I've seen quite a bit of "fishing for truth" about the interlocking topics of network effects, technology standards, platforms/two-sided markets, and blockchains recently, so it might be worthwhile untangling the lot.

TLDR: There's still a massive amount of confusion reverberating through the field, with sloppy definitions and the penchant to peddle old and largely false folk tales taking the brunt of the blame. Kinda ironic bc "path dependency" is a core concept.

The common impetus for the work in this field is to challenge the underlying assumption of consumer choice theory in standard microeconomics that individuals make choices disconnected from each other and reap utilities disconnected from each other.

Early work, concurrent with the emergence of game theory, focused on the potential of conflict (see Schelling's 1960 book), but the next step was to recognize that mutually synchronized choices can also provide benefit to each other.

Schelling's 1970 work and especially his 1978 book mark a starting point into understanding the roles of "benefits from interaction" and "structure of interaction", including this illustration of a critical mass model.

Notably, Schelling didn't write about technology at all, his models of "benefits from agreeing on things" tend to come from everyday social interaction. He also didn't dip his work in mathematese, so it didn't get all that much attention early on.

There was a flurry of activity in the mid 1980s focusing on technology, still pre-WWW: Dybvig/Spatt on "adoption externalities", Katz/Shapiro on "network externalities", Farrell/Saloner on "technology standard choice", David on "path dependency", Arthur on "increasing returns".

A lot of the confusion emanates from this period, markedly bc 1. terms were fixed while concepts were still being worked out, 2. illustrative examples ("VHS vs Beta") turned out to be very iffy, and 3. the discussion quickly descended into a fight over "Y no best technolgy win".

To illustrate the point, one of the early claims was that Beta lost even tho it was the better tech. That's nonsense, technically they were more or less the same, Beta used smaller cartridges and VHS had longer runtimes, plus Sony had a different licensing model than JVC.

For the first few years roughly 1/3 preferred Beta and 2/3 preferred VHS. If there was any interaction effect it was purely local, swapping cartridges with friends & family drove adoption choice. Network effects were barely noticeable, standard choice theory worked just fine.

Things only came to a head with the explosion of video rental and the subsequent collapse of the wildcat rental industry which killed Beta. Notably, this wasn't driven by consumer interaction but by studio plus rental store choice second on which movies to carry in which format.

So applying network effects to that dynamic only works if we consider the whole ecosystem as a P2P network with some players, in this case the "middlemen" of studios and rentals, holding much more influence than others. Notably, Sony moved into the studio biz at the time.

This gave rise to the concept of "indirect network effects" meaning inter-consumer benefits are mediated by producers or other supply side players. This will become important later on when we talk platforms but it's also still largely the only effort to incorporate structure.

Most notably, the original definition of "network externalities" expressly excluded the role of structure, so it wasn't a network effect at all but a group size effect.

But there's a huge gap between "demand side economies of scale" and "inter-consumer complementarities" which get glossed over here. I'm still under the impression that most economists, even in the field, are only dimly aware of how graph theory could help sort these things out.

To make things even more complicated, there's the parallel attempt, mostly within tech circles, of conceptualizing these phenomena. "Metcalfe's Law", expressed in the 1980s but published in the 1990s, suffers from the same problem of assuming a fully connected network.

[More confusion in a side bar: in graph theory, a network is a type of a graph where nodes and edges are assigned values, typically reflecting stocks, flows, or constraints. In real life, almost all graphs are networks, so the distinction is almost completely moot.]

Scrolling forward a bit, as @kwerb mentioned, things went into overdrive in the 1990s when the internet exploded, the browser wars heated up, and people beyond the nerdy corner of the econ department realized there was something happening, but didn't want to read the papers.

Two Berkeley econ profs, Hal Varian (now Google's chief economist) and Carl Shapiro (co-inventor of network effects), decided to ride the trend and publish "Network Rules", a book targeting the MBA/VC audience. Tellingly, the book was released in 1999 but carried a ©2000 mark.

If the debate wasn't politicized enough yet, the browser wars got a lot of people to chime in on the welfare ramifications of network effects and standard choice. Surprisingly there was a strong tendency to interpret the facts according to the observers' ideological leanings.

So we have the rare case of a theory both confirming and contradicting itself. In a world of ambiguous evidence, people tend to lean on their ideological peers for the "correct" interpretation of the facts. As the saying goes, ideology is the science of what goes with what.

On no, that doesn't constitute a natural monopoly, but it allows for two or more incompatible "truth networks" to survive and stabilize. Networks are not monopolies but clusters with frayed edges. (This would be my #1 on the list of what people still get wrong about networks.)

Another source of confusion on the econ side is the tendency to subject technology adoption processes to the comparative statics analysis from textbook micro, even if that doesn't make sense at all. Textbook markets deal with uniform unchanging products. Technologies are neither.

Phase 2 of the timeline starts around 1999/2000, both with the popularization of "Network Rules" and the boost the sociology of network field got from Duncan Watts' Six Degrees models. Networks in sociology go back to Mark Granovetter, but had been in hibernation at the time.

This wasn't only dot-com boomtime when MBAs and JDs skipped I-banking jobs for SV startups, but also the early days of Napster, P2P, and social networks like Orkut or Friendster. Direct network effects were all the rage.

Direct network effects are social effects, and technology mostly amplifies interactions across cyberspace and facilitates making new connections via likemindedness, be it via Flickr, MMO gaming, or Hotornot spinoffs. But social networks exist and have already existed offline too.

Where technology comes in is that in order to participate in this new form of interaction, peers have to adhere to a set of technical requirements and also promise to adhere to a set of social rules, which tend to be much squishier and much harder to enforce.

The second half of the 2000s was mostly devoted to recognizing both the necessity and the profitability of rulemaking (and the pains of rule-enforcing at scale). This isn't altogether new, the "formula" in Formula 1 refers to the rules teams have to adhere to in order to compete.

Both Silicon Valley VCs and IO economists went back to looking at indirect ("market-mediated") network effects as a catalyst to both harness and reap value from direct network effects. The 2010s so far have been the decade of "two-sided markets".

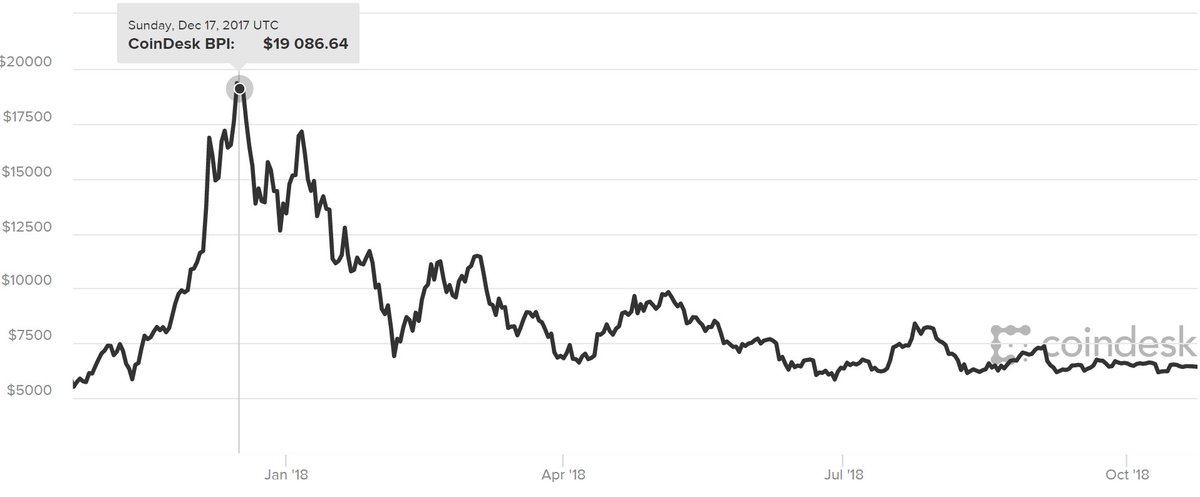

I posted about the "Class of 2009" before, Uber and Airbnb, the stalwarts of the sharing economy, and Bitcoin came into being at roughly the same time. They all center around the same model: a central technology standard to facilitate a directed P2P interaction.

Retroactively we realize that earlier platform or social media business models run on the same principle of optimizing the matchmaking algorithm between supply and demand for information: Google for web content, Facebook for social news and trivia.

In 2015, Tom Goodwin somewhat breathlessly realized that Uber owns no cars and Airbnb no hotel rooms, yet they reached billion $ valuations. Confusingly, he described this model as "disintermediation". Quite the opposite: Uber and Airbnb are intermediates in markets they created.

Controlling the central matchmaking algorithm is a potentially lucrative endeavor, and so is the ability to tweak it in order to maximize firm profits subject only to ensuring ongoing participation (in marketingspeak that's known as "barely satisfied customers").

Even though indirect network effects have been described 30+ years ago, their combination with technology platforms as two-sided markets is new enough to still be in a state of advanced confusion, which creates a whole bunch of problems if it's been dragged to the Supreme Court.

The biggest problem with capturing intermediaries from a welfare perspective is that it undercuts the whole economic model of a market. Is the counterfactual a frictionless market doing the intermediary's work, or no market at all?

Bitcoin of course went a few steps further than Airbnb and Uber in an attempt to solve the "middleman problem": the central algorithm is openly available to be tweaked via social consensus, operations is outsourced to a bidding/lottery process and incorporation is dispensed with.