,

9 tweets,

4 min read

Read on Twitter

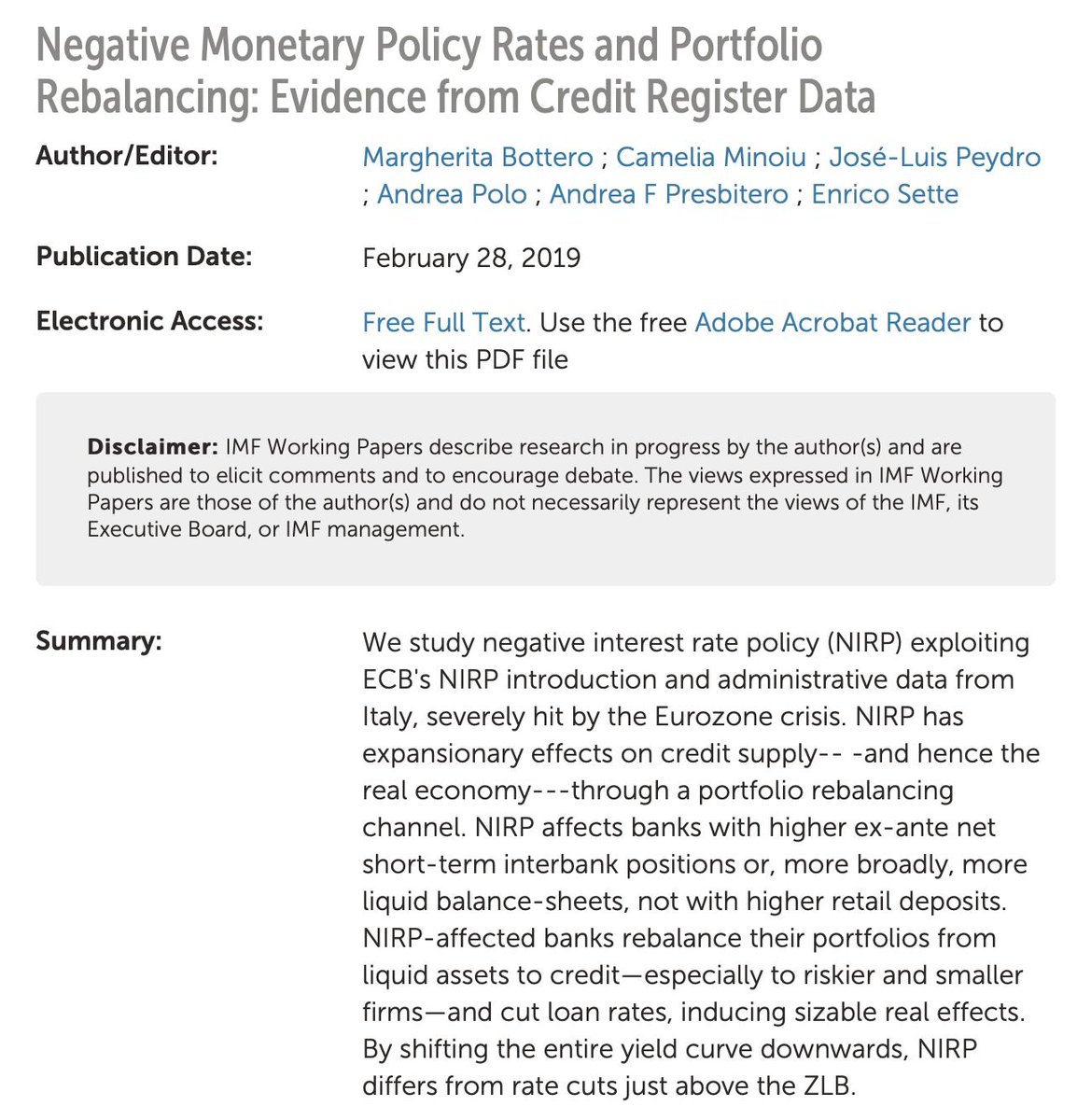

Now out as an @IMFNews working paper: new evidence on the effect of negative policy rates on bank credit supply using loan-level data.

Short thread to outline our main findings 1/9

imf.org/en/Publication…

Short thread to outline our main findings 1/9

imf.org/en/Publication…

A cut in policy rates expands aggregate demand, but:

1. in a low rates environment, the transmission of monetary policy becomes weaker

2. the ZLB is an important constraint (@krogoff)

3. beyond a “reversal” rate, lower rates could be contractionary (@MarkusEconomist) 2/9

1. in a low rates environment, the transmission of monetary policy becomes weaker

2. the ZLB is an important constraint (@krogoff)

3. beyond a “reversal” rate, lower rates could be contractionary (@MarkusEconomist) 2/9

So we ask 3 main research questions:

1. How does negative interest rate policy (NIRP) affect credit supply and the real

economy?

2. Through which channel does NIRP operate?

3. How does NIRP differ from other conventional and unconventional policies? 3/9

1. How does negative interest rate policy (NIRP) affect credit supply and the real

economy?

2. Through which channel does NIRP operate?

3. How does NIRP differ from other conventional and unconventional policies? 3/9

We study the transmission of NIRP to the economy via the banking system exploiting:

1. the ECB’s introduction of NIRP in June 2014

2. the Italian credit register matched with firm- and bank-level balance sheets 4/9

1. the ECB’s introduction of NIRP in June 2014

2. the Italian credit register matched with firm- and bank-level balance sheets 4/9

NIRP can affect credit through 2 main channels:

Retail deposits channel: as banks are reluctant to pass negative rates to depositors, NIRP may reduce banks profits and erode capital. Thus, NIRP could lead to risk-taking & lower lending (@gschepen @GautiEggertsson @LHSummers) 5/9

Retail deposits channel: as banks are reluctant to pass negative rates to depositors, NIRP may reduce banks profits and erode capital. Thus, NIRP could lead to risk-taking & lower lending (@gschepen @GautiEggertsson @LHSummers) 5/9

Portfolio rebalancing channel: by shifting the yield curve downward, NIRP could create a wedge between safer, liquid & riskier assets, incentivizing banks to rebalance their portfolio from low/negative-yield liquid assets towards higher-yield assets, such as corporate loans 6/9

We use loan-level data on almost 170,000 firms to compare the change in credit before and after NIRP to the same firm in the same period by banks with different exposure to the policy. Firm fixed effects absorb unobserved firm-specific shocks (e.g. credit demand) 7/9

We show that banks with ex-ante more liquidity:

1. Reduce their net holdings of liquid assets

2. Expand credit supply, especially to ex-ante riskier firms (with no higher ex-post NPLs)

3. Reduce lending rates

4. There are real effects on firm activities 8/9

1. Reduce their net holdings of liquid assets

2. Expand credit supply, especially to ex-ante riskier firms (with no higher ex-post NPLs)

3. Reduce lending rates

4. There are real effects on firm activities 8/9

NIRP has expansionary effects on credit & the economy through a portfolio rebalancing channel.

Unlike previous cuts just above the ZLB and forward guidance, this channel was activated as NIRP shifted downward and flattened the yield curve. We find similar results for QE

9/9

Unlike previous cuts just above the ZLB and forward guidance, this channel was activated as NIRP shifted downward and flattened the yield curve. We find similar results for QE

9/9