,

14 tweets,

10 min read

Read on Twitter

1/ Understanding and Trading the Term Structure of Volatility (Campasano, Linn)

"Movements in the term structure of individual equity options are driven by changes in short-term volatility. Long-term IV is slow to react to shocks in short-term IV."

papers.ssrn.com/sol3/papers.cf…

"Movements in the term structure of individual equity options are driven by changes in short-term volatility. Long-term IV is slow to react to shocks in short-term IV."

papers.ssrn.com/sol3/papers.cf…

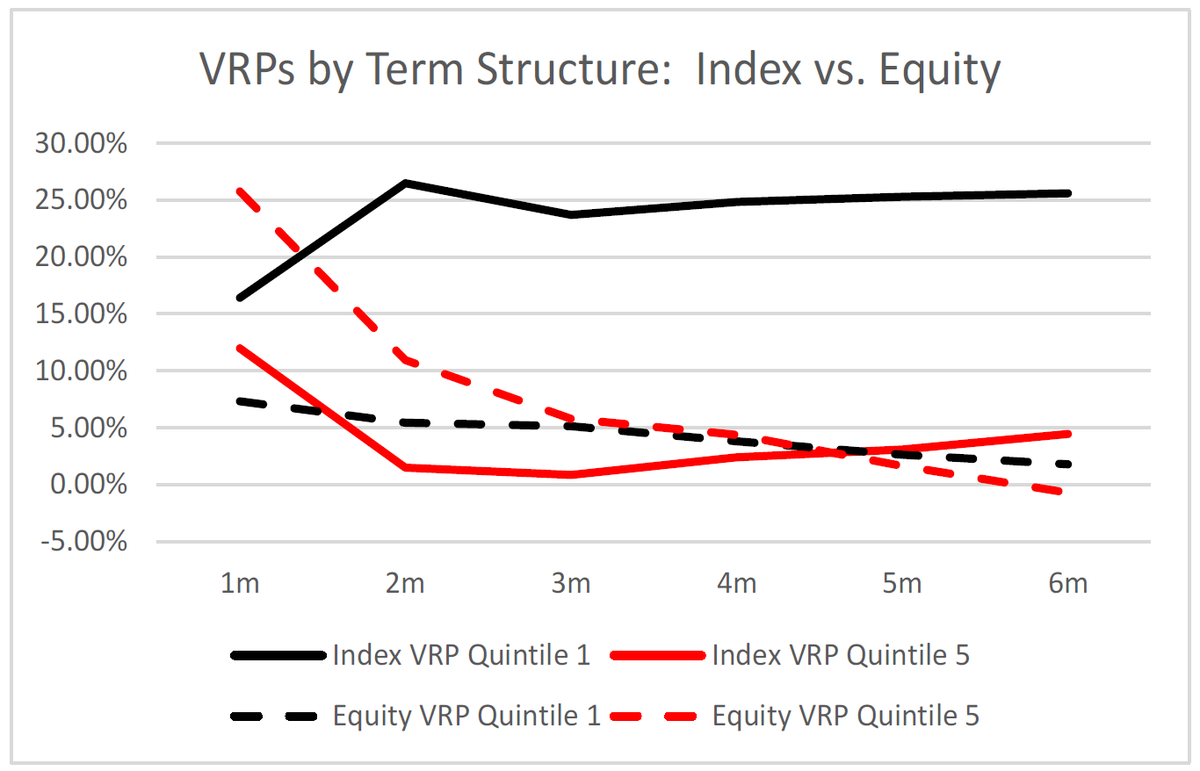

2/ VRPs look different when the IV term structure is in backwardation (quintile 5) than when it's in contango (quintile 1).

Short-dated volatility appears to "whip around" more than is justified by subsequent RV. Long-dated IV, on the other hand, does not seem to move enough.

Short-dated volatility appears to "whip around" more than is justified by subsequent RV. Long-dated IV, on the other hand, does not seem to move enough.

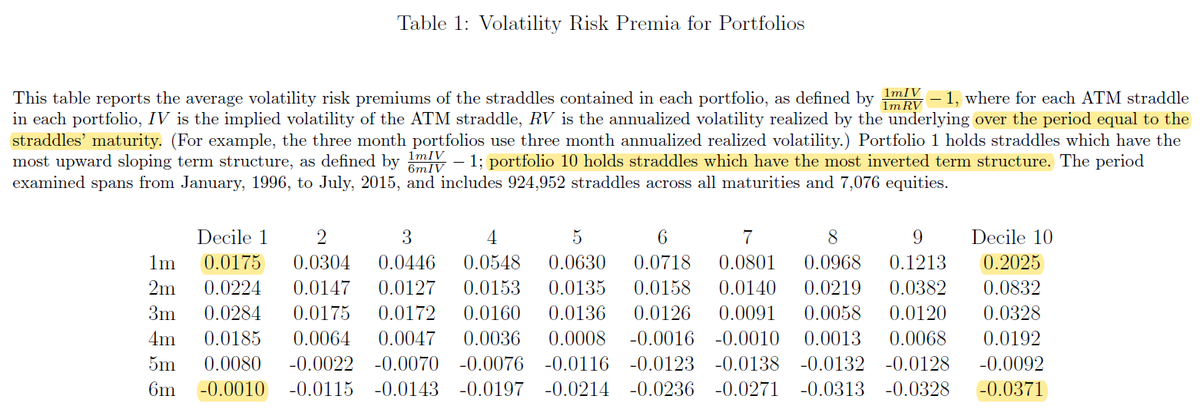

3/ 1-month VRPs in individual stocks are highest for decile 10 (backwardation).

6-m. options have *negative* VRPs (the options have positive returns), esp. in decile 10.

VRP is defined using a ratio rather than by subtraction to avoid being unduly influenced by volatile stocks.

6-m. options have *negative* VRPs (the options have positive returns), esp. in decile 10.

VRP is defined using a ratio rather than by subtraction to avoid being unduly influenced by volatile stocks.

4/ A time-series plot of decile 1 and 10 IVs shows that IVs are higher for term structures that are in backwardation.

The term structure for stocks appears to act differently than the index (SPX) term structure, and the latter might not completely explain the former.

The term structure for stocks appears to act differently than the index (SPX) term structure, and the latter might not completely explain the former.

5/ IV indeed increases monotonically as we move from contango to backwardation.

The TS slope appears to be driven by changes in short-term IV. (The magnitude of the IV differences as well as the SD of IVs both support this idea.)

IV has positive skewness in all categories.

The TS slope appears to be driven by changes in short-term IV. (The magnitude of the IV differences as well as the SD of IVs both support this idea.)

IV has positive skewness in all categories.

6/ One-month IV acts like a levered version of 6-month IV.

This becomes more true (and R-squared values decrease) as the term structure becomes more backwardated.

This becomes more true (and R-squared values decrease) as the term structure becomes more backwardated.

7/ 1-month IV and 6-month IV interact with 1-month trailing historical volatility and 12-month trailing HV in counter-intuitive ways.

It's possible that backwardated TS lead to less sensitivity to 1-month HV because of earnings announcements; the paper does not discuss this.

It's possible that backwardated TS lead to less sensitivity to 1-month HV because of earnings announcements; the paper does not discuss this.

8/ Higher trailing HV is associated with greater levels of term structure inversion, but this becomes less true as the TS becomes more inverted (coefficients and R² are both smaller).

If HV is "sticky," this may suggest that there are more trading opportunities with invert TS.

If HV is "sticky," this may suggest that there are more trading opportunities with invert TS.

9/ "When the TS is more inverted, long-term IV tends to lag behind short-term IV.

"We can think of the LT IV as taking a 'wait and see' stance. If the shock is short-lived, then LT IV is less affected. Conversely, if the shock persists, LT IV continues to react cautiously."

"We can think of the LT IV as taking a 'wait and see' stance. If the shock is short-lived, then LT IV is less affected. Conversely, if the shock persists, LT IV continues to react cautiously."

10/ "As the TS becomes more inverted, change in IV outpaces that of HV; one interpretation is that IV is overreacting to movement of the underlying."

Calendar spreads are most profitable when the TS is inverted, which is usually when IV is high.

Calendar spreads are most profitable when the TS is inverted, which is usually when IV is high.

11/ Figure 3 is inconsistent with its own description as well as the text intended to explain it on pages 20-21.

As far as I can tell, the lines actually represent the returns to portfolios that short decile 1 (contango) options and buy decile 10 (backwardation) options.

As far as I can tell, the lines actually represent the returns to portfolios that short decile 1 (contango) options and buy decile 10 (backwardation) options.

12/ The patterns seen thus far survive double-sorting on term structure and change in HV.

Another (related) pattern shows up as well: as the TS becomes more inverted, one-month options become worse at hedging HV increases, and six-month options become better at it.

Another (related) pattern shows up as well: as the TS becomes more inverted, one-month options become worse at hedging HV increases, and six-month options become better at it.

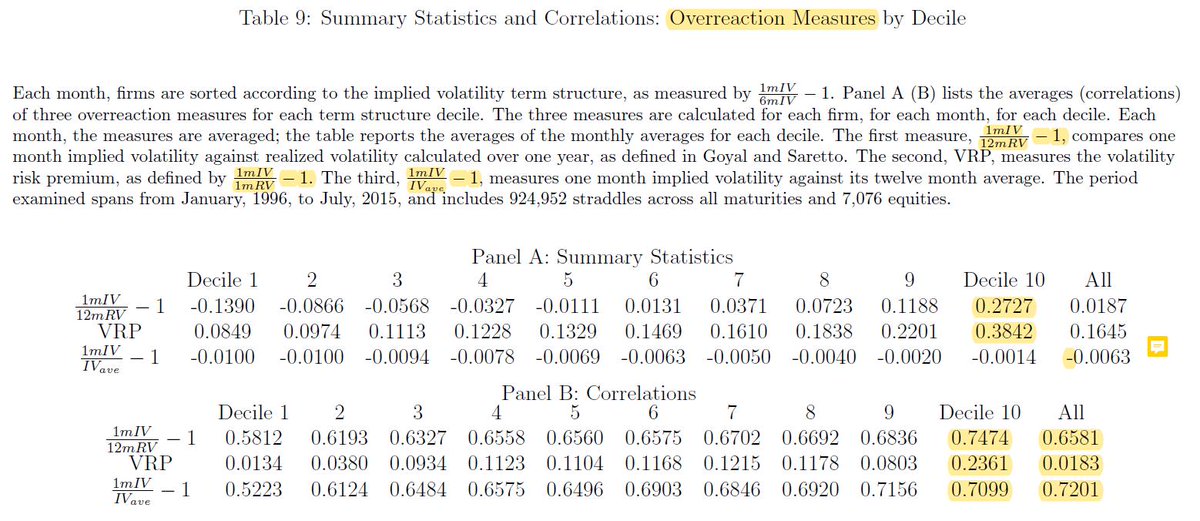

13/ As the TS becomes more inverted, IV overreaction measures are larger (slope may be a proxy for overreaction).

Correlations between overreaction measures and TS slope also increase as the TS becomes more inverted.

(I still can't figure out why 1mIV/IVavg - 1 is negative.)

Correlations between overreaction measures and TS slope also increase as the TS becomes more inverted.

(I still can't figure out why 1mIV/IVavg - 1 is negative.)

14/ Returns of "underreaction/overreaction" portfolios explain 2/3 of the profits from trading 1-month options using TS slope. (A more comprehensive composite metric might eliminate the α altogether.)

It does NOT explain (and actually strengthens) the α from 6-month options.

It does NOT explain (and actually strengthens) the α from 6-month options.