🇺🇸 Economic impact of the infrastructure & #BuildBackBetter plans.

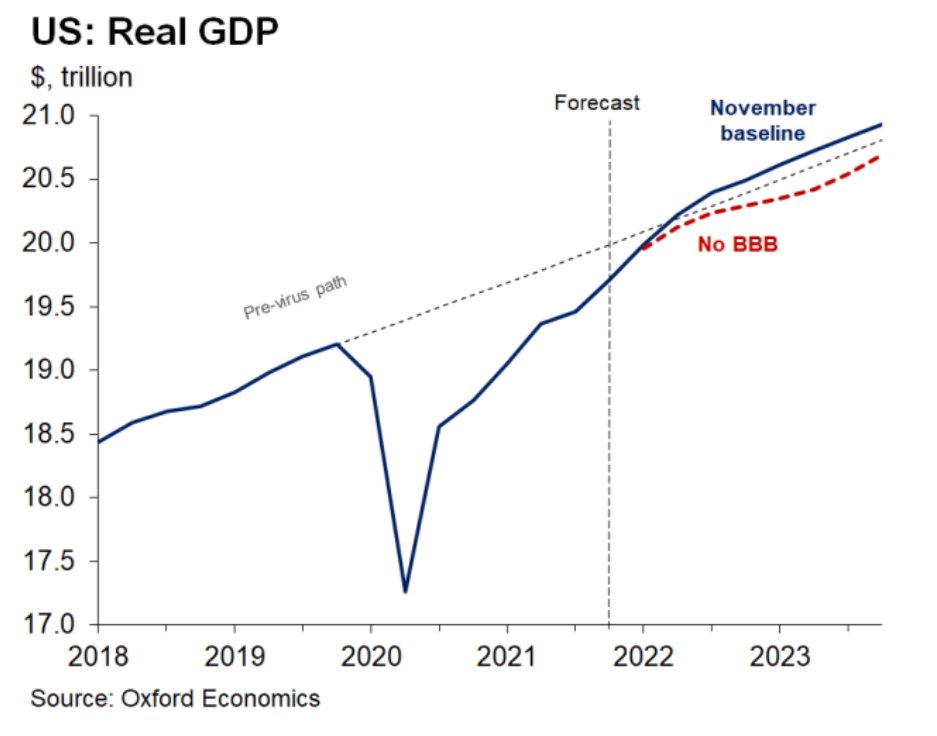

Our November baseline forecast includes both the bipartisan #infrastructure package and a $1.8tn BBB bill consisting of spending on social programs and climate initiatives via @OxfordEconomics

Our November baseline forecast includes both the bipartisan #infrastructure package and a $1.8tn BBB bill consisting of spending on social programs and climate initiatives via @OxfordEconomics

The $1.2tn #Infrastructure and Investment Jobs Act (IIJA) provides $550bn in new spending over the next 10 years.

We estimate it’ll boost #GDP growth by 0.1ppt in 2022 and 0.3ppt in 2023, with a cumulative 150,000 new jobs by the end of 2023.

We estimate it’ll boost #GDP growth by 0.1ppt in 2022 and 0.3ppt in 2023, with a cumulative 150,000 new jobs by the end of 2023.

Given that shovel-ready projects are a myth, we anticipate government outlays will only increase gradually, and the impact on #inflation will be minimal

The House has passed its version of #BuildBackBetter, and the legislation now heads to the Senate.

While we expect BBB to ultimately pass, we expect it will undergo some changes in the Senate to secure the votes of all 50 Democrats.

While we expect BBB to ultimately pass, we expect it will undergo some changes in the Senate to secure the votes of all 50 Democrats.

We estimate the #BuildBackBetter package would increase real GDP growth by 0.4ppt in 2022 and 0.5ppt in 2023 and add about 750,000 jobs to the economy by the end of 2023

#BuildBackBetter wouldn't meaningfully add to current inflationary pressures: price levels a marginal 0.2% higher by end-2023

Unlike $5.5tn #Covid relief measures passed over the past 18mo, most BBB’s outlays would be spread across 10yrs & offset by tax increases & spending cuts

Unlike $5.5tn #Covid relief measures passed over the past 18mo, most BBB’s outlays would be spread across 10yrs & offset by tax increases & spending cuts

What’s more, about $300bn of the new spending represents a continuation of existing programs, averting a fiscal cliff for many households in 2022 rather than boosting their income

• • •

Missing some Tweet in this thread? You can try to

force a refresh