,

20 tweets,

8 min read

Read on Twitter

1. Recasting thread for proper linking in tweets.

Some observations from HAL Annual Report 2018-19. Not much interesting stuff which was not already known. And I am disappointed to see any real details on LCA Mk1A. But whatever I find interesting, here it is.

Some observations from HAL Annual Report 2018-19. Not much interesting stuff which was not already known. And I am disappointed to see any real details on LCA Mk1A. But whatever I find interesting, here it is.

2. For FY 2018-19 HAL's

- Total Sale 19704Cr (+7.8% from last year) (Export - 405 Cr)

- Profit Before Tax is 3627 Cr (+12%)

- Profit After Tax is 2282 Cr (+14.5%).

- Order book at end of FY 18-19 = 58588 Cr (~3yr worth production, not v good)

- Dividend paid + Tax - 798 Cr

- Total Sale 19704Cr (+7.8% from last year) (Export - 405 Cr)

- Profit Before Tax is 3627 Cr (+12%)

- Profit After Tax is 2282 Cr (+14.5%).

- Order book at end of FY 18-19 = 58588 Cr (~3yr worth production, not v good)

- Dividend paid + Tax - 798 Cr

3.

- Production - 41 Aircrafts (Fighters + Helis) & 102 Aero Engines &Accessories.

- R&D Expenditure - 1464 Cr (~2/3rd of PAT..!!)

- Cash at hand = 112 Cr (huge reduction frm ~6500Cr last yr and ~17700Cr from 14-15. Currently key concern)

- Operating Margin - 17.1% (comparable

- Production - 41 Aircrafts (Fighters + Helis) & 102 Aero Engines &Accessories.

- R&D Expenditure - 1464 Cr (~2/3rd of PAT..!!)

- Cash at hand = 112 Cr (huge reduction frm ~6500Cr last yr and ~17700Cr from 14-15. Currently key concern)

- Operating Margin - 17.1% (comparable

4.

to big global OEMs like LM/GE et al.

- Significant increase in borrowings likely due to pending payment on deliveries - 4158 Cr up from 864Cr last FY.

- Net Worth is 10,848 Cr.

Summary in picture below.

to big global OEMs like LM/GE et al.

- Significant increase in borrowings likely due to pending payment on deliveries - 4158 Cr up from 864Cr last FY.

- Net Worth is 10,848 Cr.

Summary in picture below.

5. Currently running programs with bare minimum updates:

- LCA MK1/MK1A

- NLCA

- HTT-40

- LCH

- LUH

- Upgrades - M2K, Jag DARIN-3, Hawk-i

- HTFE-25/HTSE-1200

- Do-228

No updates on ALH, WSI, Su30MKI, IMRH, NUH, RUAV, LCA MK2, status of NP5.

- LCA MK1/MK1A

- NLCA

- HTT-40

- LCH

- LUH

- Upgrades - M2K, Jag DARIN-3, Hawk-i

- HTFE-25/HTSE-1200

- Do-228

No updates on ALH, WSI, Su30MKI, IMRH, NUH, RUAV, LCA MK2, status of NP5.

6. Key achievements mentioned as shown in pictures. Nothing new there. We already know more updates on some of the programs like LCA, LUH and HTT-40 now.

7. Status of HTT-40 as of March-2019 - Two Prototypes with 260 test flights. Interesting tidbit - Structural Test Specimen has completed Ultimate Load test (165%). Ultimate load is something that is expected to be seen once in the life of entire fleet. 165% is wrt, Limit load

8. which is max load expected once in a lifetime of a single aircraft. Typically 150% is used as design target. Interesting to see 165%. This is likely the load at which the structure failed, which means design in slightly conservative.

HTT-40 recently completed 6 turn spin test

HTT-40 recently completed 6 turn spin test

9. HAL delivered first Upgraded M2K at IOC standard with indigenous kit to IAF on Jan 2019. Sadly total number of Upgraded M2K delivered to IAF is not mentioned.

10. Update on DARIN-3 Program. Total 436 Test flights by March 2019. Must have crossed 500 by now. I see these Jags flying out daily.

11. Interestingly Hawk-i also undergoing Spin tests. Completed 2-turn spin by end of FY 18-19. SAAW already integrated with Hawk. No mention of ASRAAM though. I wonder if the RTOS mentioned is the same RTOS that HAL was working on.

12. Army version of LCH has recieved IOC. Total 1498 test flight completed by 4 TDs. All Dev Trials completed along with Weapons Trials. I guess ATGM is pending subject to HELINA testing completion. But rest of the weapons done. Orders awaited for 15 LSP. No mention of MFG status

13. LUH - 3 Prototypes completed 245 test flights by end of March 2019. Envelop expansion, Cold weather, Hot whether, Sea level, Max altitude tests done. Recently LUH finished Hot and High tests at Leh and DBO. Certification close, but no word on orders. 197 LUH are projected.

15. OK now some very very interesting information - Seems like revised cost of 20 IOC LCA MK1 Batch is Rs. 5362.17 Cr. The IOC batch was ordered in 2006 & it includes 4 Trainers in it. If my interpretation is correct, Avg cost of IOC LCA Mk1 is ~268 Cr...!!

16. Data point on ALH - Original Cost for IA was 82.10 Cr per ALH. Now its not clear which variant and whether it includes and spares or MRO component. Revised cost - 124.73 Cr

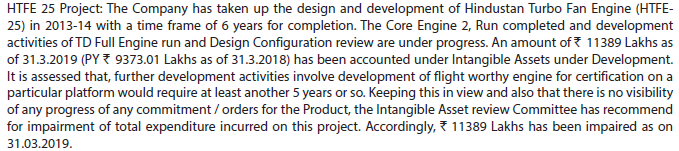

17. #HTFE25 started in 2013-14 with 6yr timeframe. Current status - Core 2 runs completed. Now Full Engine TD runs and Design Config review in progress.

No order yet, but product specific dev (e.g. for IJT or Jaguar) would take another 5yr, which is what I had expected too.

No order yet, but product specific dev (e.g. for IJT or Jaguar) would take another 5yr, which is what I had expected too.

18. HAL has projected sales potential of total 290 Aircrafts (70 for IAF and 220 for others) for #HTT40. Its not clear though whether the additional 36 nos possible from IAF are already included in the number 220 or not.

19. HAL seek approval from MoD for winding up of MTY JV company and the closure of IGA. So MTA project is finally gone for good.

20. Another interesting tidbit - Picture of LCH with an Auxiliary Fuel Tank on its pylon.