,

11 tweets,

4 min read

Read on Twitter

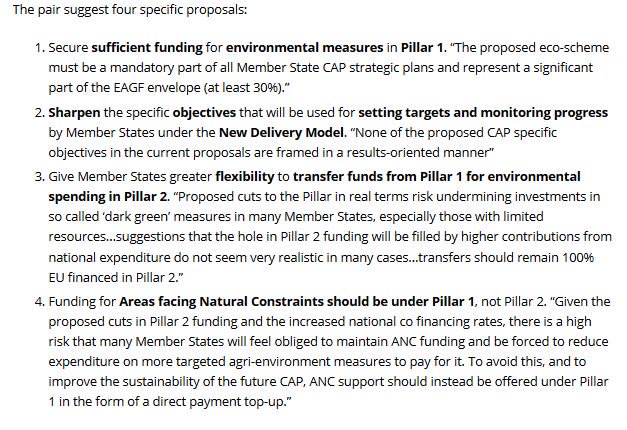

Treasury Issues Final Rules and New Proposed Guidance on Eligibility for 20% Deduction for Small and Mid-Size Businesses

@drawandstrike @catesduane @rising_serpent @almostjingo @tracybeanz @TheChiIIum @Quodverum_ @DRUDGE_REPORT @thomaswictor @TheJonGrubb

justtherealnews.com/2019/01/18/tre…

@drawandstrike @catesduane @rising_serpent @almostjingo @tracybeanz @TheChiIIum @Quodverum_ @DRUDGE_REPORT @thomaswictor @TheJonGrubb

justtherealnews.com/2019/01/18/tre…

Washington – Today, the U.S. Department of the Treasury issued final regulations and other guidance on a substantial provision of the Tax Cuts and Jobs Act, which allows owners of sole proprietorships, partnerships, trusts,

and S corporations to deduct up to 20 percent of their qualified business income.

The final regulations ensure that this historic tax cut will be available to the broadest spectrum of American businesses, consistent with the law, while minimizing compliance costs and streamlining the process for claiming the deduction.

“Small and mid-size businesses are the engines of growth for the U.S. economy,” said Secretary Steven T. Mnuchin. “The pass-through deduction will drive more investment in U.S. companies and higher wages for American workers.

This provision will reduce pass-through business tax rates to their lowest rate in more than 80 years.”

It is estimated that between 17 and 40 million American business owners will be able to take advantage of this deduction.

It is estimated that between 17 and 40 million American business owners will be able to take advantage of this deduction.

The deduction is generally available to small business owners with income below $315,000 for married couples filing jointly and $157,500 for single filers without limitations.

For business owners above those thresholds, the regulations also provide certainty and flexibility by clarifying the definitions of “specified service trade or business” and “unadjusted basis immediately after acquisition” of qualified property,

and by including “aggregation rules” for filers with pass-through income from multiple sources. Treasury also issued a revenue procedure on computing W-2 wages for purposes of the limitations that apply to owners with income above the threshold amounts.

The Treasury issued further related proposed regulations that provide further certainty for determining the deduction for REIT dividends taxpayers own through mutual funds and a proposed revenue procedure providing a safe harbor,

so that certain rental real estate enterprises may be treated as a trade or business for purposes of the deduction.