a lower cost structure (Waymo fleets) is real, but Uber's cross-product rewards and subscriptions both increase the barrier to entry (harder to replicate) and increase customer spend / stickiness as it adds products

techcrunch.com/2019/01/22/ube…

techcrunch.com/2019/01/22/ube…

Uber‘s combination of Rides and Eats (and soon more) give it better control and utilization of its supply of drivers than competitors, which it uses to create demand that pulls more users into the Uber ecosystem.

Great deep dive by Ben Thompson here:

stratechery.com/2018/ubers-bun…

Great deep dive by Ben Thompson here:

stratechery.com/2018/ubers-bun…

By controlling the app used to access mobility services (demand), Uber can layer products over the cost structure of its ride hailing network:

-Eats (soon Eats Pooling/ads)

-Buses (Uber Pool is a precursor)

-Micromobility

-Last mile delivery

-Staffing

techcrunch.com/2018/12/10/ube…

-Eats (soon Eats Pooling/ads)

-Buses (Uber Pool is a precursor)

-Micromobility

-Last mile delivery

-Staffing

techcrunch.com/2018/12/10/ube…

On the supply side, Uber must keep drivers utilized. Eats utilizes drivers during non-peak ride hail times and increases the overall supply of drivers on the network (driving a taxi and delivering goods require different skills, and don't need a high-end car to deliver food).

Drivers see Uber as a flexible, on-demand job. A long-term case for Uber (after nailing driver supply / optimal mix of AV's) is to eventually help drivers do more than just drive - turning Uber into a full-fledged, hyper-efficient staffing agency.

techcrunch.com/2018/10/18/ube…

techcrunch.com/2018/10/18/ube…

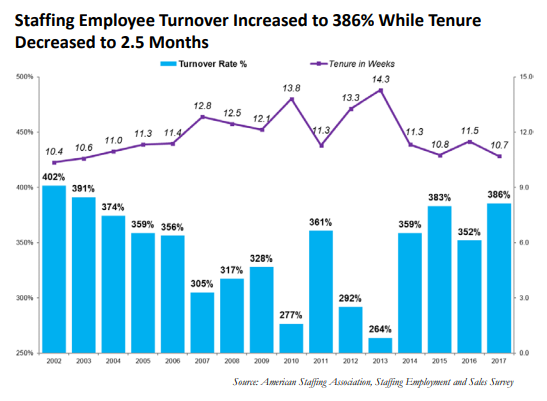

One of Uber's supposed flaws has always been driver churn. There's not enough disclosed in the S-1 to calculate it, but this in-depth CB Insights report estimates Uber's annual driver churn could be over 80%.

cbinsights.com/research/repor…

cbinsights.com/research/repor…

It's easy to forget that for millions of drivers, Uber is just a hyper-efficient temp agency.

Uber's 80% annual driver churn sounds insane, but it's low compared to the 250-400% churn seen in the staffing industry. Uber's driver churn may always be high.

americanstaffing.net/staffing-resea…

Uber's 80% annual driver churn sounds insane, but it's low compared to the 250-400% churn seen in the staffing industry. Uber's driver churn may always be high.

americanstaffing.net/staffing-resea…

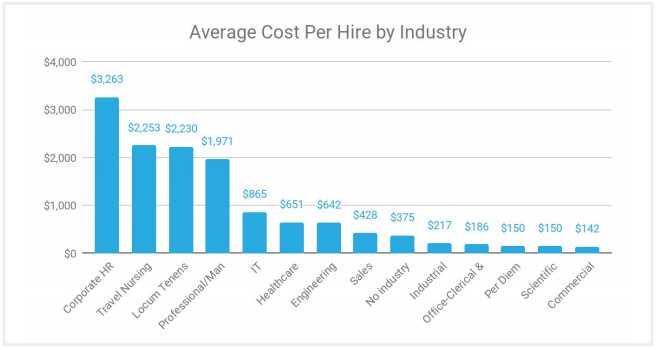

Onboarding costs are a large part of staffing agencies economic models (here's some charts for different industries). There's a clear trend:

The cost and time to onboard temp workers can be very high and fluctuates significantly by industry.

staffinghub.com/wp-content/upl…

The cost and time to onboard temp workers can be very high and fluctuates significantly by industry.

staffinghub.com/wp-content/upl…

Here's a chart detailing Uber's onboarding costs. Costs and time required vary significantly by market, largely affected by regulations.

With more than 3.9 million drivers at the end of 2018, Uber has more drivers globally than the 3 million temporary employees working for the entire US staffing industry during the average week.

americanstaffing.net/staffing-resea…

americanstaffing.net/staffing-resea…

Driving and delivery already provide drivers two options; bets in Freight, Groceries, and Health not only utilize Uber's routing capabilities, but are also new enterprise relationships it could soon staff (warehouses, shelf stockers, security, events).

Uber’s job on the supply side is to keep its drivers utilized, and help them earn sufficient income. Further developing its staffing agency model and matching drivers with alternative lines of work could help lower churn and keep them on the Uber platform.

Uber's core competency is getting things where they need to be. This goes beyond ride hailing; it's food delivery, it's logistics, it's the labor force, etc.

This is a great look inside Uber:

Just like Amazon famously API'd itself, Uber's products are designed to let employees borrow and combine different components, allowing things like its routing algorithms to scale over every product, in every city.

medium.com/swlh/whats-so-…

Just like Amazon famously API'd itself, Uber's products are designed to let employees borrow and combine different components, allowing things like its routing algorithms to scale over every product, in every city.

medium.com/swlh/whats-so-…

Every new product makes more economic sense for Uber than competitors because it can spread overhead costs over more units, and generate revenue over a wider set of uses case, in more cities, in more countries.

Uber Eats proved Uber can quickly bolt new products onto its existing global infrastructure, and it will be interesting what else it does with that capability.

"AWS for transportation" is a sexy pitch to investors, so is "AWS for physical labor"... both things Amazon can't touch

"AWS for transportation" is a sexy pitch to investors, so is "AWS for physical labor"... both things Amazon can't touch

Shout out to @michalnaka for pushing me to put this together on almost a daily basis over the past year. Also a big thanks to @James_Gross for being a sounding board, and to @nickabouzeid for convincing me to re-write this entire thing after I sent it to him.

Q1 15: wired.com/2015/12/uberea…

Q1 16: cbinsights.com/research/repor…

Q4 16/Q4 17: ft.com/content/7405bb…

Q1 17: cnbc.com/2017/12/07/ube…

Q2/3 17: nytimes.com/2017/09/23/tec…

Q1 18: foodandwine.com/news/ubereats-…

Q2 18: eater.com/2018/6/29/1751…

Q1 19: uber.com/cities; about.ubereats.com/en/cities

Q1 16: cbinsights.com/research/repor…

Q4 16/Q4 17: ft.com/content/7405bb…

Q1 17: cnbc.com/2017/12/07/ube…

Q2/3 17: nytimes.com/2017/09/23/tec…

Q1 18: foodandwine.com/news/ubereats-…

Q2 18: eater.com/2018/6/29/1751…

Q1 19: uber.com/cities; about.ubereats.com/en/cities