,

34 tweets,

6 min read

Read on Twitter

1/ Ergodicity seems like one of the most important investing (and life) concepts that few people understand.

I am not sure I fully understand it, but here is my attempt to explain ergodicity as I understand it now

I am not sure I fully understand it, but here is my attempt to explain ergodicity as I understand it now

3/ In scenario one, the ensemble scenario, one hundred people go to a Casino to gamble with a $1,000 each and have a few rounds of gin and tonic on the house.

4/ Some will lose, some will win, and we can infer at the end of the day what the “edge” is and figure out if the casino is properly pricing the odds.

5/ Let’s say in this example that our gamblers are all using a particular strategy which, on average, makes $500 each day, a 50% return.

6/ However, this strategy also has the risk that, on average, one gambler goes bust. In this case gambler number 28 blows up. Will gambler number 29 be affected? Not in this example.

7/ You can calculate that, on average, each gambler makes about $500 per day and about 1% of the gamblers will go bust.

8/ Using a standard cost-benefit analysis, you have a 99% chance of gains and an expected average return of 50%. Seems like a pretty sweet deal right?

9/ Now compare this to scenario two, the time scenario. One person, your card counting cousin Theodorus, goes to the Casino a hundred days in a row, starting with $1,000 on day one.

10/ He makes 50% on day 1 and so goes back on day 2 with $1,500.

He makes 50% again and goes back on day 3 and makes 50% again, now at $3,375

He makes 50% again and goes back on day 3 and makes 50% again, now at $3,375

11/On Day 18, he has $1 million. On day 27, $56 million.

But, when day 28 strikes, cousin Theodorus goes bust. Will there be day 29? Nope, he’s broke and there is nothing left to gamble with.

But, when day 28 strikes, cousin Theodorus goes bust. Will there be day 29? Nope, he’s broke and there is nothing left to gamble with.

12/ You can safely calculate that using this strategy he has a 100% probability of eventually going bust.

The central insight: The probabilities of success from the collection of people *does not* apply to one person.

The central insight: The probabilities of success from the collection of people *does not* apply to one person.

13/ The first scenario is an example of ensemble probability and the second one is an example of time probability (since the first is concerned with a collection of people and the other with a single person through time).

14/ An ergodic system is one in which the outcomes of an ensemble and time probability are the same.

That is not the case here and so this gambling strategy is NOT ergodic.

That is not the case here and so this gambling strategy is NOT ergodic.

15/ Most finance material assumes ergodicity (that time and ensemble probabilities are the same) even though it is not the case.

16/ If you lose all my money, you are in no way comforted that other people who I don't know did fine.

17/ Even if their forecast were right, no person can get the returns of the market unless they have infinite pockets

18/ If the investor has to eventually reduce his exposure because of losses, or margin calls, or because of retirement, or because a loved one got sick and needed an expensive treatment, the investor’s returns will be divorced from those of the market.

19/ Most famously Long-Term Capital Management used models which assumed ergodicity in a non-ergodic environment.

20/ Initially successful with an annualized return of over 21% (after fees) in its first year, 43% in the second year and 41% in the third year, in 1998 it lost $4.6 billion in less than four months

21/ In 1998, LTCM established an arbitrage position in the dual-listed company (or "DLC") Royal Dutch Shell in the summer of 1997, when Royal Dutch traded at an 8%–10% premium relative to Shell. LTCM was "long" Shell and "short" Royal Dutch

22/ LTCM was essentially betting that the share prices of Royal Dutch and Shell would converge because in their belief the present value of the future cashflows of the two securities should be similar.

23/ This might have happened in the long run, but in the short run, the premium of Royal Dutch increased 22%, combined with losses in other parts of the Portfolio LTCM had to unwind its position in Royal Dutch Shell at a loss of more than $140 million.

24/ LTCM's collapse stemmed in part from their use of only five years of financial data to prepare their mathematical models, thus drastically under-estimating the risks of a profound economic crisis

25/ By definition, it is unlikely that a 1 in 20 year event would show up in five years of data, but highly likely it would show up within 20 years.

26/ I am reminded of a joke someone once told me about leveraged deep value investors: “It looks ok at 100, it looks good at 90, it looks great at 80, it looks absolutely fantastic at 70, and you’re out of business at 60.”

Another example I have been looking at is the correlation between stocks and bonds.

Over the last 30 years or so, stock and treasury bonds have been mostly anti-correlated or uncorrelated

As @max_arbitrage points out "For most people 60/40 stock/bond strategies don’t work out.

You only get one timeline and there is a good chance at some point your income or something else serious will get hit at the same time markets drop."

You only get one timeline and there is a good chance at some point your income or something else serious will get hit at the same time markets drop."

It is non-ergodic, the returns of the market (ensemble probability) are not the returns of the individual (time probability)

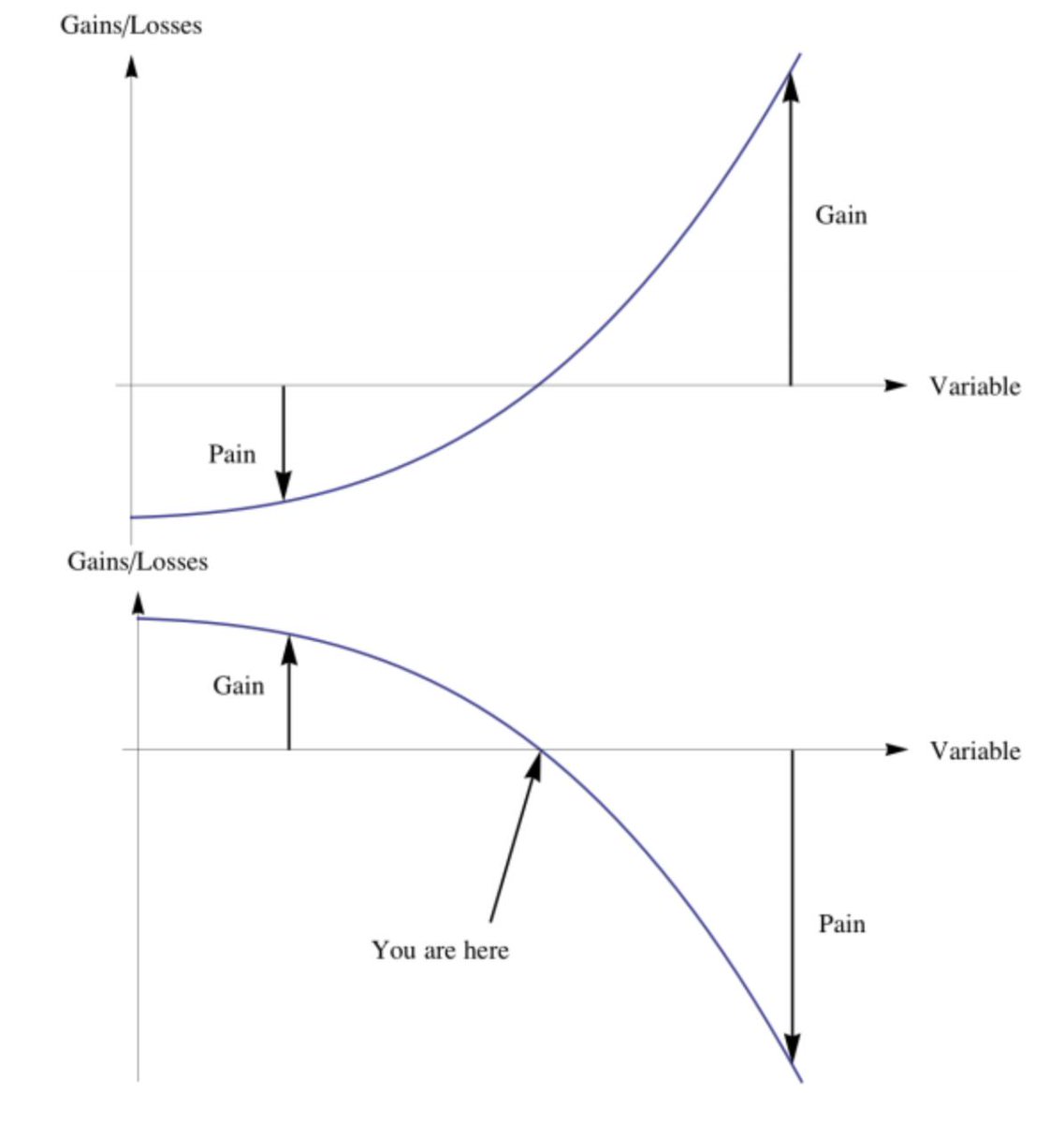

One helpful concepts that go along with this is the idea of convexity vs. concavity.

The top half of this graph is convex. As variability increases, so do gains. This is antifragility.

The bottom half is concave, as variability increases, so do losses. This is fragility

The top half of this graph is convex. As variability increases, so do gains. This is antifragility.

The bottom half is concave, as variability increases, so do losses. This is fragility

If you have concave exposure in a non-ergodic system and there is some chance of blowing up, then it is guaranteed you will eventually blow up.

Also helpful is the Kelly Criterion about bet sizing:

If cousin Theodorus sizes his bets according to the Kelly Criterion, then he is in great shape.

If cousin Theodorus sizes his bets according to the Kelly Criterion, then he is in great shape.

@threadreaderapp unroll please