,

19 tweets,

7 min read

Read on Twitter

Borrowing rates for most developers have surged to the highest in more than a decade, in some cases about 20%.

Mortgage lenders struggling to roll over debt amid downgrades in their credit ratings.

Limited disbursals from committed Pre-sanctioned limits

livemint.com/industry/banki…

Mortgage lenders struggling to roll over debt amid downgrades in their credit ratings.

Limited disbursals from committed Pre-sanctioned limits

livemint.com/industry/banki…

Tough time to be a lender.

Even tougher to be a Regulator!

RBI can at most ensure systemic liquidity remains well provided.

How can the RBI enforce last mile liquidity which has dried up due to loss of risk appetite among lenders amidst defaults/rating downgrades?

Even tougher to be a Regulator!

RBI can at most ensure systemic liquidity remains well provided.

How can the RBI enforce last mile liquidity which has dried up due to loss of risk appetite among lenders amidst defaults/rating downgrades?

Real Estate and Real Estate Funding has been one of the least transparent and complex areas of Indian lending.

Disclosures by Dewan Housing, a AAA rated entity Jan-19, highlight the sources or risk aversion among banks/investors towards NBFCs and Real Estate financing at large.

Disclosures by Dewan Housing, a AAA rated entity Jan-19, highlight the sources or risk aversion among banks/investors towards NBFCs and Real Estate financing at large.

Procedural Lapses and Documentation Deficiencies have resulted in ambiguity in the “end use monitoring of the funds loaned”.

Brings into question the value of loan assets residing in the balance sheet.

Brings into question the value of loan assets residing in the balance sheet.

Unpaid “inter corporate deposits” getting converted into “secured loans” which were to be bridge financing.

Documentation Deficiencies - Part 2

Corporate Governance Question Marks

Documentation Deficiencies - Part 2

Corporate Governance Question Marks

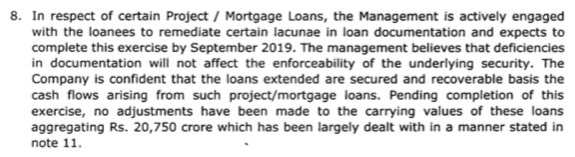

Management hopes, erm “believes”, Assets of ~Rs.208bn (Project/Mortgage loans) would face no enforceability challenges.

Documentation Deficiencies - Part 3

Documentation Deficiencies - Part 3

Repayments from Developers recognised as Revenue, but not banked! 😐

Bankers/ Investors begin to wonder - How reliable are the reported financials? Can we take decisions based on such financials with questionable revenue and cash position? 🤔

Bankers/ Investors begin to wonder - How reliable are the reported financials? Can we take decisions based on such financials with questionable revenue and cash position? 🤔

Capital is the raw material in lending business and the ability to roll over the capital determines the growth and well... the existence of a lending entity.

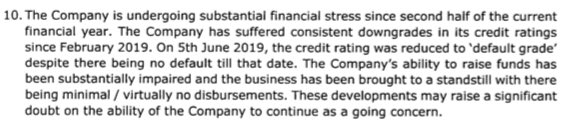

Management is honest to question the ability of the company to continue as a going concern.

Management is honest to question the ability of the company to continue as a going concern.

With business restructuring imminent and inevitable, an ~8% markdown in assets to facilitate monetisation raises further questions.

What are the implicit assumptions and the rationale for the a markdown? Does this capture or are further markdowns in store?

What are the implicit assumptions and the rationale for the a markdown? Does this capture or are further markdowns in store?

“Deficiencies identified in historical data” which are constraining the roll out of the Expected Credit Loss Model.

More questions added to the entire historical lending premise and reported financials?

More questions added to the entire historical lending premise and reported financials?

Quasi AQR report from NHB for FY18, a year before the stress emerged, deems the correct Capital Adequacy Ratio as 10.24% (v/s the reported 15.3%)!!!

Risk averness led constrained last mile liquidity to the Real Estate ecosystem has its origins in Credit Risks.

The clean up of the ecosystem will continue, but the budget proposal of credit guarantee upto 10% first loss can help clear the credit thaw & isolate problem entities.

The clean up of the ecosystem will continue, but the budget proposal of credit guarantee upto 10% first loss can help clear the credit thaw & isolate problem entities.

RBI Residential Asset Price Survey

Mumbai remains the least affordable city in India.

Mumbai remains the least affordable city in India.

Knight Frank: The mood of residential realty in Mumbai continues to be somber and withdrawn.

Unsold inventory across top eight cities recorded a decline of 9% in 1H 2019.

Mumbai was the only market to record an increase in inventory overhang of 14%.

thehindubusinessline.com/news/real-esta…

Unsold inventory across top eight cities recorded a decline of 9% in 1H 2019.

Mumbai was the only market to record an increase in inventory overhang of 14%.

thehindubusinessline.com/news/real-esta…

Omkar Developers cans its biggest slum redevelopment

More than 80 slum redevelopment projects are stuck in the city as some or other the activist has instigated the public.

dnaindia.com/mumbai/report-…

More than 80 slum redevelopment projects are stuck in the city as some or other the activist has instigated the public.

dnaindia.com/mumbai/report-…

Countering the stand of companies that homebuyers should not be part of proceedings under IBC, Govt said providing alternative remedy to them under a separate law does not violate any constitutional provisions.

Sought dismissal of all the petitions

timesofindia.indiatimes.com/city/delhi/law…

Sought dismissal of all the petitions

timesofindia.indiatimes.com/city/delhi/law…

PropEquity: Real Estate Distress due to

1. Financial distress of small developers;

2. Lack of execution capability;

3. Inventory Oversupply;

4. Excessive land banking;

5 Poor understanding of demand supply;

6. Unjustified price appreciation

economictimes.indiatimes.com/industry/servi…

1. Financial distress of small developers;

2. Lack of execution capability;

3. Inventory Oversupply;

4. Excessive land banking;

5 Poor understanding of demand supply;

6. Unjustified price appreciation

economictimes.indiatimes.com/industry/servi…

How India’s tallest building ended as an unfinished construction site

Bets on expensive property go bad in downturn, scaring off buyers/choking credit.

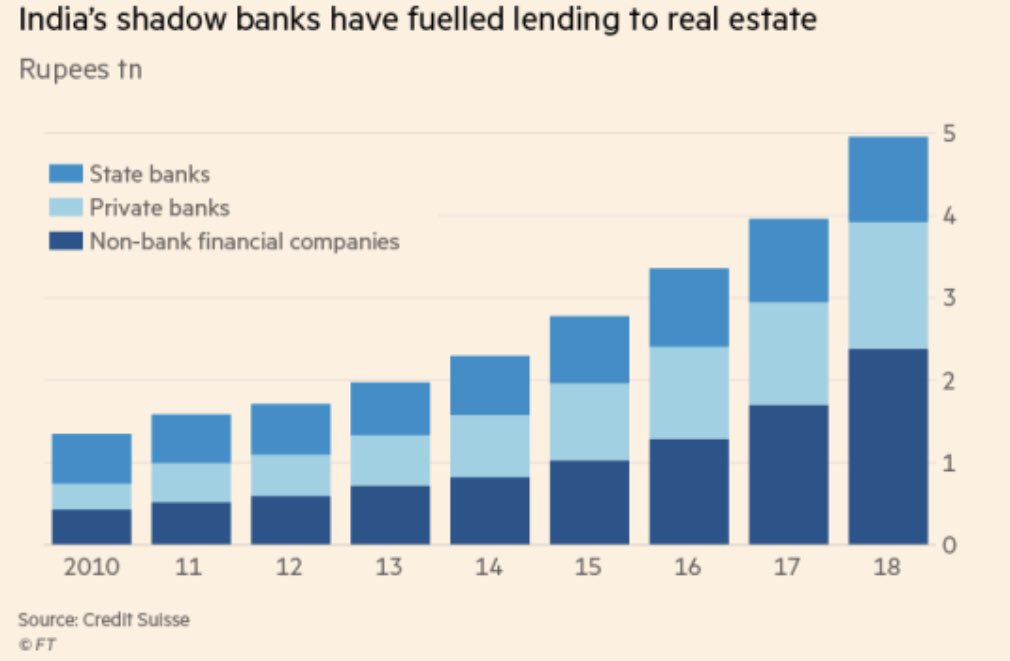

Real Estate Debt: Developers collectively owe about Rs2.5tn ($37bn) to the non-bank financial sector.

amp.ft.com/content/9f67b9…

Bets on expensive property go bad in downturn, scaring off buyers/choking credit.

Real Estate Debt: Developers collectively owe about Rs2.5tn ($37bn) to the non-bank financial sector.

amp.ft.com/content/9f67b9…

Another Real Estate NBFC defaults despite being well capitalized + Low NPAs + strong pedigree of financial sponsors.

Peak risk aversion among lenders impairing rollovers for RE-NBFCs.

Focused on lending to mid-income residential/ Commercial RE projects across Tier-1 cities.

Peak risk aversion among lenders impairing rollovers for RE-NBFCs.

Focused on lending to mid-income residential/ Commercial RE projects across Tier-1 cities.