In the run up to EMU, 2 famous views dominated. The 'economists' thought that real economic convergence ought to occur before monetary unification. The 'monetarists' thought that nominal convergence could drive real one (endogenous OCA theory and all that). 2nd view prevailed 1/

The 1st decade of EMU proved the economist right. Nominal convergence let to massive real divergence, imbalances accumulated although - except in the case of Greece - they were not fiscal. Fiscal rules worked, but we did not have rules to keep other macro imbalances in check 2/

Then the crisis hit. Private debt migrated on public balance sheets, and what did NOT start as a public debt crisis morphed into one. That's when the "sinners vs saints" rhetoric became the predominant interpretative framework for the EZ crisis. 3/

Except the 'sinners' (🇬🇷 and 🇮🇹excluded) had stellar public finances before 2010, and in terms of their other macroeconomic imbalances they did not 'break' any rules - as rules didn't exist. Most of it was the result of what economists welcomed as 'capital flowing downhill'. 4/

Yet, at that time you could still argue (although wrongly, in my view) that some countries had brought this on themselves. The ASYMMETRIC nature of the Eurozone crisis provided plausible deniability to the concern with moral hazard and the obsession with 'legacy assets'. 5/

The asymmetric nature of the EZ crisis is reflected also in the characteristic features of the tools we equipped ourselves with to fight it. ESM lending tools are all subject to MoUs or some degree of macroeconomic conditionality. 6/

ECB OMT is 'monetary policy with conditionality', whereby the Central Banks effectively subjects part of its action to an exogenous political decision. The risk from ECB's ELA is re-rooted nationally, QE is capital key based and issue/issuer limited not to be too asymmetric. 7/

This framework is wrong for addressing the COVID crisis, because this a global exogenous shock that nobody brought on themselves, but that can still have asymmetric effects on countries' market access / debt sustainability, based on what physicians call pre-existing conditions 8/

High-debt countries are going to be more exposed - including those who made herculean adjustment to their economies since 2010. Yet, this time the risk has nothing to do with how they managed their economies / what economic policy they took. 9/

As a matter of fact, the Eurozone "north" and "south" has literally never been closer in macroeconomic terms during the past 20 years than they are today (we talked about it here ⬇️) and this has been the result of a unilateral adjustment in the South 10/ media.algebris.com/algebris_polic…

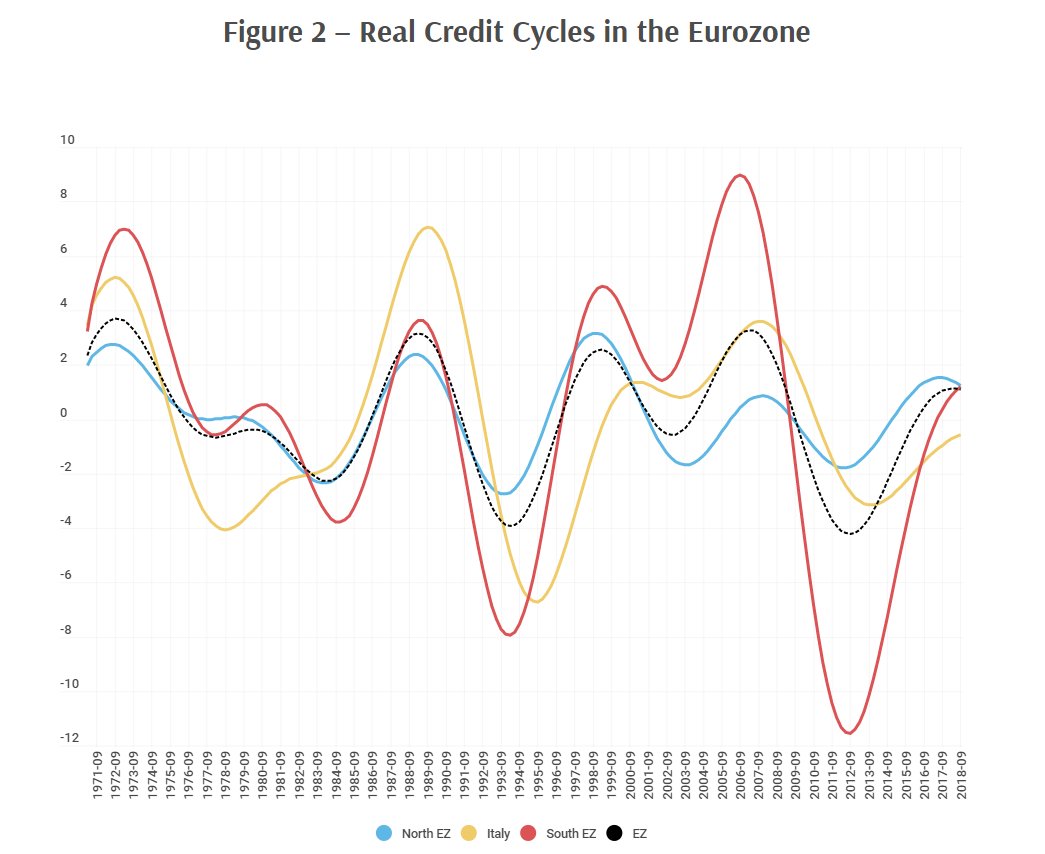

📊By unilateral adjustment I mean this ⬇️ (just a few pictures). The Eurozone crisis has led to what the pre-EMU 'economists' advised: real convergence of a staggering speed and magnitude. 11/

📈Real convergence means that today, contrary to the first 10 years of currency unification, interest rate prescriptions from a simple Taylor Rule would be remarkably homogeneous across the EZ, thus making the job of single monetary policy easier. 12/

📈It also means that financial and credit cycles are today aligned across north and south. This is key, because it means that today financial integration no longer drives economic asymmetry (algebris.com/policy-researc…). 13/

We moved from a world of one-size-fits-none to a world of one-size-fits-most. The rationale for moral hazard concerns is per se much weakened in the second kind of world than in the first. To this, add the fact that the shock we now face is entirely exogenous and symmetric 14/

The ECB PEPP programme is a good response to the immediate emergency, because it provides states with a safety valve for the debt that they will need to issue to fund the health response AND the need to freeze economies for months without bankrupting them. 15/

But, what happens after emergency is over? That debt will remain on MS balance sheets (because this is still national debt). Will that debt - which was incurred to fight covid crisis - be counted towards EU fiscal rules (that will be switched on)? How will markets price it? 16/

Again, what started this time as a purely exogenous and symmetric shock may turn out to have very asymmetric consequences ex post, completely unrelated from countries' economic management. Here's where the rational for mutualisation comes in. 17/

Best way to avoid such outcome would be to issue eurobonds backed by a common fiscal capacity, which does not exist and probably won't come into existence soon enough - because it would require among other things amending TFEU and ratify it (the poisoned chalice). 18/

One alternative, could be to mutualise the *additional* covid-related debt à la red/blue bonds proposed by @jakob_eu et al back in the days. You agree on 'corona debt' being mutualised as the expression of the common catastrophe we faced together. 19/

2ns best is to have ESM issue supra-national corona bonds and fund unconditional credit lines to MS. Those loans will remain as debt on MS balance sheet, but if maturities are v long and interest v low, refinancing risk is lower than having same debt but all mkt-financed. 20/

So long story short: I think the corona crisis calls for mutualisation, not so much to deal with the immediate emergency but to avoid that the higher debt needed now resurfaces the economic divergence that we have overcome. 21/

But what about Italy, you will say? 🇮🇹 is in many respects a case of missed adjustment on many fronts (and many of those charts). Most of it coming from the unresolved internal north/south divide. Yet, I believe Italy will emerge out of this a deeply transformed country. 22/

Economically, nothing like this shock can convey the urgency of adjusting in good times to have more policy space in bad ones. Cohesion around internal solidarity will also be harshly tested. And as far as Euroscepticism is concerned, this is THE make or break moment. 23/

The rest of Europe will admittedly need to do an act of faith in the country that today is its weakest link, if it was decided to pursue mutualisation as discussed above. But if instead it decides to let Italy go now, there will certainly be no coming back from this. end/