Had talked about WeWork pricking the fever in private company valuations.

Upon further consideration am now somewhat concerned about the fallout-cascade.

(a thread)

Upon further consideration am now somewhat concerned about the fallout-cascade.

(a thread)

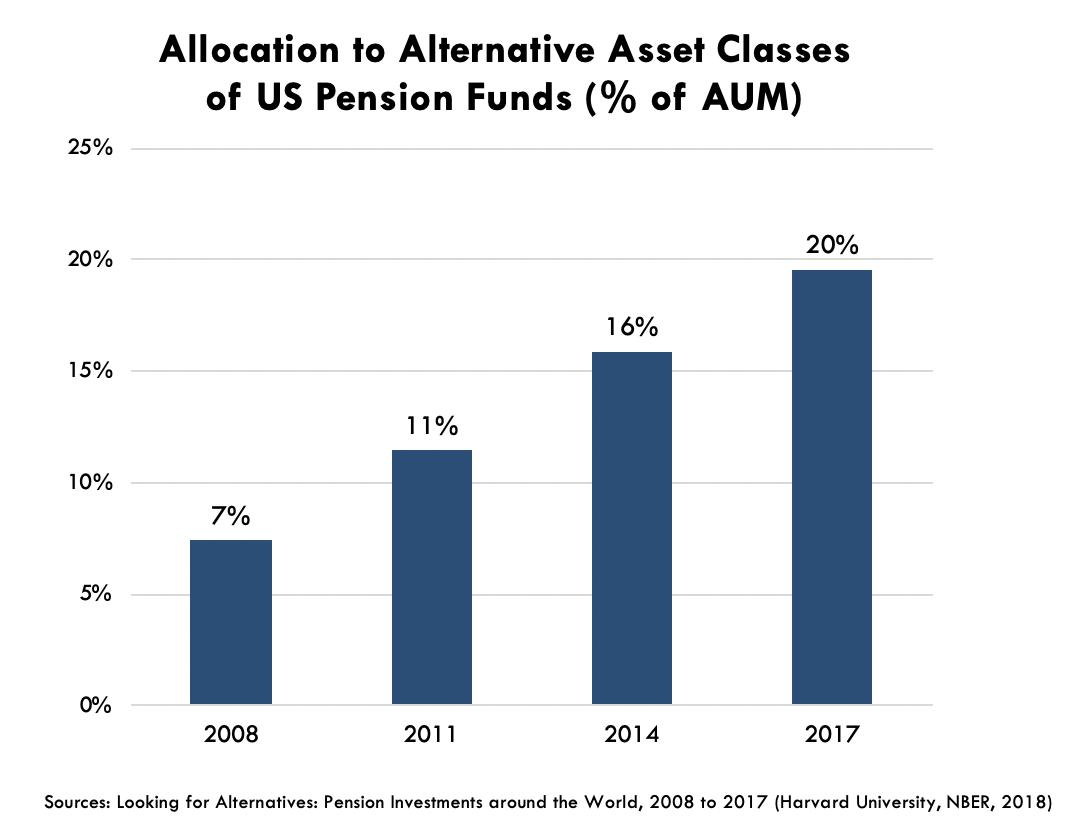

Endowments and institutions have spent the past decade throwing money at VC/illiquid opportunities.

2/

(display from a great presentation forthcoming by @mfriedrichARK)

2/

(display from a great presentation forthcoming by @mfriedrichARK)

@mfriedrichARK The capital flow has overwhelmed the number of opportunities available in the sector, but the VCs aren't incentivized to turn down money (those management fees!)

3/

3/

@mfriedrichARK Moreover, the VC incentive structure for holding the line on valuation is relatively weak. As covered by @stalwart even a failed unicorn can be good for business.

4/

4/

@mfriedrichARK @Stalwart (The founder incentive structure for holding the line on valuation is *obviously* even weaker 🤑🤑🤑)

(And though the employees should push back they're not well-positioned to do so)

5/

(And though the employees should push back they're not well-positioned to do so)

5/

@mfriedrichARK @Stalwart Valuation-shorthands and business-models will concomitantly arise that will most readily solve the problems of this system

The problems: a surplus of capital, and the need to justify continual valuation mark-ups.

6/

The problems: a surplus of capital, and the need to justify continual valuation mark-ups.

6/

@mfriedrichARK @Stalwart The best-fit solution to this dilemma will be the use of price-to-sales as a valuation shorthand coupled with business models that can most easily convert unlimited capital into nearly-unlimited revenue growth.

7/

7/

@mfriedrichARK @Stalwart The scooter companies are a fine example.

I convert $1 raised into $1 worth of 🛴 and fractionally onsell it into $0.75 of revenue before the 🛴 gets chucked in a lake.

Seems a bad business.

8/

I convert $1 raised into $1 worth of 🛴 and fractionally onsell it into $0.75 of revenue before the 🛴 gets chucked in a lake.

Seems a bad business.

8/

@mfriedrichARK @Stalwart But if the valuation shorthand is 10x sales, raising $1 and onselling it at $0.75 can yield astounding riches, so long as you can do it at scale (and the investors keep playing along.)

9/

9/

@mfriedrichARK @Stalwart To keep investors playing along you only have to obscure the fact that the product you are selling is negative gross margin (exclude capital depreciation and amortization, classify discounting as a customer acquisition cost, etc etc.)

10/

10/

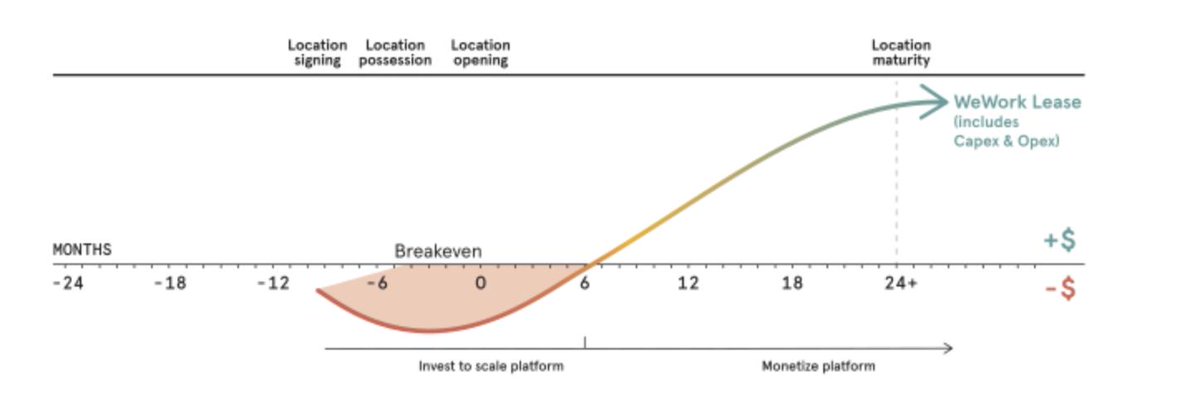

@mfriedrichARK @Stalwart WeWork was the logical end-point of all of this; they dealt in a product that is maximally leverage-able and where the underlying unit economics are most concealable.

11/

11/

@mfriedrichARK @Stalwart If the Vision Fund had successfully injected another $16 billion into WeWork, on-paper returns to the fund would likely have looked attractive enough to successfully fundraise Vision II--the merry-go-round would still be spinning.

12/

12/

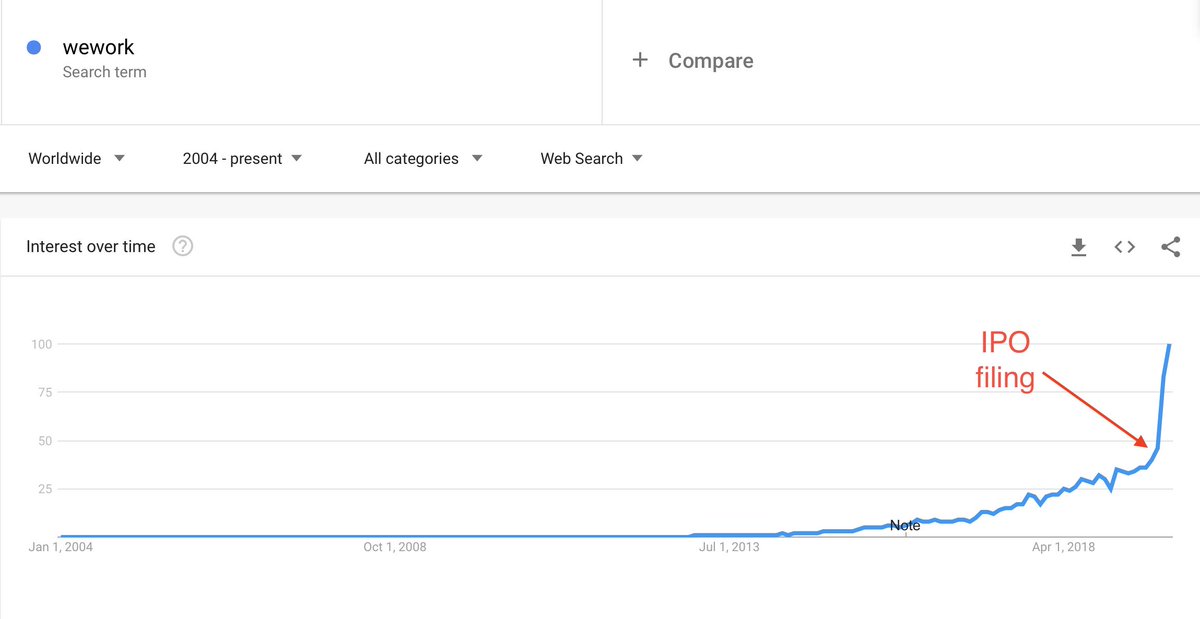

@mfriedrichARK @Stalwart WeWork's stumble is most directly attributable to the LPs (rather than the VCs) finally yanking the reins.

The Saudis finally balked at the valuation, forcing WeWork prematurely into public market scrutiny.

13/

The Saudis finally balked at the valuation, forcing WeWork prematurely into public market scrutiny.

13/

@mfriedrichARK @Stalwart The concern is that WeWork--while the largest and most prominent example--is representative of an entire herd of unicorns that are leveraged upon the characteristics of this VC-mediated capital-flow tailwind.

14/

14/

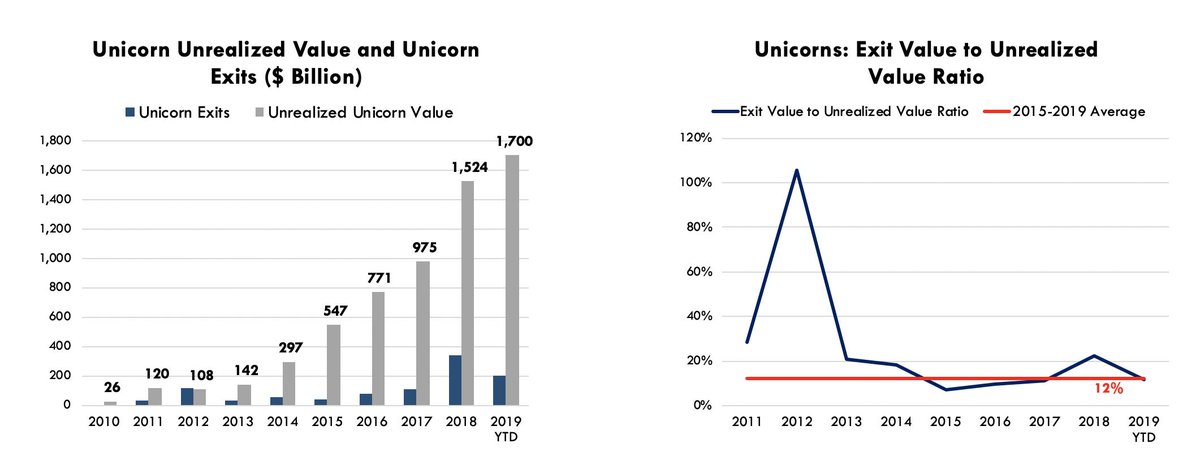

@mfriedrichARK @Stalwart What percent of the $1.7 trillion in on-paper unicorn market-cap is driven by unit economics that don't efficiently scale or prove?

15/

15/

@mfriedrichARK @Stalwart And even among those with reasonably defensible business models how many have growth rates and sales-cycles that specifically cater to the class of VC-funded companies that are price-insensitively sloughing off VentureBucks?

16/

16/

@mfriedrichARK @Stalwart Further, even amongst those companies not directly tied to VentureBucks or pursuing unit-economics-backwards business models, how many have addressable markets that only seem broad from inside the Silicon Valley bubble but are actually quite narrow?

17/

17/

@mfriedrichARK @Stalwart (Good time to remind everyone that uber/lyft miles are cost-equivalent to driving a ~$250k car, and that a $2,000 exercise bike is a major major purchase for all but 10% of households.)

18/

18/

@mfriedrichARK @Stalwart Given the perceived recklessness of the WeWork trajectory, and the degree to which that recklessness and its sudden evaporation has permeated the media, it seems likely to me that LPs will begin asking their VCs to justify/assess their portfolios.

19/

19/

@mfriedrichARK @Stalwart LPs may even begin to resist capital calls, or simply re-allocate elsewhere rather than pumping further bucks into the venture ecosystem; at the margin the liquidity will begin to choke off.

20/

20/

@mfriedrichARK @Stalwart In any leverage cycle the marginal drying up of liquidity can have dramatic (and often painfully prolonged) impact.

21/

21/

@mfriedrichARK @Stalwart As stumbles at the IPO window cascade back into private valuations the process has the potential to self-reinforce: LPs try to claw back capital, companies--now balance-sheet-constrained--have to choke off growth ambitions; valuations adjust further down ♻️♻️♻️

22/

22/

@mfriedrichARK @Stalwart The tightening of the spigot may further hurt VC-funded business fundamentals. Without the price-insensitive startup tumult sales cycles for B2B software will prolong and growth will come more dear...

23/

23/

@mfriedrichARK @Stalwart ...that WeWork flex-space seems a likely first-cut on the bottom line, that $4 per mile scooter ride to save a 15 minute walk no longer seems such a necessary trade (particularly as prices go up to accommodate the balance sheet crunch.)

24/

24/

@mfriedrichARK @Stalwart And absurd SF real-estate prices driven by on-paper wealth (and VC management fees) at least plane off--likely ramifications for commercial real estate as well--it could all be more painful and longer than anyone foresees.

25/

25/

@mfriedrichARK @Stalwart Hurt worst of all will be the employees of the firms--as were hurt worst by WeWork--they had incentive to hold the line on valuation but no mechanism by which to do so--they almost certainly bought the vision and accepted over-priced equity in lieu of cash.

26/

26/

@mfriedrichARK @Stalwart If the cash-cost of attracting talent goes up as a by-product of this shake-out it may present the most grave threat to startup bootstrapping of all.

27/

27/

@mfriedrichARK @Stalwart As should have been obvious it is/was a leverage cycle. The VCs have been borrowing additional money from their clients collateralized by the underlying assets into which they are going to invest.

28/

28/

@mfriedrichARK @Stalwart Subjectively, any time a class of professionals gets lionized (as VCs have been, as CryptoNerds slightly were, as HedgeFunders before, and banker/traders before, and TechGods before) it is a fair indication that something is self-perpetuating is askew

29/

29/

@mfriedrichARK @Stalwart Though it is not certain that WeWork signals the turn, it seems a reasonable candidate, and if history is a guide the unraveling could be prolonged and painful.

30/

30/

@mfriedrichARK @Stalwart (I don't mean to imply that system participants are/were acting in bad faith--VCs try to do legitimately right by their clients as do entrepreneurs by their shareholders--the ""misbehavior"" is instead an emergent property of the competitive system's incentive structure.)

/fin

/fin