,

14 tweets,

4 min read

Read on Twitter

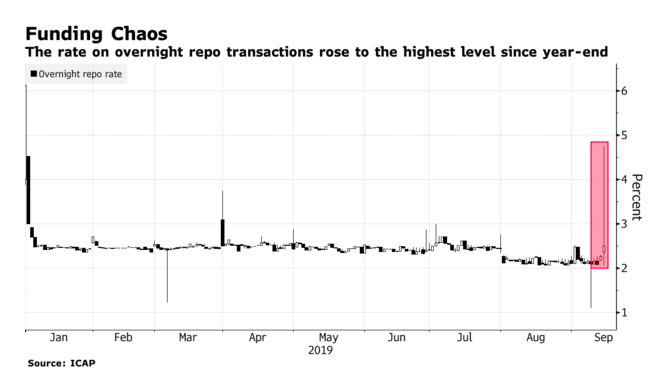

hmm, I am not sure that 'A decade of extraordinary monetary policy experiments has left the system badly distorted' ft.com/content/35d662…

the US repo market before 2008 was a uniqely complex animal. Take the tri-party segment, at the time hosted by the balance sheets of two banks, JP Morgan and Bank of New York Mellon.

shadow banks ran away from Fed's intraday liquidity charges in the mid 1990s - a Volcker attempt to contain the Fed's balance sheet, thanks Milton - into the triparty repo market.

Securities dealers that used triparty repo could avoid Fedwire, as triparty agents moved cash and collateral between dealer accounts. But tri-party repo financing actually only occured overnight.

during the day, dealers needed access to their securities (no practices of collateral substitution like in Europe). So JP Morgan unwound repos in the morning for its clients, and rewound them at night.

throughout the day, it was JP Morgan and BNYMellon that provided unsecured financing. By 2008 this intraday financing increased to USD 2.8 trillion intraday. That is, the triparty repo activity of these two banks equalled in size their entire non-repo balance sheet.

this of it like that - the two clearing banks were a sort of shadow central bank, replacing the Fed in providing intraday liquidity to dealers. And you guessed right, the Fed imposed no capital surcharge on that.

all changed after 2008 - with a Task Force on Tri Party Repo Infrastructure mandated to sort this out asap (see Copeland et al 2012)

the tri party arrangement explains, to my mind, why we had a regime of falling Fed reserves, rapidly expanding securities before 2008

JP Morgan didnt like the reforms and exited the triparty repo in 2016, leaving BNY Mellon the only institution that provides a critical part of the plumbing pionline.com/article/201608…

yet tri-party volumes, particularly of Fedwire eligible securities, picked up after 2016.

in collateral terms, it's not actually Treasuries, but Agency MBS that seems to have picked up in GFC repo, mirroring the overall rise in triparty volumes.

I am yet to see an analysis that connects changes in triparty plumbing to this week's developments. If plumbing was so important before 2008, is it reasonable to assume it's not an issue any more? If you know of one, please share at daniela.gabor at uwe.a.uk

If @NathanTankus is right about how intraday liquidity rules require Fed to support banks' Treasuries positions (think he is), imagine how much fun this will be when it hits @ecb in post QE era