1/ Risk Premia and the VIX Term Structure (Johnson)

"A single principal component, Slope, predicts the excess returns of S&P 500 variance swaps, VIX futures, and S&P 500 straddles for all maturities to the exclusion of the rest of the term structure."

papers.ssrn.com/sol3/papers.cf…

"A single principal component, Slope, predicts the excess returns of S&P 500 variance swaps, VIX futures, and S&P 500 straddles for all maturities to the exclusion of the rest of the term structure."

papers.ssrn.com/sol3/papers.cf…

2/ 1st PC = "Level"

2nd PC = "Slope"

"It is possible for Slope to be positive [in contango] on a day in which the VIX term structure is strictly decreasing [in backwardation]. For this reason, my analyses compare high Slope to low Slope periods, making average Slope irrelevant."

2nd PC = "Slope"

"It is possible for Slope to be positive [in contango] on a day in which the VIX term structure is strictly decreasing [in backwardation]. For this reason, my analyses compare high Slope to low Slope periods, making average Slope irrelevant."

3/ "Longer-maturity variance assets [and those with larger β to ΔVIX] have less negative Sharpe ratios.

"Results make it unlikely that the conditional risk premia of all 18 test assets are related in the same direction to a single factor. However, I show that this is the case."

"Results make it unlikely that the conditional risk premia of all 18 test assets are related in the same direction to a single factor. However, I show that this is the case."

4/ "The VIX term structure does *not* reliably increase (decrease) after the term structure is upward (downward) sloping. To the extent that it does, the term structure contains no information other than simple mean reversion already captured by current VIX."

5/ "All time-series variation in variance risk premia come from variations in Slope, while all cross-sectional differences in variance risk premia come from the constant factor loading [on Slope] and the intercept."

6/ "Slope negatively predicts variance asset returns [33/36 statistically significant]. No other PC predicts returns with such consistency.

"The failure of the Level factor is particularly surprising: most models predict variance risk premia to be larger in high variance times."

"The failure of the Level factor is particularly surprising: most models predict variance risk premia to be larger in high variance times."

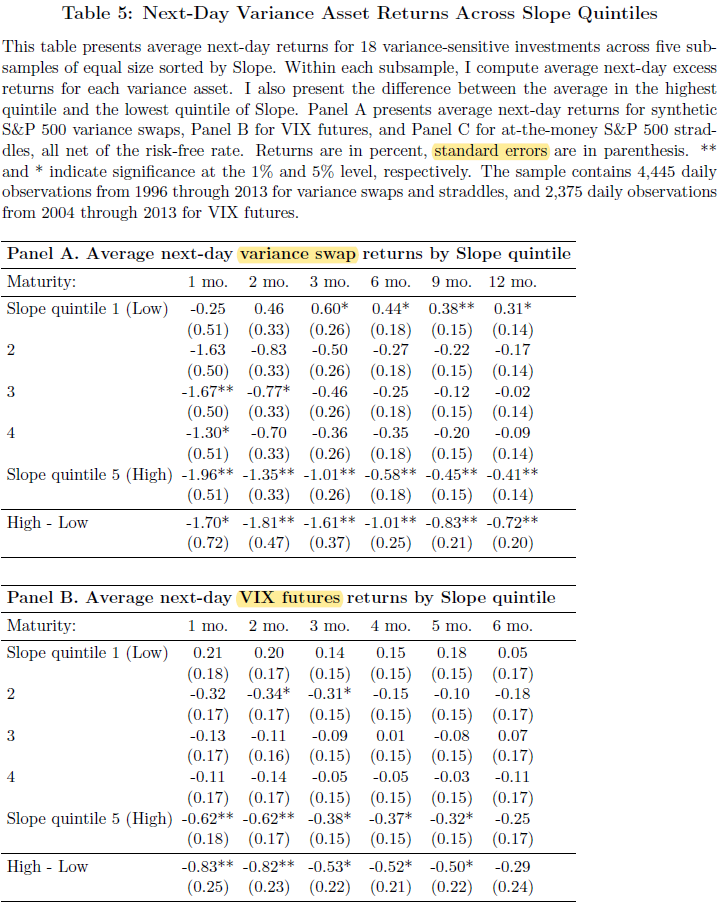

7/ "The difference between high and low Slope quintiles is statistically significant for all but the 6-month VIX futures returns and economically enormous/

"The relationship appears to be non-linear (much stronger in quintile 1, for which average returns increase dramatically)."

"The relationship appears to be non-linear (much stronger in quintile 1, for which average returns increase dramatically)."

8/ "The exogenous slope definition is likely less effective because it is -68% correlated with Level, which is unrelated to variance asset returns. The neg. correlation is due to mean reversion in volatility, which makes the term structure [backwardated] when its level is high."

9/ "If anything, future variance risk asset returns are higher following market crashes, indicating that the magnitude of variance risk premia actually decreases.

"VIX² is an insignificant or incrementally *positive* predictor of variance asset returns."

"VIX² is an insignificant or incrementally *positive* predictor of variance asset returns."

10/ "Conditional S&P 500 skew [as well as Dealer Leverage] do not predict future variance asset returns incremental to the other indicators.

"The predictability is robust to winsorizing Slope, using quintiles of Slope, and using alternate geometric definitions of slope."

"The predictability is robust to winsorizing Slope, using quintiles of Slope, and using alternate geometric definitions of slope."

11/ Carry (the failure of the expectations hypothesis) generalizes to other markets, including equities, bonds, commodities, Treasuries, and credit.

Jim Campasano outlines a simple strategy for trading the VIX term structure here:

Jim Campasano outlines a simple strategy for trading the VIX term structure here: