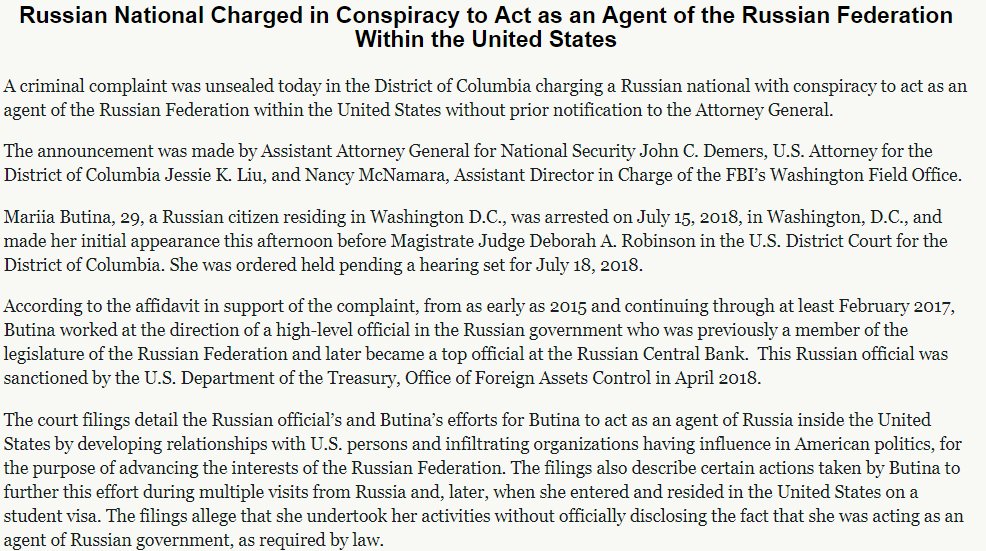

,

30 tweets,

4 min read

Read on Twitter

The @OECDtax just dropped their consultation document on taxation of the digitalising economy. Lots of new details in here … let’s read it together. oecd.org/tax/beps/publi…

The document outlines three approaches under the banner of ‘revised profit allocation and nexus rules’ (that was Pillar 1 from the two-pager). And a fourth proposal on ‘global anti-base erosion) (aka Pillar 2).

The first Pillar 1 proposal is about ‘User Participation’. Its thesis: users create value, especially for social media, search engines, and marketplaces. So you need to allocate taxing rights to countries where users are.

This is hard to do. TP’s not up to it (here’s the ‘beyond the ALP’ stuff we were all so hyped about); instead it’s suggested that countries adopt a ‘non-routine or residential profit split approach’.

You work out the residual profits of a business and then apportion them to ‘the value created by the activities of users, which could be determined through quantitative/qualitative information, or through a simple … percentage’.

(Significant that this is left open, bc working out where users of digital services are is hard … I have a story forthcoming on this)

Once you’ve apportioned taxing rights to the countries where users are, nexus pretty much drops out of the picture. No need for any PE whatsoever.

A last point on the first Pillar 1 proposal: because it’s such a hassle to administer, it’s suggested it may be applied ONLY to social media, search, and platforms.

That’s a big drawback as I see it. These three categories barely existed 15 years ago; what will the Internet look like in another 15? So it looks pretty brittle and inflexible.

On to the second Pillar 1 proposal: ‘marketing intangibles’.

The idea here is that marketing intangibles ‘are reflected in the favourable attitudes in the minds of customers and so can be seen to have been created in the market jurisdiction’. Same with other intangibles like customer data.

So the proposal would alter TP rules to allocate these intangibles to the market jurisdiction. You can’t just keep them wherever you want them: they’re linked to (a theme is emerging here…) where users are!

How do you accomplish this? Folks, it is hard. Again it rests on the allocation of non-routine or residual income to market jurisdiction.

This is both wider (bc applying to more companies) and narrower (bc it’s not junking TP rules, at least conceptually) than the ‘user participation’ proposal, as I read it.

There is a proviso that you could work out income allocation based on ‘a revised residual profit split analysis’ rather than the more familiar TP rules. The door is visibly ajar to what we can call formulary apportionment.

And in a recognition of the massive disputes all this could produce, the proposal calls for ‘the possibility of early certainty on the taxation’ for businesses. Er, bon courage on that

On to Pillar 1’s third proposal: ‘significant economic presence’.

This goes way beyond what we would think of as ‘economic nexus’ (a simple revenue threshold). ‘Revenue generates on a sustained basis is the basic factor, but such revenue would not be sufficient in isolation to establish nexus.’

That’s supplemented by a salad of ‘one or more’ of these ingredients: user base; ‘volume of digital content’; billing in local currency; website in local language; responsibility for goods delivery (facilitation to you or me); sustained marketing activity.

Okay, so you establish nexus with your salad. Then to work out apportionment you (1) define the base, (2) determine ‘allocation keys’ [salad ingredients?] to divide it; (3) decide how to weight the keys.

‘The tax base could be determined by applying the global profit rate of the MNE to the revenue (sales) generated in a particular jurisdiction.’ 🤔

Not much nitty gritty here, to be honest. Proposals 1 and 2 raise a lot of questions, for sure, but they seem quite a bit more thought-through.

The report then helpfully compares the different proposals. I’m going to skip ahead though to the Pillar 2 proposal.

This is the one that France and Germany are pushing. The two big ideas here are an income inclusion rule and a tax on base-eroding payments (aka global minimum tax).

These ideas are pretty familiar (not least from BEAT and GILTI), but it’s still pretty amazing to see them spelled out here in technocratic detail.

Having said that, the report is heavier on the conceptual framework (how the rules would interact with tax treaties, etc) than the ‘juicy’ details of, for instance, the potential rate. Various concerns about double taxation are also flagged.

Okay, that’s pretty much the document. My first thought: the second proposal in Pillar 1 may be challenging technically but it has one massive strength that the first lacks …

… namely that the challenges of taxing the digital economy aren’t really about the digital economy at all. They’re really to do with intangibles, and the massive increase in their importance since the 80s/90s.

What’s so impressive about the ‘marketing intangibles’ proposal is its breadth. By not ring-fencing ‘digital companies’ (whatever they are) it offers a wider solution and looks a lot more future-proof than the first proposal. /fin

And the story is up: internationaltaxreview.com/Article/385807…