,

13 tweets,

5 min read

Read on Twitter

A short thread on an updated WP published in @nberpubs: Testing the effectiveness of consumer financial disclosure. With @stefanhunt, Christopher Palmer (@MITSloan) and Redis Zaliuaskas. #EconTwitter #BehavioralEconomics #RCT (1/n)

Savings accounts are widespread (93% of UK pop.) and important (deposits total ~£700bn). Instant access savings accounts are the most common form of saving in the UK and are relatively simple - most people say the interest rate is the most important feature (2/n)

Accounts typically provide a high introductory interest rate in the 1st year (“front book”) but lower rates in subsequent years (“back book”). Despite this and despite being easy to switch (15 minutes on average), a 3rd of deposits sit in accounts more than 5 years old (3/n)

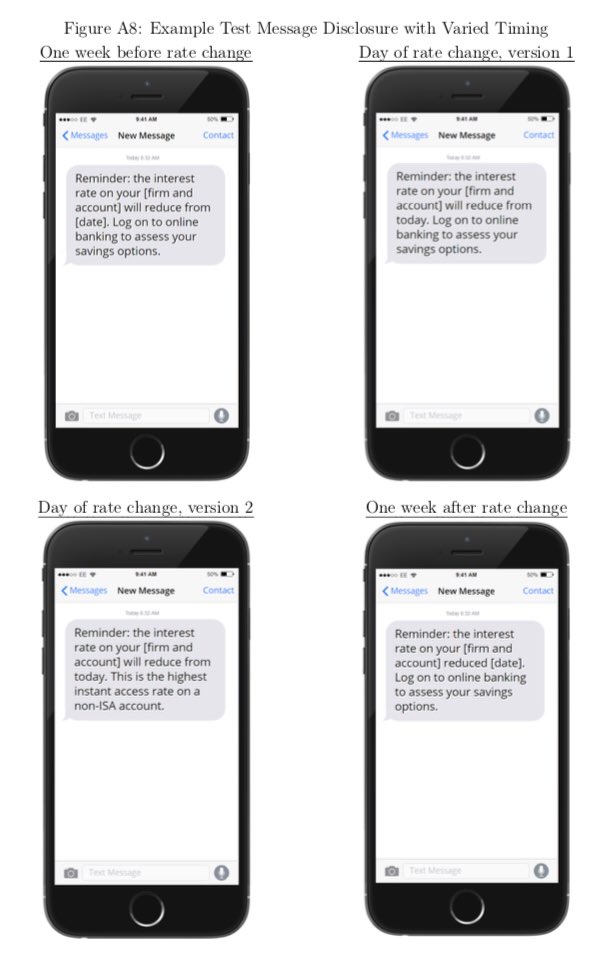

We test disclosures in 5 trials (N=124,000) designed to encourage switching to higher paying accounts. Motivated by the literature we focus on three types of interventions designed to 1. alleviate search frictions, 2. reduce switching costs, and 3. tackle inattention (4/n)

We report on two outcomes: ‘internal switching’, moving to the better account with the same firm. And ‘any switching’, which adds in closing or withdrawing funds. Importantly, in 4 out of 5 trials, there was a strictly better product available *within* the same firm. (5/n)

Despite a potential gain of £123 in the first year, switching rates in the control groups in our field trials were generally low. 8.7% on average but as low as 3% in one firm and as high as 40% in another firm. (6/n)

Looking at the average effect of recieving our disclosures we see modest impacts on switching. Giving account info led to a 2pp increase. Providing a sign-and-return switching form gave a 9pp bump. Reminding people to take action by SMS/email increased it by 4-5pp. (7/n)

Most switching is within their existing firm. We see limited variation between different disclosure designs within each trial. And there are no obvious customer characteristics that respond better or worse to treatment. (8/n)

We conduct a follow up survey to further understand behaviour along three key dimensions - recall and awareness of interest rates, self-reported drivers of switching, and satisfaction with their decision (9/n)

Our research provides direct evidence on the effectiveness of disclosure in facilitating optimal choice in a simple financial product. Our survey suggests sticky deposits are a result of non-price preferences and pessimistic beliefs about the switching process (10/n)

Whilst our treatments had a moderate (3-9pp) impact on behaviour, many people still failed to take action, despite the potential gains and their intention to do so, pointing towards the potential use of stronger interventions (11/n)

Our research directly supported the policy of @TheFCA in improving customer outcomes in the instant access cash savings market (End)

@threadreaderapp unroll