$TSLAQ There has been endless discussion about $TSLA GAAP accounting and I am the primary culprit. We never really discuss accounting as a social science. GAAP is a nasty document open to manipulations by management. Which provides a study of management behavior (1/19).

External audit only provides reasonable assurance that the financial statements materially adhere to GAAP. Management is the responsibility for their creation. Why is this important? Let’s just look at the last three quarters of $TSLAQ. (2/19)

Q1 2019 was after two successful – by $TSLAQ standards – quarters. Q3 2018 reported $311m in net income with operating cash flow of $1,391m. Q4 reported 210m in net income and operating cash flow of $1,234m. (3/19)

The stock reported price peaks for each quarter at $346 & $365 respectively. Before announcements the stock bottomed at $258. (4/19)

Q1 2019? If expectations theory exists beyond the bond market, we found it in Q1. $702m loss. Negative $639m operating cash flow. Unit deliveries down 13,600 Q to Q. Stock price bottoms at $186. (5/19)

Q1 Accounting: $35m increase in warranty accruals, a net impact of $92m for sales returns, $80m inventory write-down, restructuring of $34m and $18m in asset disposals. $259m or 37% of the loss was discretionary accruals. Big bath quarter. The stock price got nailed. (6/19)

Q2 2019? Management learned a little from Q1. Don’t surprise the market and move metal. $408m loss with $863 operating cash flow. Unit deliveries 95,200 up from 63,000 Q1. The stock bumps to $264. (7/19)

Q2 Accounting: Its really a mixed effort. Restructuring charges were $117m, $35m inventory write-downs, $29m losses on disposal of assets, $5m sale return net income impact were losses. (8/19)

But, intangibles for in use technology – company written software increased by $102m which decreases expenses. Net discretionary negative accruals were $84m. (9/19)

Q3 2019? Management has learned a few things. Discretionary accruals are their friend. The market is ignorant about accounting. Moving metal forgives all sins. (10/19)

Net income $143m. Cash flow from operating activities 756m. Units delivered 97,186 up 1,986 from Q2. The stock price is still ripping closing at $406 today. (11/19)

Q3 Accounting: warranties provision reversed $37m, sales return reserve reversed $16m, depreciation estimates changed $46m, additional FSD recognized $30m, prepaids capitalized (no cash associated) $55m, currency manipulation $85m, capitalize intangibles again $37m. (12/19)

Disposal loss was $21m. Total positive discretionary accruals $285m. Add in Q2 restructuring charges of $117m from Q2 and it totals $402m. The Q2 loss was $408. Call the CEO of Pana, belittle their relationship, and get $156m in concessions. It is a $150m profit. (13/19)

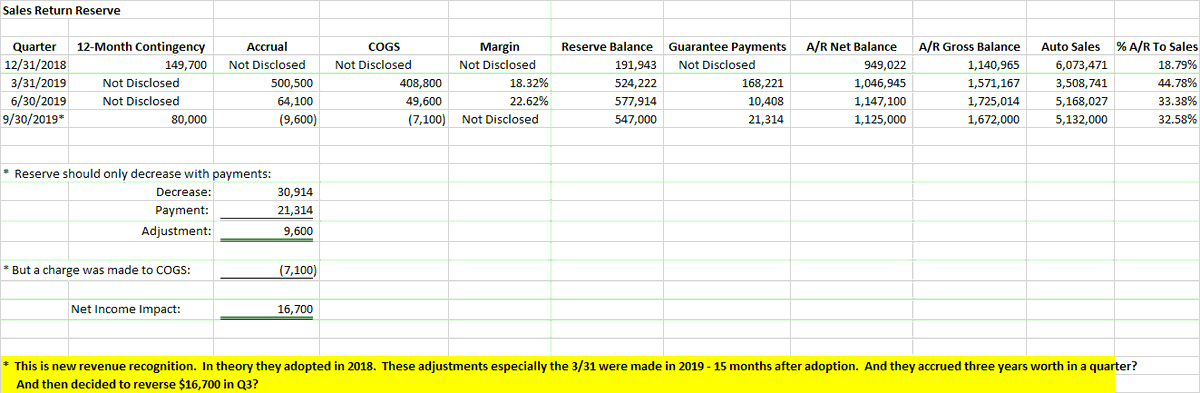

So what about Q4? The 12-month contingency for sales returns was lowered from $149m to $80m. $69m. Warranties can easily handle another $35m. They already changed useful life for molds so $50m. Prepaids can handle another $20m. Intangibles are good for another $50m. (14/19)

Currency might have $10m. No disposals in Q4 $20m. Management does not execute 1/24 of their normal options $34m. The effective interest rates goes down with the new bond rating for in use and capital leases $10m. Good for at least $298m before deferred revenues. (15/19)

Here is the mother load. Early release of FSD plus a speed booster. The Q3 reported $662m of auto deferred revenues to be recognized in 12 months. $140m of ZEV credits. If it is just averaged over 12 months that’s $66.8m per month or $200m in for Q4. (16/19)

Potentially $498m in discretionary accruals for Q4. Hit Pana for another $150m and you are up to $648m. It only took $283m in Q3 plus Pana to hit $150m. It’s now $241m profit (17/19)

It should good for another 100 point rip in the stock. Giving a buffer for the absolute misery of the 20% vig that the CCP is about to hit $TSLAQ with for every vehicle they make at GIGAswamp. Plus the 20% loss of demand next year with no new markets (18/19)

Also all of those cars on the road are about to face normal warranty expenses - the kind you have to pay in cash instead of accrue. Since 2016, they have produced 697k cars. 515k since 2018 (74%). Those puppies are about to make a pit stop (19/19 plus 1.)

If anyone has tracked accounting and legal counsel turnover, overlap it to the increase in aggression in the accruals for the past three quarters. Down to the staff level. Turnover had to be traumatic just for the SEC filings. (plus 1)