1/ Quality Minus Junk (Asness, Frazzini, Pedersen)

"Higher-quality stocks have higher prices (P/B) on average, but not by a very large margin. A quality-minus-junk (QMJ) factor earns significant risk-adjusted returns in the U.S. and globally."

papers.ssrn.com/sol3/papers.cf…

"Higher-quality stocks have higher prices (P/B) on average, but not by a very large margin. A quality-minus-junk (QMJ) factor earns significant risk-adjusted returns in the U.S. and globally."

papers.ssrn.com/sol3/papers.cf…

2/ AQR hypothesizes that quality stocks (profitable, growing, and safe) deserve higher prices. They construct profitability, growth, and safety factors as well as a combined quality factor in the same fashion as Fama and French.

(Global returns are not currency-hedged.)

(Global returns are not currency-hedged.)

3/ Quality tends to be persistent, with quality stocks tending to remain quality stocks after ten years (with some signal decay but still stat. significant).

Growth suffers the most signal decay, and the short side of each quality style decays more than the long side does.

Growth suffers the most signal decay, and the short side of each quality style decays more than the long side does.

4/ Quality stocks do tend to have higher P/B ratios than junk stocks do, though R² is only 0.10 when quality alone is used to try to explain P/B.

Both the association and low R² hold after controlling for size, stale book values, firm age, profit uncertainty, and dividends.

Both the association and low R² hold after controlling for size, stale book values, firm age, profit uncertainty, and dividends.

5/ The association between quality and P/B also holds across industries and in the broad (global) sample.

6/ Even though quality stocks are expensive, they also have higher returns. The effect increases after controlling for MKT (quality is low beta, partly by construction), SMB and HML (negative correlations), and UMD (low correlation).

So risk may not be the entire story....

So risk may not be the entire story....

7/ Portfolio Visualizer shows the correlations between AQR factors (1/1964 - 8/2019). QMJ has moderately negative correlations to MKT, SMB, and HML-Dev as well as moderately low postive correlations to momentum and BAB (even though BAB is part of QMJ).

8/ The profitability, safety, and growth aspects of quality have 4-factor (MKT, SMB, HML, UMD) alphas that are moderately correlated to each other.

One measure of quality tends to be associated with other measures of quality, but they're also not identical.

One measure of quality tends to be associated with other measures of quality, but they're also not identical.

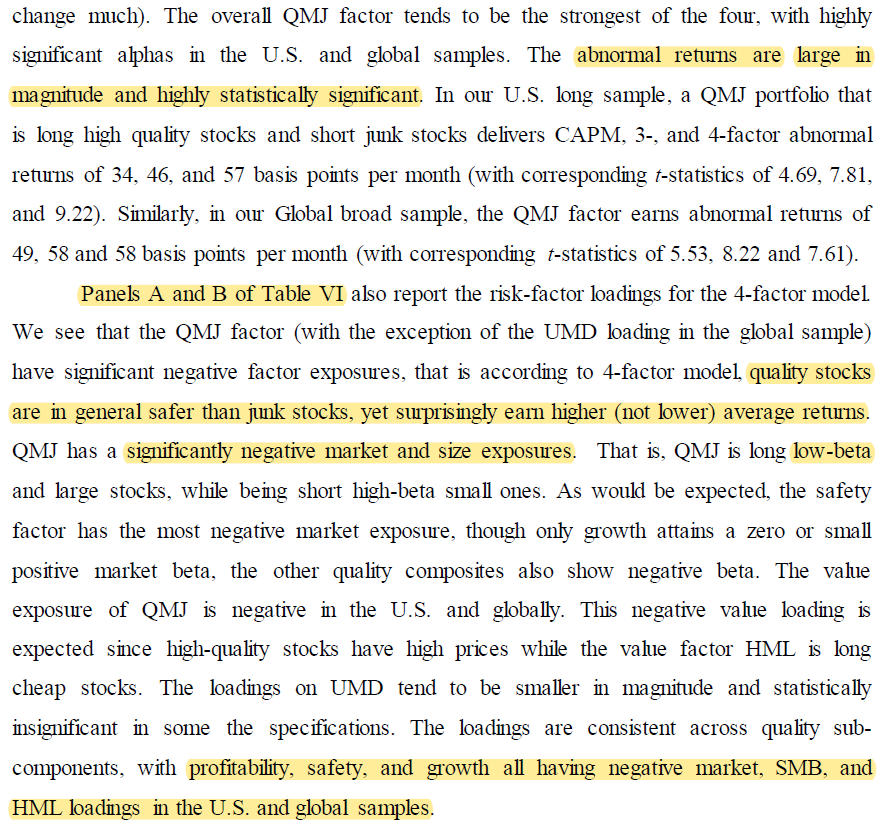

9/ The pattern we've seen previously holds when the profitability, safety, and growth aspects are examined separately. Factor loadings are negative, and alphas increase as we control for more factors.

QMJ's 4-factor alpha is the largest and most statistically significant.

QMJ's 4-factor alpha is the largest and most statistically significant.

10/ The results hold globally and are statistically significant in a surprising number of countries (given the small cross-section of stocks and short period of time used for some of these markets).

The 4-factor adjusted information ratio is 1.29 in the U.S. and 1.60 globally.

The 4-factor adjusted information ratio is 1.29 in the U.S. and 1.60 globally.

11/ "The QMJ factor has consistently delivered positive excess returns and risk-adjusted returns over time with no particular subsample driving our results."

12/ The results survive the inclusion of CMA and RMW.

"QMJ portfolios have a large loading on the RMW factor based on gross profits over assets (GPOA), which is not surprising given that GPOA is a component in our profitability composite."

"QMJ portfolios have a large loading on the RMW factor based on gross profits over assets (GPOA), which is not surprising given that GPOA is a component in our profitability composite."

13/ Quality seems to work about as well in large stocks as in small ones.

The negative loading on HML only shows up in the large, high-quality bucket, and controlling for this raises alphas considerably.

These results hold in the broad (global) sample as well.

The negative loading on HML only shows up in the large, high-quality bucket, and controlling for this raises alphas considerably.

These results hold in the broad (global) sample as well.

14/ Although BAB is a component of QMJ's "safety" composite, the results hold for QMJ, profitability, safety, and growth after controlling for BAB.

The 4-factor adjusted information ratio is also somewhat consistent across industries, both in the U.S. and globally.

The 4-factor adjusted information ratio is also somewhat consistent across industries, both in the U.S. and globally.

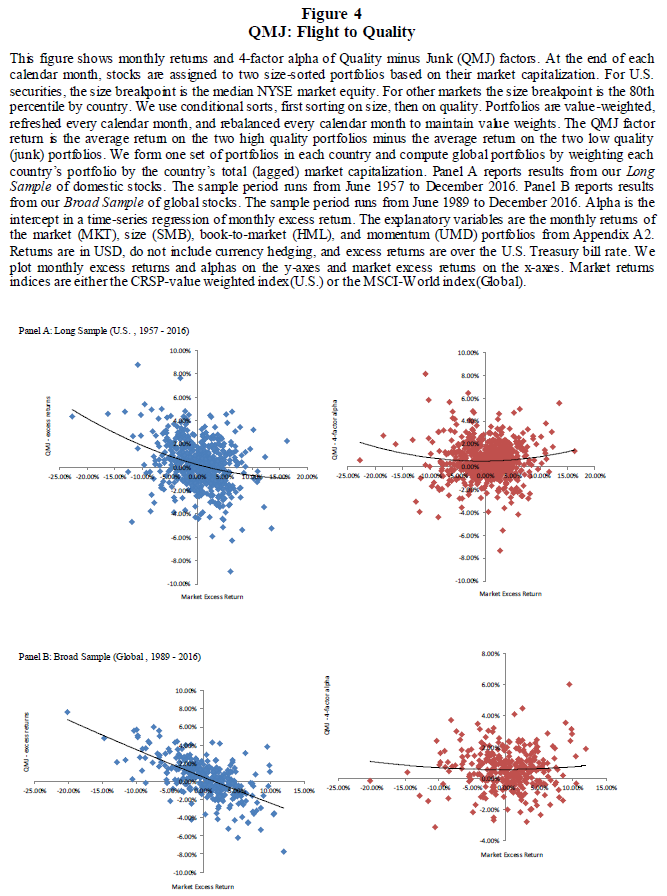

15/ The return to quality doesn't seem to be a compensation for tail risk. Four-factor alphas are positive and mostly statistically significant in all of the regimes AQR identified.

The returns and alphas even have a mild (though not stat. significant) convexity wrt mkt returns.

The returns and alphas even have a mild (though not stat. significant) convexity wrt mkt returns.

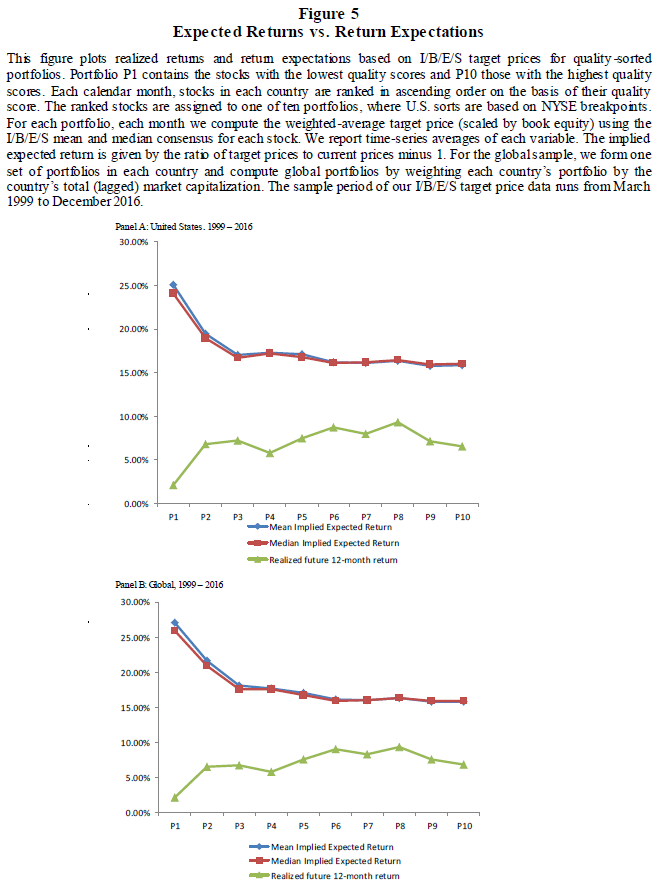

16/ Analysts' expectations tend to be too high, but the problem is worse for low-quality stocks.

They expect quality to perform worse than junk, but the opposite tends to be true going forward.

This is highly statistically significant, both in the U.S. and globally.

They expect quality to perform worse than junk, but the opposite tends to be true going forward.

This is highly statistically significant, both in the U.S. and globally.

17/ This tends to be true for factors in general and not just QMJ.

Analysts are on the wrong side of most factors. Large forecast errors are associated with very high factor returns during earnings events.

Analysts are on the wrong side of most factors. Large forecast errors are associated with very high factor returns during earnings events.

18/ The relationship between quality and P/B varies over time. Quality was cheap in early 2000 during the Internet bubble and expensive in 2002 and 2009, after the last two bear markets.

19/ "A high price of quality indeed predicts lower returns on QMJ.

"Predictability rises with the forecasting horizon, indicating slowly changing expected returns."

"Predictability rises with the forecasting horizon, indicating slowly changing expected returns."

20/ AQR ranks on both quality and P/B to generate "quality at a reasonable price" (QARP).

"The Sharpe ratio of QARP is naturally higher than either quality or value alone... it helps investors avoid the "value trap," buying securities that look cheap but deserve to be cheap."

"The Sharpe ratio of QARP is naturally higher than either quality or value alone... it helps investors avoid the "value trap," buying securities that look cheap but deserve to be cheap."

21/ Here's the obligatory Buffett reference:

22/ Controlling for QMJ makes the alphas for both SMB and HML statistically significant, even when CMA and RMW are included.

RMW is a component of QMJ, and its alpha is no longer statistically significant in QMJ's presence.

RMW is a component of QMJ, and its alpha is no longer statistically significant in QMJ's presence.

23/ Here are the variable definitions for QMJ. Have fun!