1/ Global Factor Premiums (Guido Baltussen, Laurens Swinkels, Pim van Vliet)

"New sample evidence reveals that the large majority of global factors are strongly present under conservative p-hacking perspectives, with limited out-of-sample decay."

papers.ssrn.com/sol3/papers.cf…

"New sample evidence reveals that the large majority of global factors are strongly present under conservative p-hacking perspectives, with limited out-of-sample decay."

papers.ssrn.com/sol3/papers.cf…

2/ "One does not have to be extremely skeptical to disregard the empirical evidence provided in the literature. Further analysis is warranted using new and independent data.

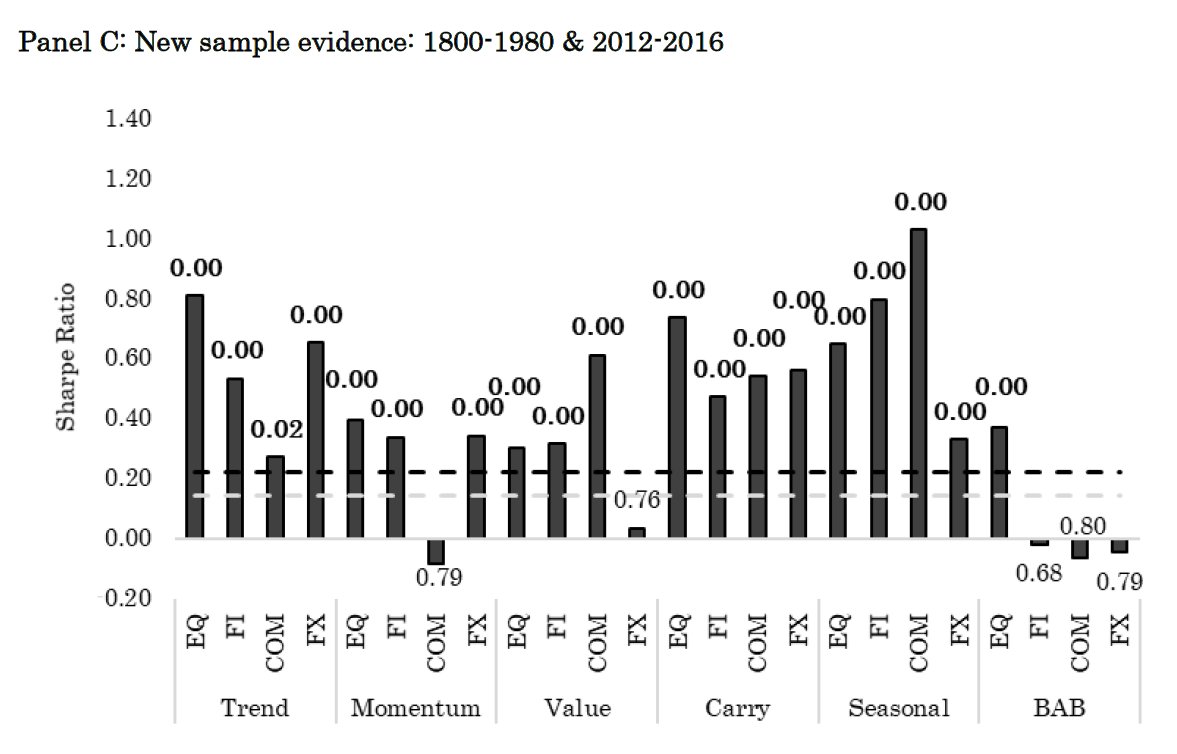

"We construct a deep, largely uncovered historical global database spanning the period 1800-1980."

"We construct a deep, largely uncovered historical global database spanning the period 1800-1980."

3/ "We replicate the original studies in a unified testing framework in which we limit the degrees of freedom (uniform sample period, cross-section of assets, and factor construction method: rank-weighting, vol scaling).

"SRs are marginally lower than in the original studies."

"SRs are marginally lower than in the original studies."

4/ "Trend" = 12-month TS momentum, skipping most recent month

"Momentum" = XS using 12-month excess returns, skipping most recent month

Also: value, carry, monthly seasonality, and BAB (relative to global asset class portfolio return)

No individual stocks (asset classes only)

"Momentum" = XS using 12-month excess returns, skipping most recent month

Also: value, carry, monthly seasonality, and BAB (relative to global asset class portfolio return)

No individual stocks (asset classes only)

5/ "One does not need to be very skeptical to disregard the (in-sample) empirical evidence. This leaves us to conclude that further analysis is warranted using new and independent data."

6/ "Our sample covers 217 years of data from 31 Dec 1799 to 31 Dec 2016."

Asset classes include global equity indices, global bonds, commodities, and FX. The start dates is different for each index used; not all of the series are 200 years old.

Asset classes include global equity indices, global bonds, commodities, and FX. The start dates is different for each index used; not all of the series are 200 years old.

7/ The number of markets shrinks as we move backward in time, which should lead to less diversification and more noise (potentially biasing the results toward the null hypothesis).

The authors filter out hyperinflation (ex-ante), low liquidity, and smaller markets.

The authors filter out hyperinflation (ex-ante), low liquidity, and smaller markets.

8/ "We find a strong presence of most global return factors... very limited out-of-sample decay. In fact, the average Sharpe ratio of our replication exercise is also [the same] 0.41."

"Time-seires momentum, carry, and seasonality are generally the strongest."

"Time-seires momentum, carry, and seasonality are generally the strongest."

9/ "One needs to be extremely skeptical in order not to reject the null hypothesis that global factor returns are zero.

"This study does not examine smarter and possibly better definitions, nor aspects linked to (limits to) arbitrage and tradeability."

"This study does not examine smarter and possibly better definitions, nor aspects linked to (limits to) arbitrage and tradeability."

10/ "With the exception of BAB, the multi-asset combinations have a positive Sharpe ratio in at least 90% of the rolling 10-year periods between 1800 and 2016. This consistency of performance over time further strengthens our empirical evidence."

11/ The results are robust to

* removing the liquidity screen

* using top-bottom terciles instead of rank-weighting

* using simple equal-weighting rather than volatility scaling

* lagging the signals by an additional month

* rebalancing less often

* trimming extreme returns

* removing the liquidity screen

* using top-bottom terciles instead of rank-weighting

* using simple equal-weighting rather than volatility scaling

* lagging the signals by an additional month

* rebalancing less often

* trimming extreme returns

12/ Alphas are positive and highly stat. significant.

Correlations of (1) each factor to the same factor in other asset classes and (2) factors to other factors in the same asset class are close to zero.

In spanning tests, trend subsumes XS momentum; BAB doesn't survive.

Correlations of (1) each factor to the same factor in other asset classes and (2) factors to other factors in the same asset class are close to zero.

In spanning tests, trend subsumes XS momentum; BAB doesn't survive.

13/ "Downside beta is very similar to the regular beta.

"The price of beta is of the wrong sign and insignificant, as also evident from the flat line in Figure 3.

"Downside market risk does not materially explain the global factor premiums."

"The price of beta is of the wrong sign and insignificant, as also evident from the flat line in Figure 3.

"Downside market risk does not materially explain the global factor premiums."

14/ "Most global return factors do not display stronger returns during bad states (e.e. recessions, crises, turbulence).

"The most notable exception is value in equities during recession periods or bear markets, but these findings do not persist in crisis periods."

"The most notable exception is value in equities during recession periods or bear markets, but these findings do not persist in crisis periods."

15/ "The global return factors have intercepts that are highly significant and are of similar magnitude to the raw returns over this sample. These results suggest that macroeconomic risks have very limited explanatory power for the global factor returns."

16/ Ilmanen, Israel, Moskowitz, Thapar, and Wang run similar tests under different conditions. They find some evidence of data mining but not of arbitrage.

(Results differ for low-beta "defensive" they estimate betas using *local* market indices.)

(Results differ for low-beta "defensive" they estimate betas using *local* market indices.)