1/ Cross-Sectional and Time-Series Tests of Return Predictability: What Is the Difference? (Goyal, Jegadeesh)

"The difference between the performances of TS and CS strategies is largely due to a time-varying net-long investment in risky assets."

papers.ssrn.com/sol3/papers.cf…

"The difference between the performances of TS and CS strategies is largely due to a time-varying net-long investment in risky assets."

papers.ssrn.com/sol3/papers.cf…

2/ The authors first replicate others' results with respect to the performance of time-series (TS) and cross-sectional (CS) momentum in individual stocks.

As expected, CS has reversals for formation periods of one month and 3-5 years. TS can be held for longer (no reversals).

As expected, CS has reversals for formation periods of one month and 3-5 years. TS can be held for longer (no reversals).

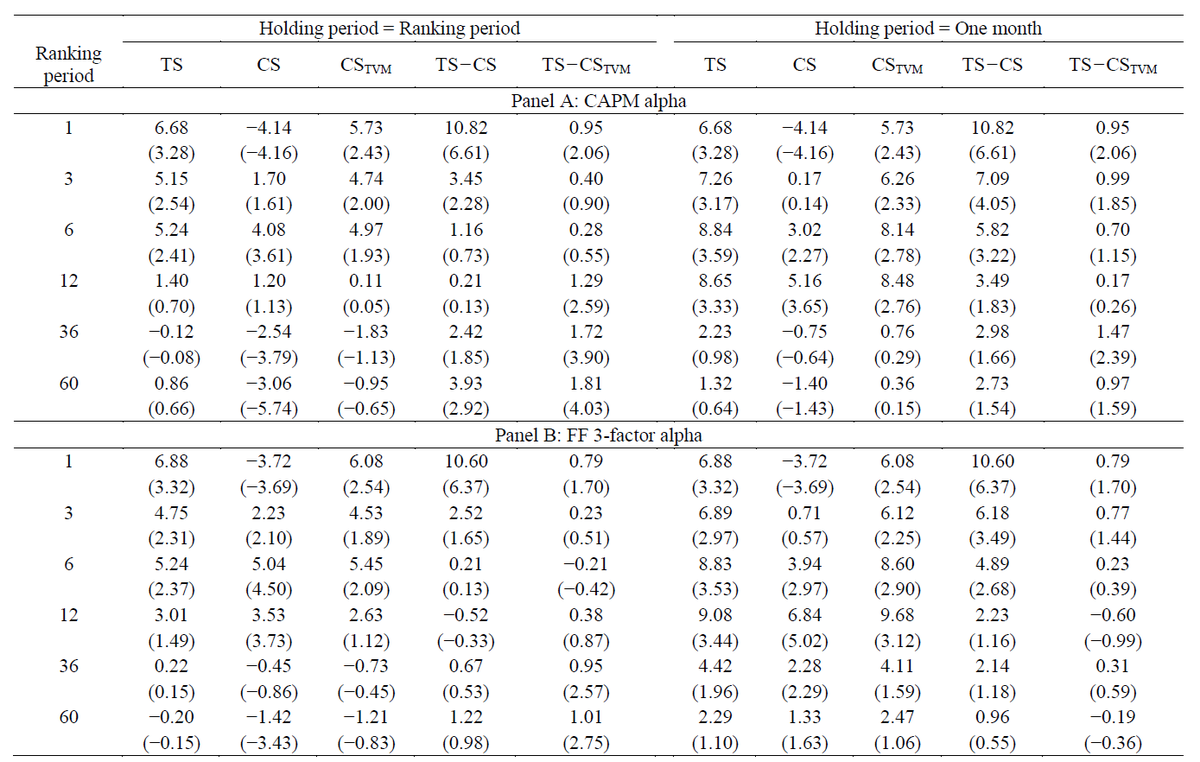

3/ As expected. TS has alpha after controlling for CS but not vice versa. This effect is most pronounced for short (one month) and long (3 and 5 year) ranking periods, resulting in a U-shape if alpha is plotted vs. ranking period.

4/ However, TS can be net long, while CS is market-neutral. The longer the ranking period, the more TS is net long.

The authors construct a CSTVM strategy that adds a time-varying exposure to the market based on the net long position of TS. TS and CSTVM perform similarly.

The authors construct a CSTVM strategy that adds a time-varying exposure to the market based on the net long position of TS. TS and CSTVM perform similarly.

5/ This also holds if TS is built in a market-neutral way ("TS0"). Short-term and long-term reversals show up. TS0 and CS behave in similar ways.

TS0 has more focused exposure to losers (because the median decile is set at the risk-free rate rather than stocks' mean return.)

TS0 has more focused exposure to losers (because the median decile is set at the risk-free rate rather than stocks' mean return.)

6/ TS CAPM and 3-factor alphas are still slightly larger than for CSTVM, but the differences are mostly no longer statistically significant.

CS has negative alphas for one-month and 60-month ranking periods, reflecting the presence of short- and long-term reversals.

CS has negative alphas for one-month and 60-month ranking periods, reflecting the presence of short- and long-term reversals.

7/ The TS and CS strategies seem to be similar except for the number of stocks on the long and short sides.

Because stock returns are positively skewed and because CS goes long (short) stocks above (below) the mean return, CS has more stocks on the short side than the long side.

Because stock returns are positively skewed and because CS goes long (short) stocks above (below) the mean return, CS has more stocks on the short side than the long side.

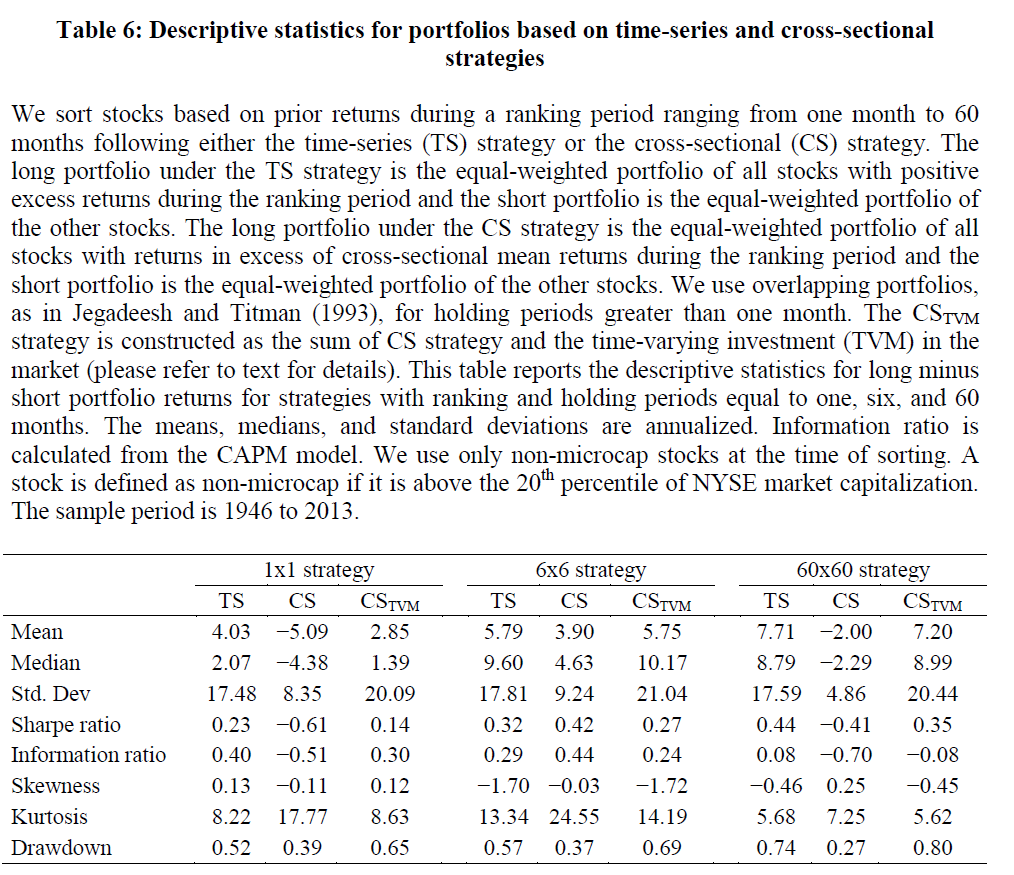

8/ With respect to Sharpe and information ratios, skewness, kurtosis, and drawdown, TS performs similarly to (and perhaps slightly better than) CSTVM.

Given momentum's tendency to crash it's puzzling that the authors didn't find a large drawdown for 6x6 CS.

Given momentum's tendency to crash it's puzzling that the authors didn't find a large drawdown for 6x6 CS.

9/ CS tends to have short-and long-term reversals (previous table), which may be a good strategy to trade in concert with either TS or CSTVM.

This is consistent with short-term reversals being an intra-industry effect, not a broad stock market effect.

This is consistent with short-term reversals being an intra-industry effect, not a broad stock market effect.

10/ Given that TS and CSTVM have a time-varying net long market exposure, what explains their outperformance?

For the one-month ranking period, most of the outperformance comes from market timing. For long ranking periods, all of the benefit comes from being net long the market.

For the one-month ranking period, most of the outperformance comes from market timing. For long ranking periods, all of the benefit comes from being net long the market.

11/ For the 1x1 strategy, the source of the market timing return is likely the serial correlation of market returns (0.14).

(This idea has been explored more generally for asset class - for example, here: )

(This idea has been explored more generally for asset class - for example, here: )

12/ TVM, the time-varying component of TS and CSTVM, doesn't seem to be explained by macro variables.

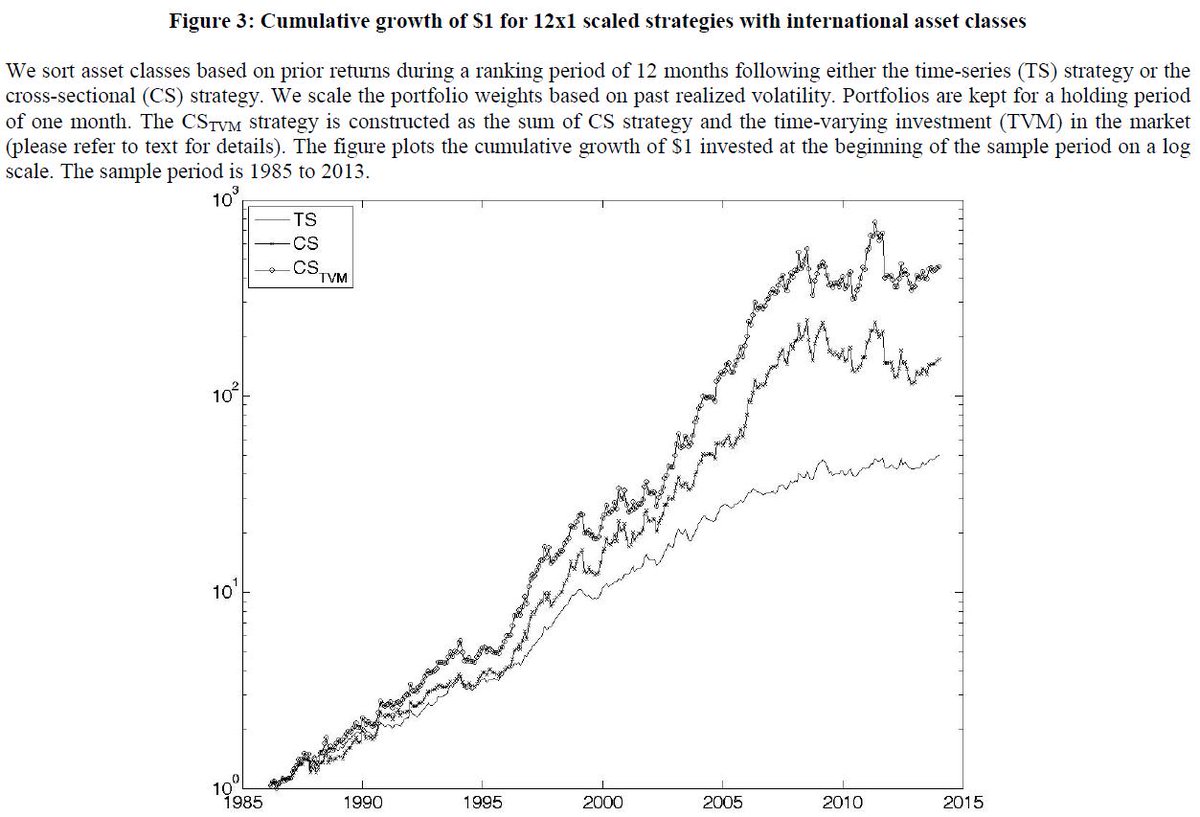

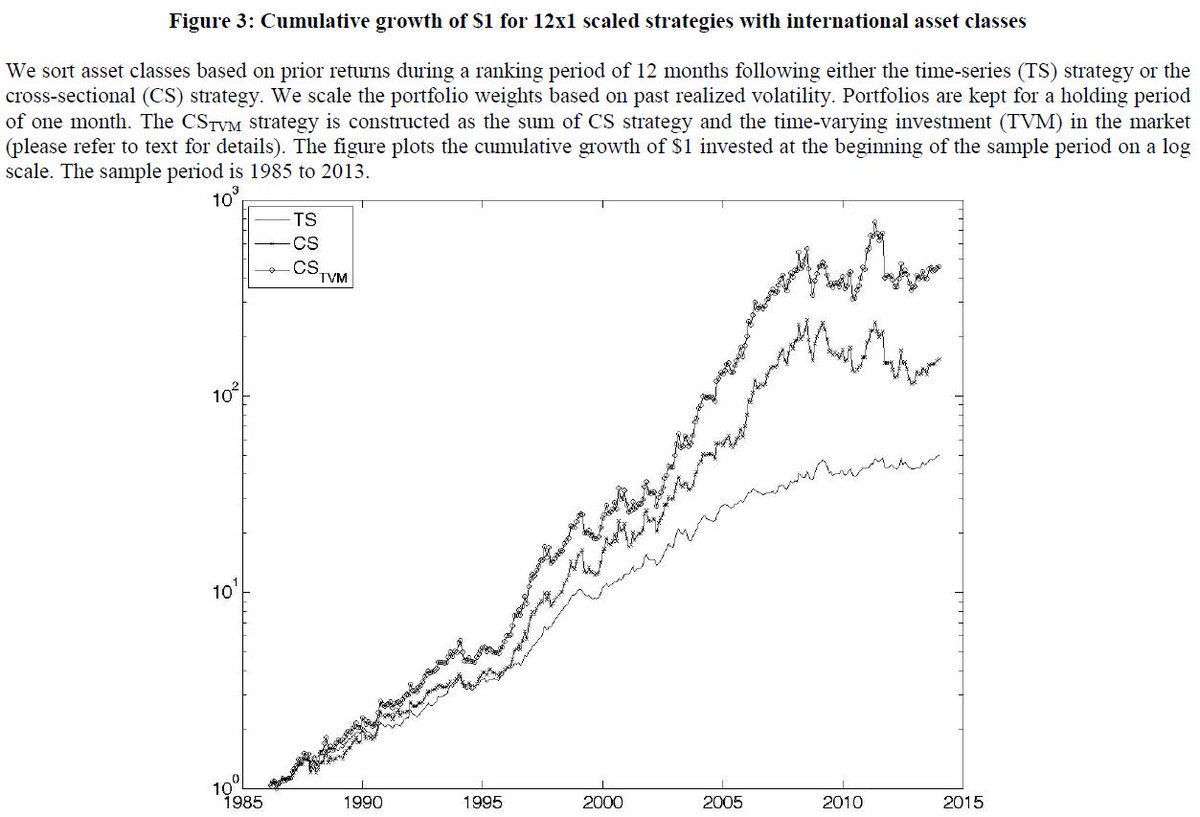

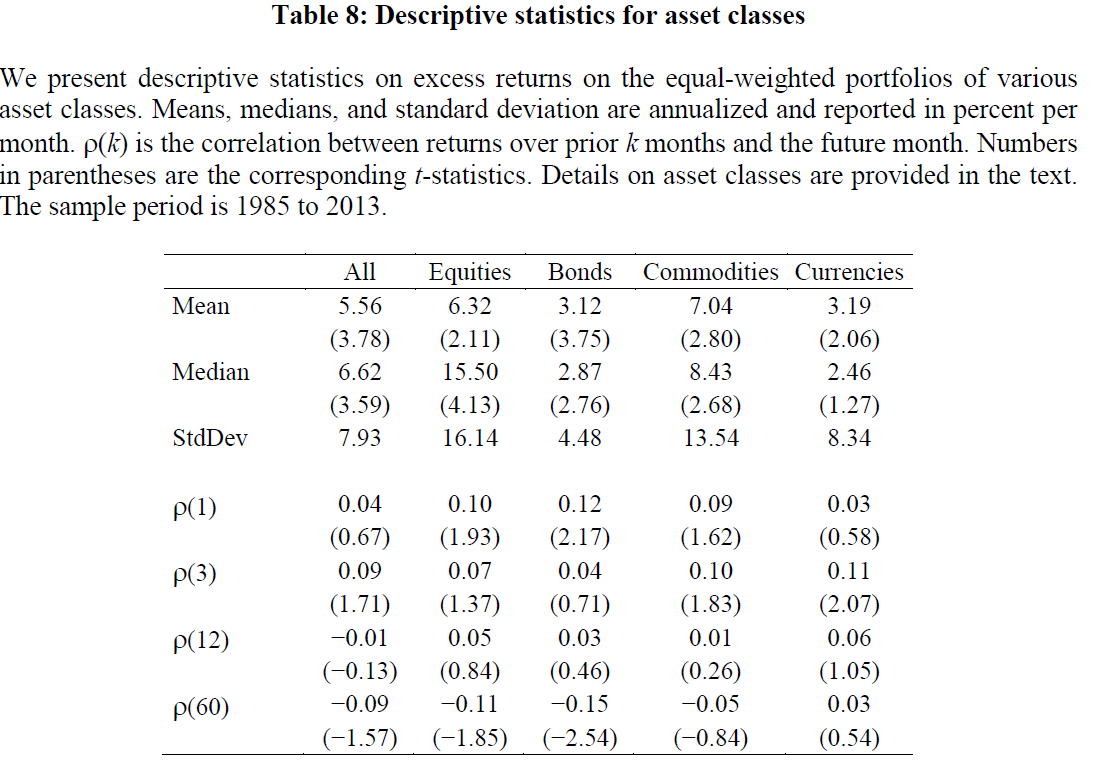

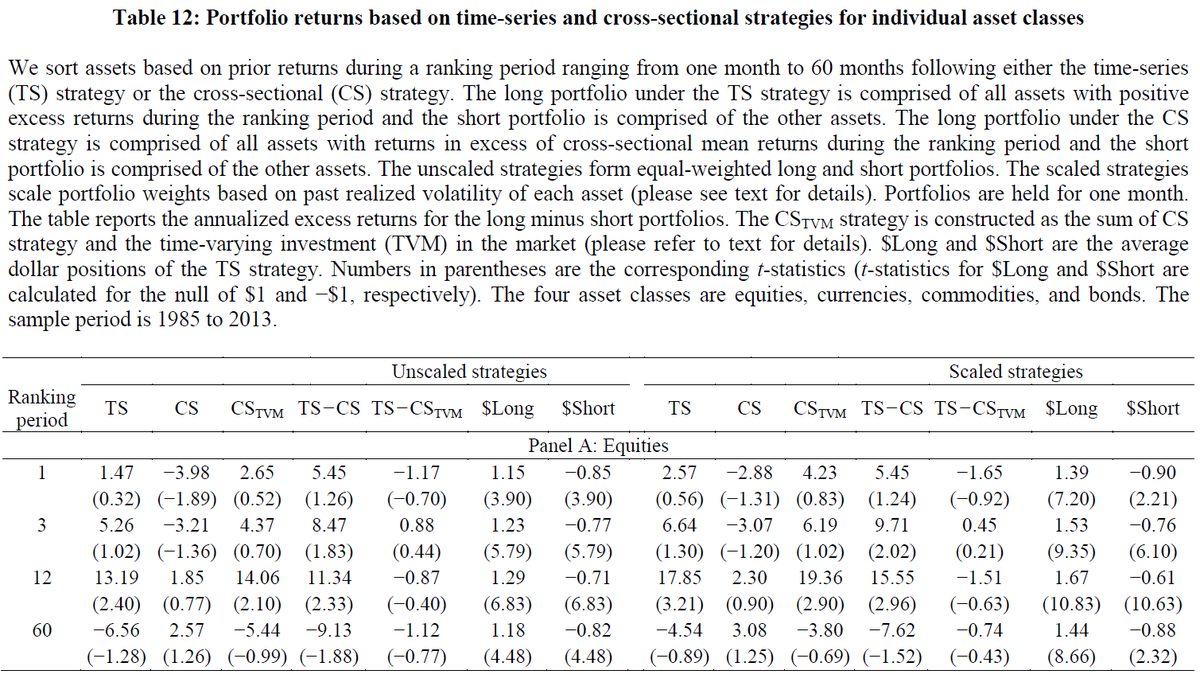

13/ The authors then perform a similar analysis for asset classes (equities, bonds, commodities, and currencies). They note that, to do a fair comparison, TS and CS portfolios should either both be equal weighted (unscaled) or both be inverse volatility weighted (scaled).

14/ TS and CSTVM perform similarly, with CSTVM having a moderate edge.

Since bonds usually trend up with low volatility, the scaled TS strategy takes a large leveraged net long position in bonds. This may partially explain why TS returns have historically looked so smooth.

Since bonds usually trend up with low volatility, the scaled TS strategy takes a large leveraged net long position in bonds. This may partially explain why TS returns have historically looked so smooth.

15/ Once cross-sectional momentum is properly volatility scaled and adjusted for TS's time-varying exposures, the adjusted cross-sectional strategies outperform the time-series strategies.

16/ TS looks moderately better than CSTVM with respect to Sharpe ratios, skewness, kurtosis, and (especially) drawdowns.

The authors attribute this to scaled TS's tendency to leverage up into bonds, which tend to have low risk and high Sharpe ratios.

The authors attribute this to scaled TS's tendency to leverage up into bonds, which tend to have low risk and high Sharpe ratios.

17/ When raw returns are considered, TS and CSTVM perform similarly in each asset class.

As noted before, the scaled version takes large net long positions in bonds.

As noted before, the scaled version takes large net long positions in bonds.

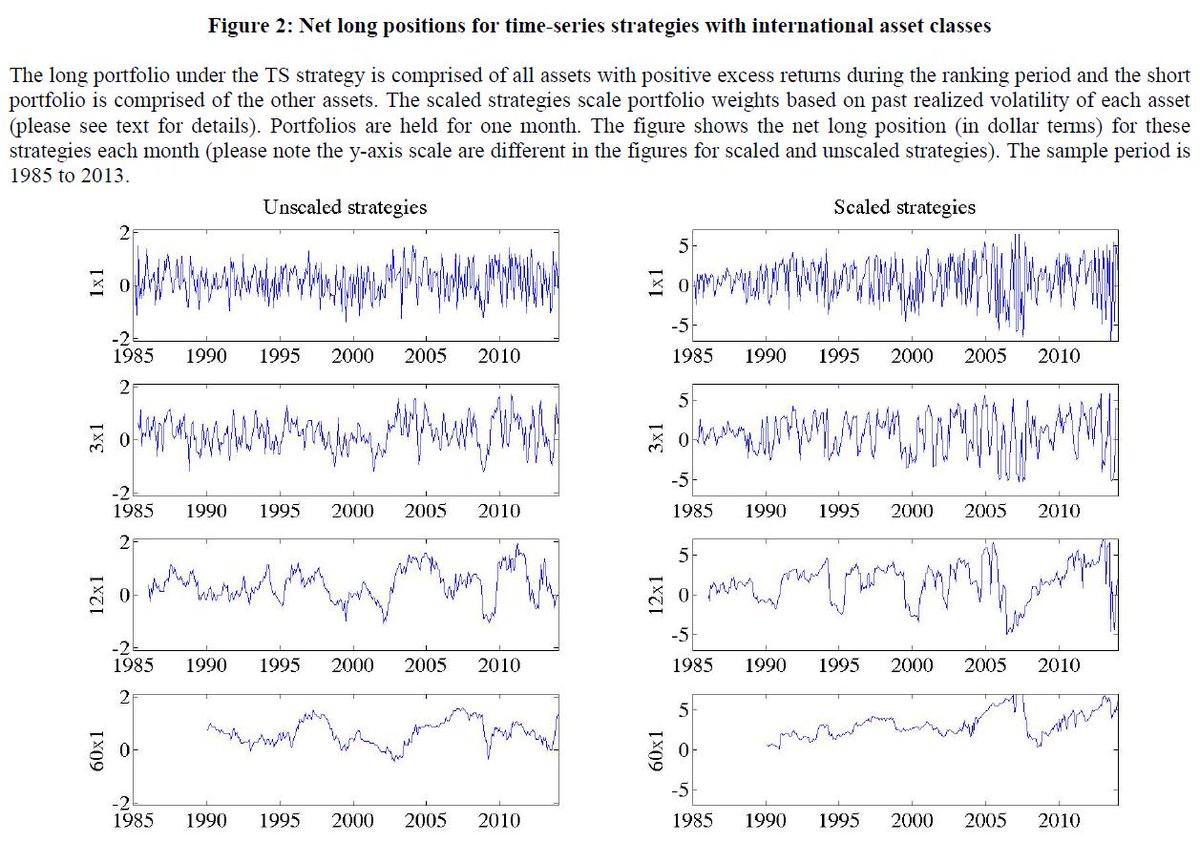

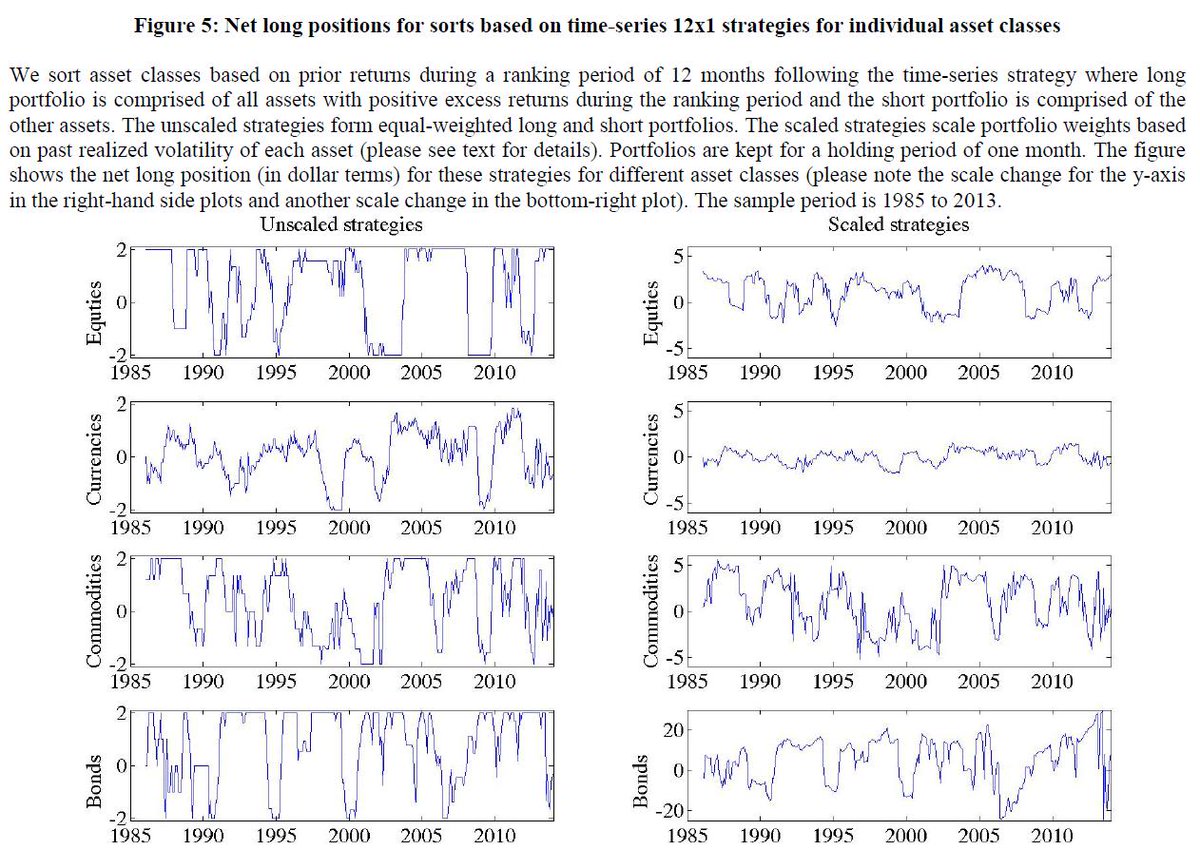

18/ Market timing provides most of the benefit with short ranking periods, while the risk premium from being net long is greater with longer periods.

The market timing (trend-following) aspect works for individual asset classes but not when asset classes are grouped together.

The market timing (trend-following) aspect works for individual asset classes but not when asset classes are grouped together.

19/ The longer the ranking period, the greater the tendency for TS and CSTVM to to be net long. (Risk premium > market timing for those periods.)

The effect is magnified for the scaled strategies (look at the scales of the y-axes on the left-hand and right-hand columns).

The effect is magnified for the scaled strategies (look at the scales of the y-axes on the left-hand and right-hand columns).

20/ The authors obtain similar results using portfolio weights that are proportional to past returns.

Overall, the authors find that TS and CS momentum perform similarly after adjusting for the former's time-varying net long exposure and differences in portfolio weighting.

Overall, the authors find that TS and CS momentum perform similarly after adjusting for the former's time-varying net long exposure and differences in portfolio weighting.