MEGA THREAD:

Just in March, has outperformed the index by ~15%. Here's AMZN's historical return:

5-yr CAGR +37%

10-yr CAGR +30%

20-yr CAGR +18%

From IPO +36%

I will discuss the whole business, why I am bullish, and the possible risks.

Just in March, has outperformed the index by ~15%. Here's AMZN's historical return:

5-yr CAGR +37%

10-yr CAGR +30%

20-yr CAGR +18%

From IPO +36%

I will discuss the whole business, why I am bullish, and the possible risks.

1/ business segments:

1P: First-party i.e. AMZN brands or the products for which they take inventory risks

3P: Third-party sellers

Physical Stores: Wholefoods Stores/AMZN Go

Subscriptions: Prime membership, Music, Video etc

AWS: Cloud

Other: mainly Ad

1P: First-party i.e. AMZN brands or the products for which they take inventory risks

3P: Third-party sellers

Physical Stores: Wholefoods Stores/AMZN Go

Subscriptions: Prime membership, Music, Video etc

AWS: Cloud

Other: mainly Ad

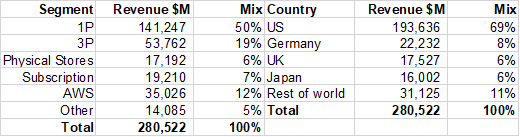

2/ Before I talk about each business lines in more detail, here's a fascinating table. basically transformed every expense line item in Income Statement into source of revenue.

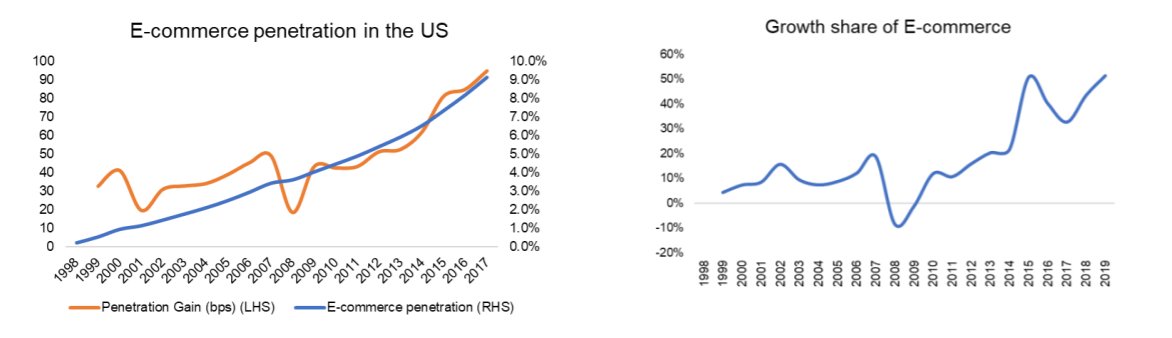

3/ Let's start with e-Commerce which was ~70% of 2019 revenue. Two things I want to mention:

A) While it’s not Day 1 anymore, e-commerce is still just ~10-12% of retail sales

B) e-Commerce growth share (e-Commerce $ growth/US retail sales $ growth) shows no signs of slowdown

A) While it’s not Day 1 anymore, e-commerce is still just ~10-12% of retail sales

B) e-Commerce growth share (e-Commerce $ growth/US retail sales $ growth) shows no signs of slowdown

4/ e-Commerce will be ~2x 10 years from now i.e. ~25% of US retail. If has ~40% share of all US e-Com retail, 1P+3P GMV just in US will be $700 Bn. Add international GMV, we are looking at $1 Tn GMV for AMZN in 10 years.

COVID-19 will quicken the shift even further.

COVID-19 will quicken the shift even further.

5/ But two questions I have heard:

A) Will be (Is it already) too big?

In 10 years, will be ~10% of US retail. was at 12% of US retail at its peak.

There will be lots of noise, but nothing damaging is unlikely to happen to from regulatory perspective

A) Will be (Is it already) too big?

In 10 years, will be ~10% of US retail. was at 12% of US retail at its peak.

There will be lots of noise, but nothing damaging is unlikely to happen to from regulatory perspective

6/

B) Is retail profitable?

I believe Yes for 3P, No for 1P.

How much? It's complicated. But I'll explain.

Let's talk about 1P first. doesn't disclose profitability by business segment. They disclose by North America, International, and AWS. So we will have to..

B) Is retail profitable?

I believe Yes for 3P, No for 1P.

How much? It's complicated. But I'll explain.

Let's talk about 1P first. doesn't disclose profitability by business segment. They disclose by North America, International, and AWS. So we will have to..

7/ ...play a guessing game.

, doesn't do 1P. does. For 1P, shipping cost is the biggest Achilles heel because it doesn't seem to scale at all. Some may say 's cost as % of GMV is increasing because of 1-day shipping. But look at , it's been ~7% in last 5yr

, doesn't do 1P. does. For 1P, shipping cost is the biggest Achilles heel because it doesn't seem to scale at all. Some may say 's cost as % of GMV is increasing because of 1-day shipping. But look at , it's been ~7% in last 5yr

8/ If comes close to 's numbers 10 yrs from now, we are looking at 2% EBIT margin. I assumed 1.5% in 2030.

You may think I am conservative. But when I am forced to play guessing game, I want to err on the side of caution.

You may think I am conservative. But when I am forced to play guessing game, I want to err on the side of caution.

9/ I estimate $315 B revenue from 1P, but assuming 1.5% EBIT margin, it leads to *only* $4.7 Bn EBIT. Given the size of , my advice is don't lose ANY sleep thinking about 1P's profitability even though it can seem VERY important looking at topline.

10/ Now let's talk about 3P.

, has 3P business. 3P, just like them, is a marketplace connecting buyers and sellers.

's take rate is ~15%, 's take rate in 2018 was 26.7%. But there's a caveat...

, has 3P business. 3P, just like them, is a marketplace connecting buyers and sellers.

's take rate is ~15%, 's take rate in 2018 was 26.7%. But there's a caveat...

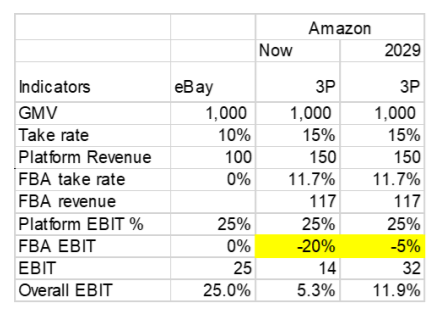

11/ also has FBA (Fulfillment by AMZN) which charges ~15% to 3P sellers. ~80% of 3P sellers use AMZN FBA, and the rest use FBM (Fulfillment by Merchant). If you're FBM, you just pay 15% "toll" to access the marketplace. FBA 3P sellers pay ~30%.Overall take rate 26.7%.

12/ So, even though has 25% EBIT margin, 3P will most certainly not achieve such margin ever because FBA is inherently capex intensive and low margin business. I estimate long-term EBIT margin to be ~12% for 3P business. Here's how...

13/ Here's a sample calculation (see image). Why do I assume FBA to remain unprofitable? Lots of reasons, but mainly as long as hardly makes any money from FBA, it will discourage any potential entry. will just focus on scale.

Scale is 's religion.

Scale is 's religion.

14/ I estimate 3P to be ~$200 Bn topline business in 2030 and with ~12% EBIT margin, it will be $25 B EBIT.

So big takeaway from retail:

1P doesn't matter much.

3P does.

Also, look at this table from @JeffBezos letter in 2018. this is 3P as % of retail GMV.

So big takeaway from retail:

1P doesn't matter much.

3P does.

Also, look at this table from @JeffBezos letter in 2018. this is 3P as % of retail GMV.

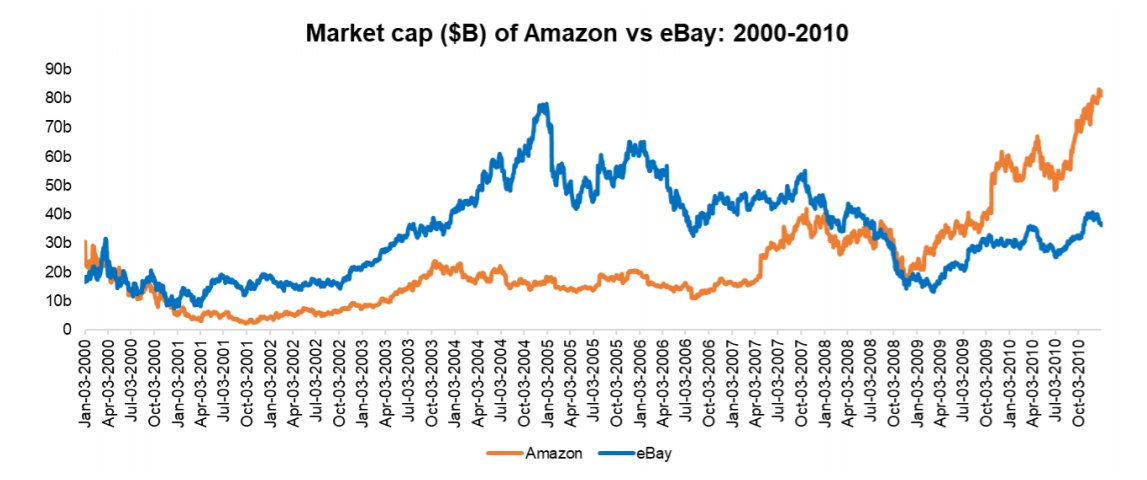

15/ I thought it was interesting that almost the entire decade of 2000s, Mr. Market valued more than . Not picking on investors; the business has obviously changed a LOT and it wasn't clear would become what it has become.

16/ Let's move on to Subscription business (~$20 B rev).

Half of subscription revenue comes from Prime membership.

In 2015 letter, @JeffBezos said, "“We want Prime to be such a good value, you’d be irresponsible

not to be a member."

Half of subscription revenue comes from Prime membership.

In 2015 letter, @JeffBezos said, "“We want Prime to be such a good value, you’d be irresponsible

not to be a member."

17/ Prime is perhaps the most effective marketing tool in last two decades. Why? It helped customers "forget" the friction of shipping expense!

"Once you become a Prime

member, your human nature takes over. You want to leverage your $79 as much as possible." (Now it's $119/yr)

"Once you become a Prime

member, your human nature takes over. You want to leverage your $79 as much as possible." (Now it's $119/yr)

18/ Prime members grew at 28% CAGR in last 5 yrs.

Prime, FBA, marketplace, and logistics have created a wide and defensible moat for retail platform which does and will drive profitability through subscription and advertising (will discuss later)

Prime, FBA, marketplace, and logistics have created a wide and defensible moat for retail platform which does and will drive profitability through subscription and advertising (will discuss later)

19/ 1/5th Prime members use AMZN Music, 1/3rd use Prime Video.

Prime is a GREAT platform to launch all sorts of ancillary services and grab a greater wallet share.

So how profitable is the subscription segment? A LOT.

I estimate EBIT margins to be ~40%. Here's how.

Prime is a GREAT platform to launch all sorts of ancillary services and grab a greater wallet share.

So how profitable is the subscription segment? A LOT.

I estimate EBIT margins to be ~40%. Here's how.

20/ Prime subscription dollars (~$10 B) go directly to bottom line.

The other half (Music, Video, Audible etc) is obviously not such high margin business. I assumed -20% EBIT margin for this half of the business.

So the segment EBIT margin: ~50%*100% + ~50%*(-20%) = ~40%

The other half (Music, Video, Audible etc) is obviously not such high margin business. I assumed -20% EBIT margin for this half of the business.

So the segment EBIT margin: ~50%*100% + ~50%*(-20%) = ~40%

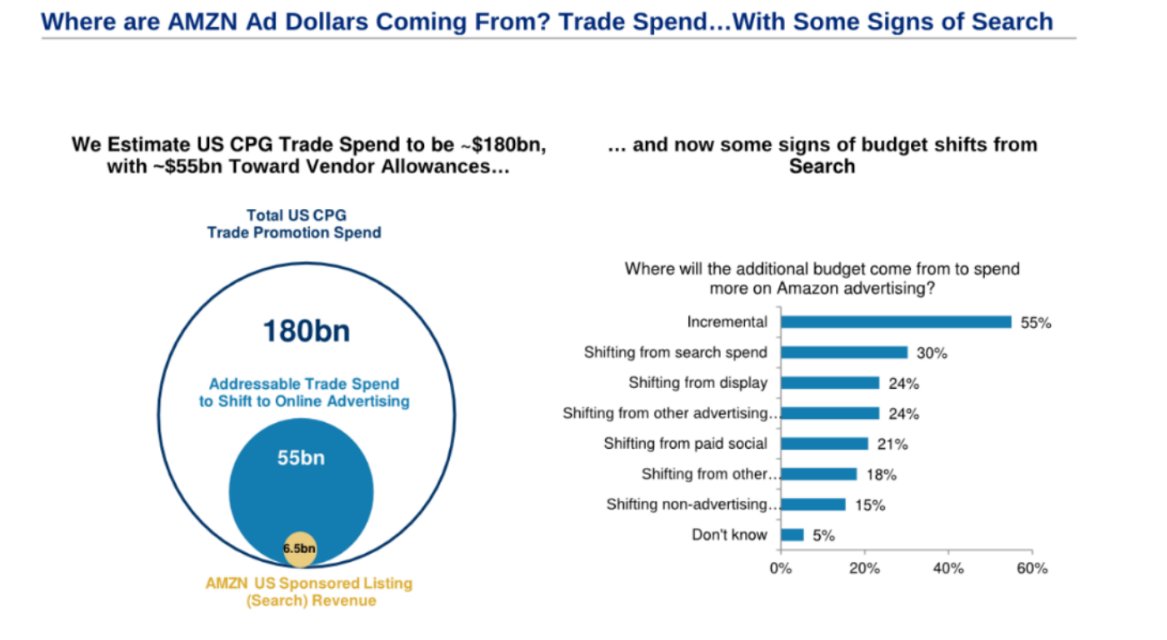

21/ Before I discuss AWS, I want to talk about the "other" segment first. "Others" is $14 B rev segment, ~80% of which is advertisement.

Relevant TAM for ad is NOT just global digital ad market, which itself is $130 B market dominated by and .

Relevant TAM for ad is NOT just global digital ad market, which itself is $130 B market dominated by and .

22/ MS on ad: “most of AMZN ad dollars are coming from traditional branded trade spend. These are dollars CPG brands/manufacturers pay to traditional brick and mortar retailers to promote inventory through their channels in the form of promotional/vendor allowance"

23/ How profitable is "other" segment?

5-yr avg EBIT margins for was ~43%. 's core commerce (~60% ad revenue) margin hovered between 35-55%. I assume ~40% EBIT margin for .

What about the rest 20%? throws a lot of darts at the wall (e.g. AMZN payment)...

5-yr avg EBIT margins for was ~43%. 's core commerce (~60% ad revenue) margin hovered between 35-55%. I assume ~40% EBIT margin for .

What about the rest 20%? throws a lot of darts at the wall (e.g. AMZN payment)...

24/...most (r all) of which is unprofitable. I assumed a punitive -50% EBIT margins for the rest of the segment.

So, Ad: 80% of other segment, EBIT margin: 40%

The rest: 20% of other segment, EBIT margin -50%

Overall margin for other segment: ~22%

So, Ad: 80% of other segment, EBIT margin: 40%

The rest: 20% of other segment, EBIT margin -50%

Overall margin for other segment: ~22%

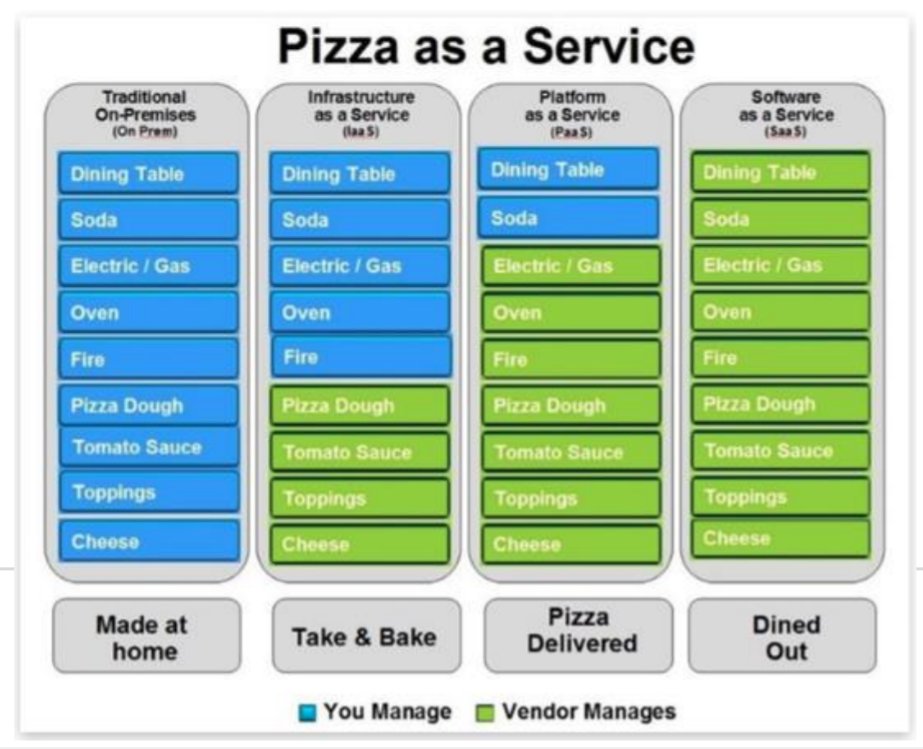

25/ Okay, now let's get to the juicy stuff: AWS.

is the undisputed leader in IaaS (Infrastructure-as-a-Service), and one of the major players in PaaS (Platform-as-a-Service). Instead of going all technical, let me just share this Pizza analogy that I came across to explain

is the undisputed leader in IaaS (Infrastructure-as-a-Service), and one of the major players in PaaS (Platform-as-a-Service). Instead of going all technical, let me just share this Pizza analogy that I came across to explain

26/ So how big is cloud market?

$1 T. Here's how:

Global IT spending: $2.8 T (IDC est)

Cloud TAM, excl. SaaS: $1 T (Bernstein)

Shift from on-prem to cloud 60-70% (JPM)

Current AWS relevant TAM $700 B

Assuming 3% IT spending growth, $1 T TAM in 2030

$1 T. Here's how:

Global IT spending: $2.8 T (IDC est)

Cloud TAM, excl. SaaS: $1 T (Bernstein)

Shift from on-prem to cloud 60-70% (JPM)

Current AWS relevant TAM $700 B

Assuming 3% IT spending growth, $1 T TAM in 2030

27/ Even if the competition is heating up from and , the fact is 10 yrs from now, hyperscale players , and MSFT will be market leaders (GOOG distant third). Given industry structure, they will have pricing power and all the SaaS companies, cloud is their COGS...

28/ ...and they will be at the mercy of and . Potential entrants will simply not stand a chance. There will be significant pricing power for MSFT and AMZN after Moore's law plays its course out.

So current competitive dynamics does not concern me.

So current competitive dynamics does not concern me.

29/ With the rise of multi-cloud and hybrid cloud strategy, is likely to gradually lose market share in IaaS,

but will remain market leader. Even if IaaS margin erodes, PaaS is likely to help maintain and possibly improve margin potential. Just see the below chart:

but will remain market leader. Even if IaaS margin erodes, PaaS is likely to help maintain and possibly improve margin potential. Just see the below chart:

30/ AWS posted $35 B topline in 2019 and here are its growth rates in last 5 yrs: 70%, 55%, 43%, 47%, 37% (oldest to latest)

How profitable is AWS?

A LOT.

This isn't retail. Oligopoly, mission critical infra., capital intensive. Not easy to just come in and compete.

How profitable is AWS?

A LOT.

This isn't retail. Oligopoly, mission critical infra., capital intensive. Not easy to just come in and compete.

31/ I estimate cloud will have ~50% penetration in 2030 (still early days). I expect to lose market share to (and some to ), but they will remain market leader. Even if the margin doesn't expand further, AWS itself (~$500B) explains ~60% of current valuation.

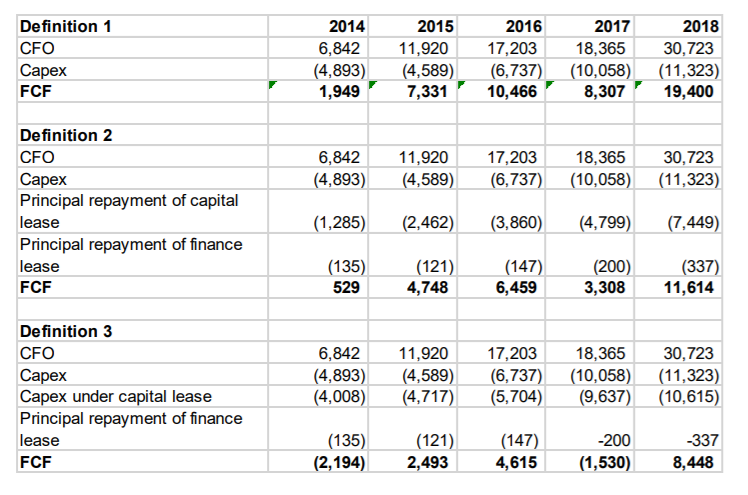

32/ When I was looking to value , I realized estimating cash flow is tricky because of different ways you can calculate cash flow for AMZN. AMZN itself provides three different definitions in its 10k (see table):

33/ There are a lot of unknowns and assumptions needed (more than usual) for valuing . Therefore, I used definition 3 to estimate FCF, the most conservative definition. I said to myself I will invest only if it makes sense from this restrictive FCF measure.

34/ And it does make sense "to me" (emphasis).

There are obviously lots of risks. Escalating shipping costs, failure in international markets, degrading customer experience because of increased ad load, antitrust concerns come to mind.

There are obviously lots of risks. Escalating shipping costs, failure in international markets, degrading customer experience because of increased ad load, antitrust concerns come to mind.

35/ Overall, there are perhaps not too many companies out there which are as well positioned as for next 5-10 years.

Remember, take investment decisions on your own.

RT if you learned something.

Remember, take investment decisions on your own.

RT if you learned something.