,

36 tweets,

12 min read

Read on Twitter

It's probably the world's most controversial coal mine, but the sums just don't add up.

Here's my breakdown, with links to sources, of why Adani's Carmichael pit doesn't make sense: (thread)

bloomberg.com/opinion/articl…

Here's my breakdown, with links to sources, of why Adani's Carmichael pit doesn't make sense: (thread)

bloomberg.com/opinion/articl…

I wasn't actually planning to write a piece on this, as I'd written on it several years ago (here: bloomberg.com/opinion/articl… ) and the numbers haven't really changed.

But I started tweeting out some back-of-the-envelope calculations while I was waiting for my 8yo to fall asleep on Wednesday night and it blew up a bit.

I don't have a Soundcloud to promote so the best thing I can do is write an article! 😀

I don't have a Soundcloud to promote so the best thing I can do is write an article! 😀

The numbers are with some minor modifications the same as my off-the-top-of-head figures on Wednesday. I asked Adani for comment. They provided a general denial but declined to provide alternative figures or any specifics about why they think these are wrong. Response in full:

If people want to play around with these assumptions to reach their own conclusions I made a very rough model on Google Sheets: docs.google.com/spreadsheets/d…

You can download and change the orange cells to input your own assumptions.

You can download and change the orange cells to input your own assumptions.

I want to just talk about two things quickly I didn't mention much in the previous thread and the article. One is the issue of self-financing.

Adani have promised they'll fund it off their own balance sheet, but it's quite hard to see how this is possible.

Adani have promised they'll fund it off their own balance sheet, but it's quite hard to see how this is possible.

Adani Group has four main listed companies. These are collectively fairly deep in debt. As a very general rule of thumb you want net debt of no more than 3.5x Ebitda, but only Adani Ports & SEZ achieves this (to be fair, the rules are often looser on utilities and infrastructure)

More to the point, look at interest cover. You'd prefer to have this *above* 3.5 and below 1.5 things get very scary. Below 1 you are spending more on interest than you're making in operating income, which is very dangerous if you can't turn it round.

There's also lots of unlisted entities in the Adani Group so maybe there's somewhere that Adani can rustle up $2bn. But it's hard to see how -- the balance sheet isn't a magic pudding. Really they should be rebuilding group balance sheets rather than taking on yet more debt.

Given the state of the Indian banking sector -- for an introduction, read my colleague @andymukherjee70 here: bloomberg.com/opinion/articl… -- I would never say never to a state bank making an uncommercial loan to a well-connected billionaire. But a normal bank wouldn't.

@andymukherjee70 Second point is about what happens to this coal when it gets to India.

If you look at the bottom of that Google Sheet you'll see some rough calculations for the cost of coal per megawatt hour, based on the assumptions at the top about mining costs etc.

If you look at the bottom of that Google Sheet you'll see some rough calculations for the cost of coal per megawatt hour, based on the assumptions at the top about mining costs etc.

@andymukherjee70 My estimate of that is that the *fuel cost* alone for coal comes to about $42/MWh. On top of that, of course, a generator has general operating and maintenance costs plus its own depreciation, interest etc costs to deal with.

This, again, just doesn't stack up.

This, again, just doesn't stack up.

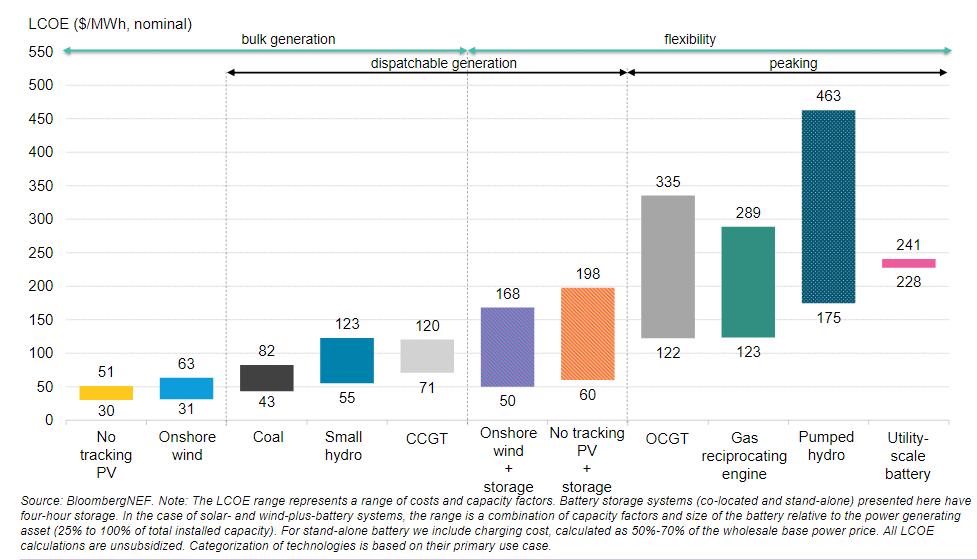

@andymukherjee70 Look at @BloombergNEF estimates of the costs of building new generation in India. Majority of solar and wind projects are cheaper. Even with battery back-up to provide dispatchable power, the low end of renewables costs would undercut *existing* thermal burning coal at this price

@andymukherjee70 @BloombergNEF (important energy-nerd point: It's one thing for new projects to be cheaper, as wind and solar is vs. coal now in most places. It's a whole other, and much more dramatic, thing for new projects to undercut *existing* depreciated plants)

@andymukherjee70 @BloombergNEF I find it hard to believe that Adani, who are quite a big solar developer, are ignorant of the way these costs are changing.

I want to end with, actually, a small *defence* of Adani here. The Carmichael coal project is not a very big one and attracts attention, from both sides, *vastly* out of proportion to its significance. 10mtpa projects get up in Australia all the time.

If you're not a miner or an anti-coal campaigner you have probably never heard of Mount Pleasant machenergyaustralia.com.au or Vickery vickery.com.au but these are Carmichael-scale projects that are quietly going ahead with little fanfare or talk of public funding.

To put this in context, a ton of coal produces about 2.5 tons of CO2-equivalent.

Carmichael stage 1 would be ~25mt CO2e, stage 2 ~70mt CO2e.

Australia's coal and LNG exports total 1,200mt CO2e, and domestic emissions are 600mt CO2e. Read more here:

bloomberg.com/opinion/articl…

Carmichael stage 1 would be ~25mt CO2e, stage 2 ~70mt CO2e.

Australia's coal and LNG exports total 1,200mt CO2e, and domestic emissions are 600mt CO2e. Read more here:

bloomberg.com/opinion/articl…

As I say in the article, I *think* Carmichael is such a flashpoint because it's not seen as just a mine but as the wedge to open up the entire Galilee Basin, where the ~215mtpa of possible coal projects would add up to 500mt CO2e:

bloomberg.com/opinion/articl…

bloomberg.com/opinion/articl…

Oddly enough, the *coal mining industry* is in some ways as worried about this prospect as environmentalists. Glencore cancelled its Wandoan project, which is quite Carmichael-like, back in 2013 and worries that extra tonnages will flood the market.

melbourneminingclub.com/wp-content/upl…

melbourneminingclub.com/wp-content/upl…

It's very telling that despite masses of coal mining investment going on when the Galilee was put out to tender in 2010, *not a single major listed miner* put in a tenement bid.

It was all Adani, Gina Rinehart, Clive Palmer, GVK, and other random investors.

It was all Adani, Gina Rinehart, Clive Palmer, GVK, and other random investors.

Adani and GVK are sophisticated companies but *none of them* could have been described as sophisticated miners at the time (Gina Rinehart is now with Roy Hill, but wasn't then)

The mining industry knows this doesn't stack up.

We saw just this week that one of the projects close to Carmichael has been put on hold.

theguardian.com/environment/20…

BHP on Wednesday said coal power may be "phased out, potentially sooner than expected": bloomberg.com/news/articles/…

We saw just this week that one of the projects close to Carmichael has been put on hold.

theguardian.com/environment/20…

BHP on Wednesday said coal power may be "phased out, potentially sooner than expected": bloomberg.com/news/articles/…

Glencore, the biggest player in Australia and in export-traded coal globally, in February said it would cap its output for the foreseeable future: bloomberg.com/opinion/articl…

Above all you can look at investment numbers for the industry generally. More coal power plants were decommissioned last year than given the go-ahead for investment: bloomberg.com/opinion/articl…

Some mines will still get approved to make up for production declines elsewhere -- many individual mines will lose production, at least at first, quicker than coal generators close.

But this is a dying industry and it can't support whole new coal basins going into production.

But this is a dying industry and it can't support whole new coal basins going into production.

The reason I wrote this is that this fact -- basically an open secret in financial and mining circles -- seems to be almost entirely absent from the public debate in Australia (ends)

BTW a few people have said: "So approve the mine!" I don't disagree. As long as it's not asking for a publicly-funded handout I'm fine with Adani trying to fund this project on its own merits.

For what it's worth, while Adani blame the Queensland government for obstructing them, the Queensland government say Adani keep dragging their feet on doing the paperwork. As to who is right on that, ¯\_(ツ)_/¯

There is a legal process, though, that new mining and infrastructure projects have to go through. I can believe that this has been unusually arduous for Adani given the attention, but it's (rightly) tough everywhere and you don't see Whitehaven and MACH Energy sooking about it.

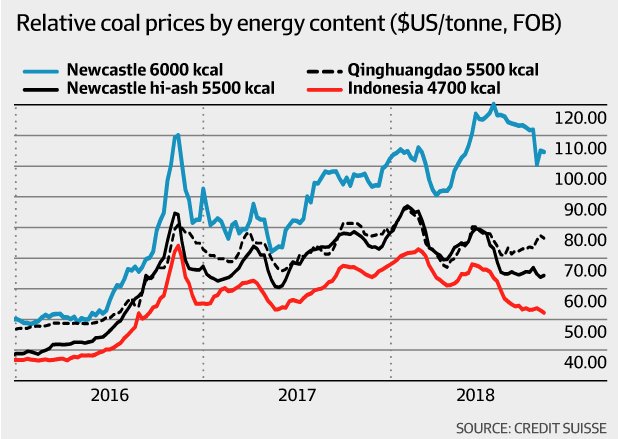

One last thing. This is a chart of 5500kcal thermal export coal at Newcastle over the past six years. You'll see that the highest price it ever achieved was a brief spike to $90/ton in *one week* in early 2018.

Play around with that Google Sheets model docs.google.com/spreadsheets/d… and you'll see that Carmichael needs to get $90/ton to break even, ie. it needs to achieve that *every single week of its mine life*

And this is the price for 5500kcal product. Adani won't be pinned down on their product quality but the numbers they've put out indicate the whole resource is 5000kcal, which gets more like $66/ton: bloomberg.com/opinion/articl…

The *upper end* of the range given by Adani's CEO in a Queensland public inquiry was 5600kcal (4800kcal was the lower end). He point-blank refused to give an average figure.

This is telling because mining projects -- especially those having trouble raising finance, or facing public opposition, or looking for public funds -- usually give out fairly detailed numbers about their assumptions so that third parties can do valuation models.

Adani have never done that, and are extremely difficult to pin down on what numbers they're using. In my view, that's a tell.