,

19 tweets,

6 min read

Read on Twitter

The three pages of text in this @OECDtax policy note may be more significant than the thousands that made up the BEPS project

oecd.org/tax/internatio…

oecd.org/tax/internatio…

The BEPS project failed before it began, despite the best efforts of many committed OECD staff, because the most powerful member states ruled out dropping the arm's length principle at the outset - so BEPS could only ever offer a sticking plaster or two to a broken system

But even those OECD member states realised by the end of BEPS that it had failed - that they had made it fail. US and EU developed their own proposals that *did not* rest on the arm's length principle - having denied that possibility to the rest of the world in BEPS

But the economic illogicality of the arm's length principle is too strong: you can't build a tax system on the assumption that intra-group transactions take place at market (arm's length) prices, when multinationals exist precisely so that these prices need not apply

That is, the economic rationale for multinationals is that they exist where internalising transactions is more efficient than having them occur between myriad separate entities operating at, yes, arm's length

The predictable and predicted (by @TaxJusticeNet at least) failure of BEPS reflected the incompatibility of the arm's length principle with reality, and with the single agreed BEPS goal: to reduce misalignment between the locations of real economic activity and of profits

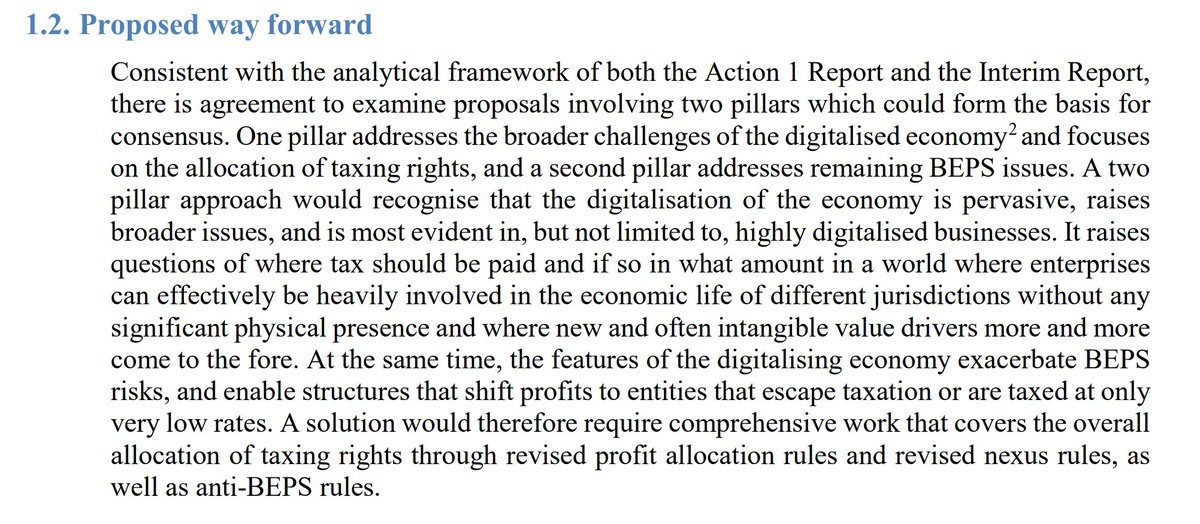

The @OECDtax policy note is the public statement that arm's length pricing is done, finished, toast. "Comprehensive work on the allocation of taxing rights"? Yes please!

What's next? Well, @OECDtax will push on with this effort - looking at rules for digital tax, but with their biggest members pushing competing alternatives for broad, radical reform. See e.g. @YohannesBecker writing on some of these developments for us: taxjustice.net/2019/01/15/the…

And while the OECD struggles to keep up with its fickle members, the tax debate is rapidly picking up pace elsewhere... Executive directors of @IMFNews will shortly finalise an important position paper on alternatives to the OECD tax rules - including unitary/formulary options

Lower-income countries are increasingly demanding, and having, a voice - including powerful new thinking at the G24... (watch this space)

And many eyes are on the 'Inclusive Framework' - designed to bind lower-income countries to a BEPS agreement they had little influence over, it could provide a channel to ensure their meaningful contribution to the more radical solution coming. (Tho don't hold your breath...)

One thing for sure: we're closer now than ever before to the kind of open, global discussion of tax rules that could finally redress some of the glaring inequalities in the distribution of taxing rights that lower-income countries face.

Nothing is guaranteed - as with scorpions crossing rivers, nobody should expect OECD members to give up their excess rule-setting power, nor their excess taxing rights, without a battle.

But big shifts are underway, and the forces released will not easily be stopped.

Consider:

1. The arm's length principle has lost its monopoly.

2. Will the OECD's monopoly go with it? (Has it already?)

3. Can lower-income countries still be held to OECD discipline?

Consider:

1. The arm's length principle has lost its monopoly.

2. Will the OECD's monopoly go with it? (Has it already?)

3. Can lower-income countries still be held to OECD discipline?

Outside the global policy debates, here's one thing to watch. As the arm's length norm crumbles, which country or group of countries will unilaterally introduce unitary tax and formulary apportionment? And will it be as outright (a la CCCTB), or as an alternative minimum tax?

A formulary alternative minimum corporate tax, or FAMICT - as proposed by @TaxJusticeNet and @icrict (who incidentally have done so much to normalise the end of the arm's length principle): taxjustice.net/2018/02/07/icr…

The potential for an explosive splintering of tax rules and norms is also high, of course. OECD dominance is ebbing, and there are substantial divisions among major economies - to say nothing of the typically voiceless countries where the majority of the world's population live

One important, and easily delivered priority now: make multinationals' country-by-country reporting data public, for all to see. This will ensure a common evidence base for proposals, and ultimately support progress towards a fairer distribution of taxing rights globally

@threadreaderapp unroll please