🇺🇸 #GDP thread

There are only so many ways to spin old data in a rapidly evolving #COVID19 environment.

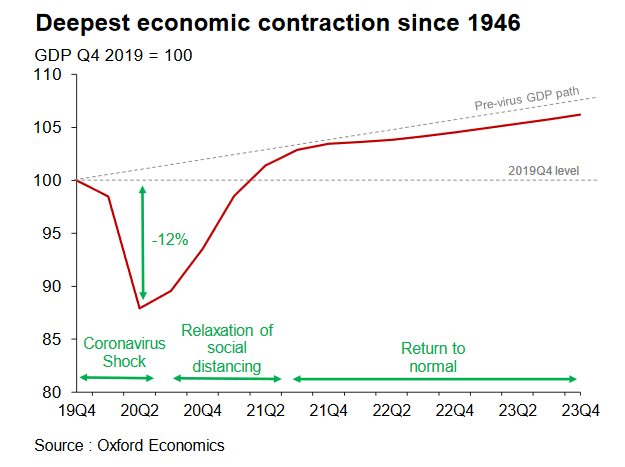

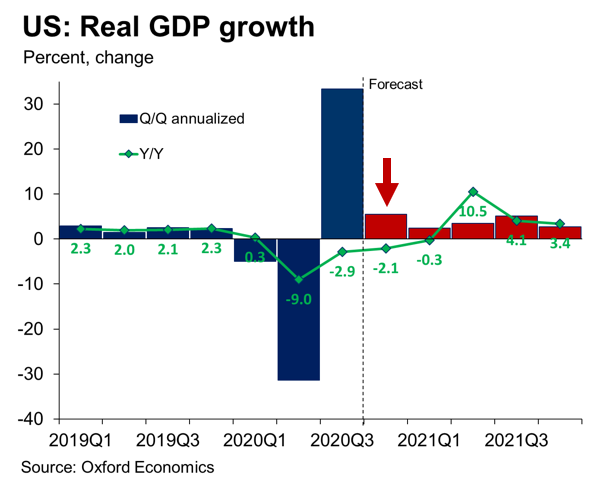

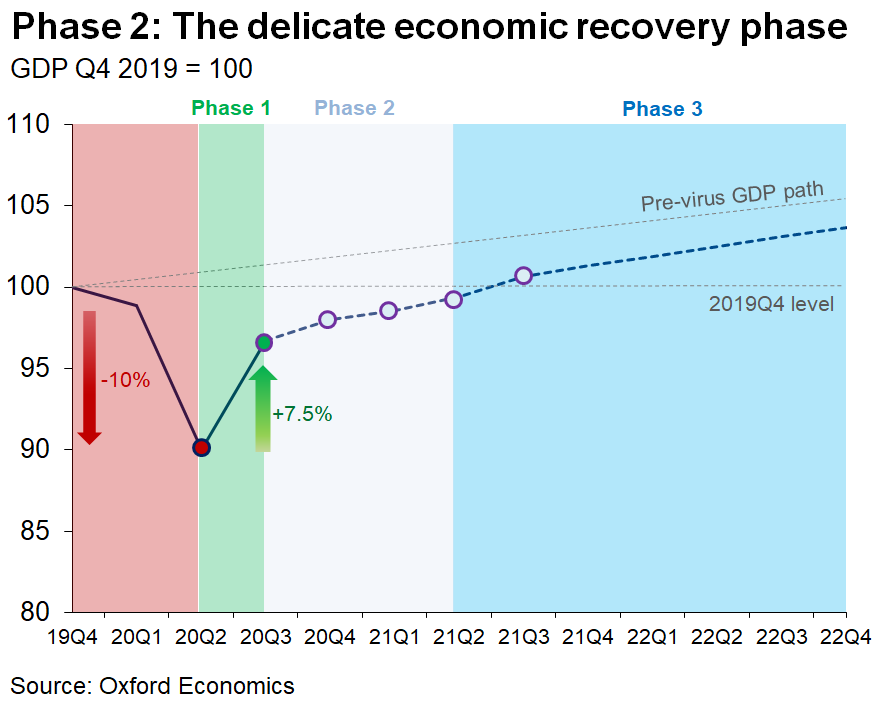

The economy grew an upwardly revised 7.5% (⬆️0.1ppt) or, 33.4% annualized (⬆️0.3ppt) in Q3 – recouping 2/3 of Covid output loss.

Still, remained 3.4% smaller than end 2019

There are only so many ways to spin old data in a rapidly evolving #COVID19 environment.

The economy grew an upwardly revised 7.5% (⬆️0.1ppt) or, 33.4% annualized (⬆️0.3ppt) in Q3 – recouping 2/3 of Covid output loss.

Still, remained 3.4% smaller than end 2019

The strong Q3 #GDP performance gives a false impression of the economy’s true health.

Much of Q3 gain came from carry-over effects from fast progress in May-July while real GDP remained down 2.9% y/y in Q3.

Much of Q3 gain came from carry-over effects from fast progress in May-July while real GDP remained down 2.9% y/y in Q3.

With most of Q4 in the books, we expect ongoing but much slower #GDP growth around 1.5% (or, 5.5% annualized) in the final quarter of the year.

Still, that will also reflect much stronger entering Q4 than the current underlying pace of activity

Still, that will also reflect much stronger entering Q4 than the current underlying pace of activity

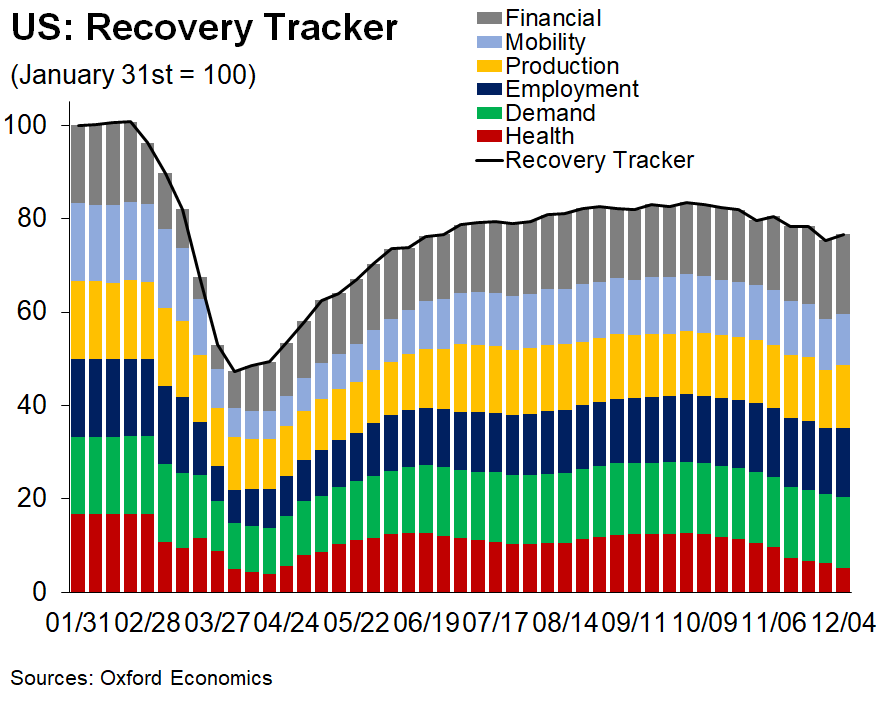

On the eve of 2021, the economy carries very little momentum as a catastrophic third #COVID19 wave is limiting mobility, curbing employment & constraining demand.

> We should be prepared for very weak economic readings in December

> We should be prepared for very weak economic readings in December

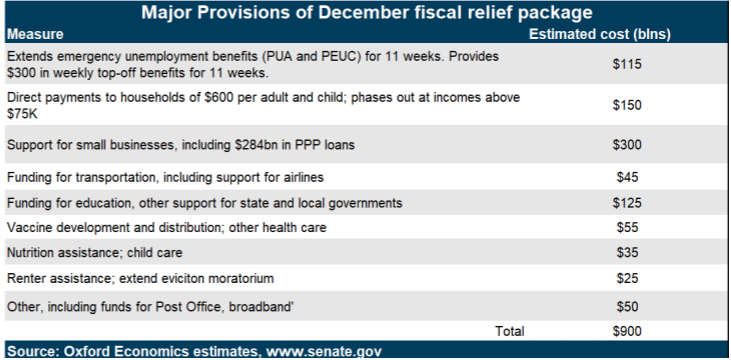

The $900bn #COVID19 relief package is months late & will likely fall short of what is needed to prevent a rough winter, but it’s better than nothing.

It'll help partially buffer the current economic slowdown & provide + economic dynamism during the initial #vaccine rollout phase

It'll help partially buffer the current economic slowdown & provide + economic dynamism during the initial #vaccine rollout phase

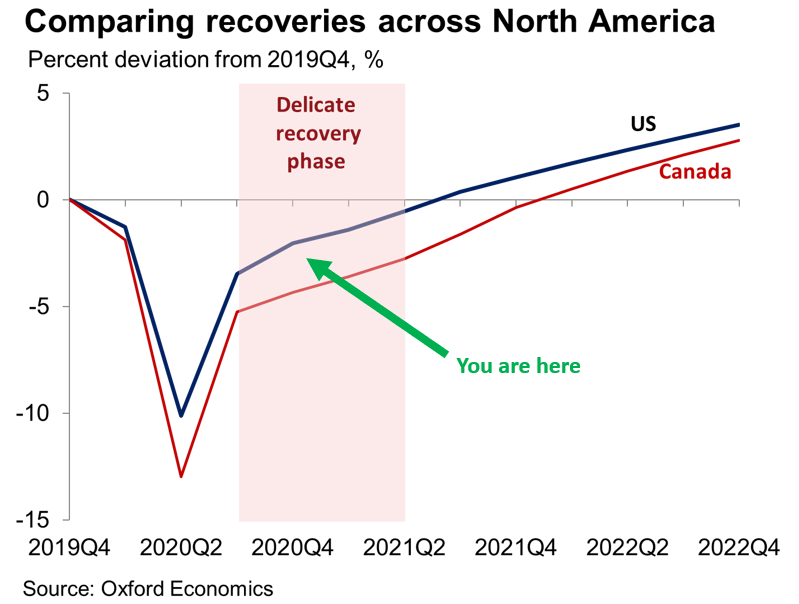

As we gaze into 2021, the outlook will be one of contrasts.

The economy will start the year gingerly, and it’ll be prone to hiccups during the delicate vaccine diffusion phase.

The economy will start the year gingerly, and it’ll be prone to hiccups during the delicate vaccine diffusion phase.

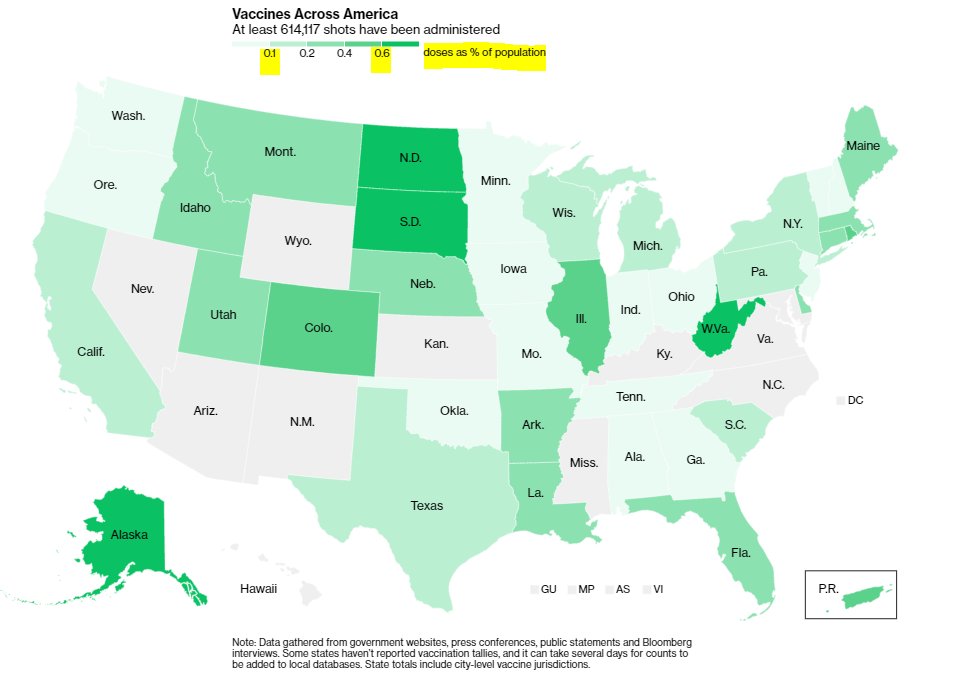

Vaccinations began Dec.14 :

So far, 614,117 doses have been administered, according to nationwide tally from @CDCgov.

That's about 0.2% of the population.

#Vaccine tracking feature via @business

bloomberg.com/graphics/covid…

So far, 614,117 doses have been administered, according to nationwide tally from @CDCgov.

That's about 0.2% of the population.

#Vaccine tracking feature via @business

bloomberg.com/graphics/covid…

As we approach Phase 3 of the recovery, the cocktail of increased government transfers & broad-based vaccinations should support gradually firming activity culminating in a mini-summer boom

Still, the outlook will be one of contrasts

Much of the fiscal aid for the $900bn #COVID19 relief will expire before full recovery:

- renters eviction protection Jan 31

- PUA, PUEC unemployment benefits March 14 phase out

- FPUC ($300/week UI top-up) March 14

- PPP through March

Much of the fiscal aid for the $900bn #COVID19 relief will expire before full recovery:

- renters eviction protection Jan 31

- PUA, PUEC unemployment benefits March 14 phase out

- FPUC ($300/week UI top-up) March 14

- PPP through March

• • •

Missing some Tweet in this thread? You can try to

force a refresh