So @CPSThinkTank is signing off 2019 with one last report - one of our most important. Thread (with graphs!).

@CPSThinkTank 'Resentful Renters', by Graham Edwards, is a new analysis of the housing/ownership crisis, arguing that the mortgage market has been one of the main drivers of the problems - and could potentially be a big part of the solution. You can read it here cps.org.uk/files/reports/…

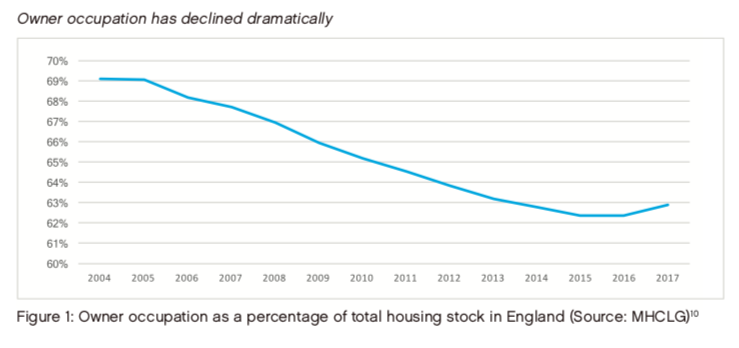

@CPSThinkTank The starting point is that, as we all know, home ownership has been falling.

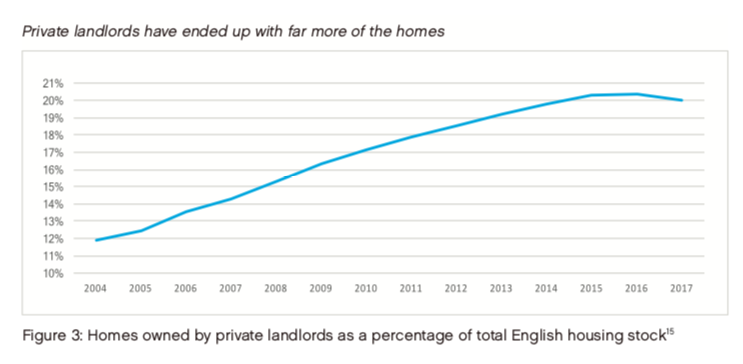

@CPSThinkTank And buy-to-let has been rising.

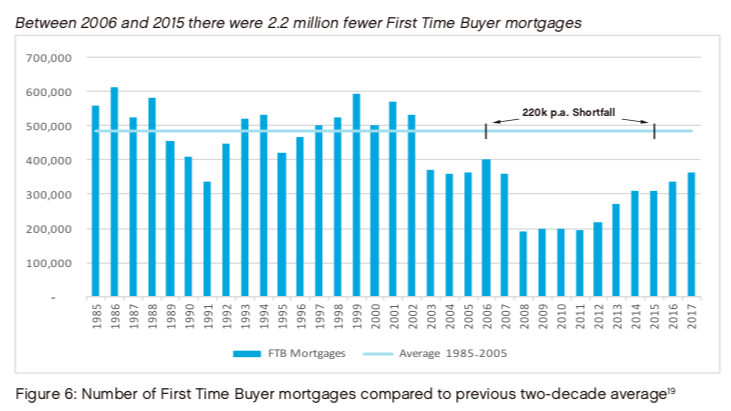

@CPSThinkTank In fact, as I pointed out in the @Telegraph today (telegraph.co.uk/politics/2019/…), first-time buyers have received 2.2 million fewer mortgages since the financial crisis, and private landlords increased their share of housing stock by 2.1 million properties

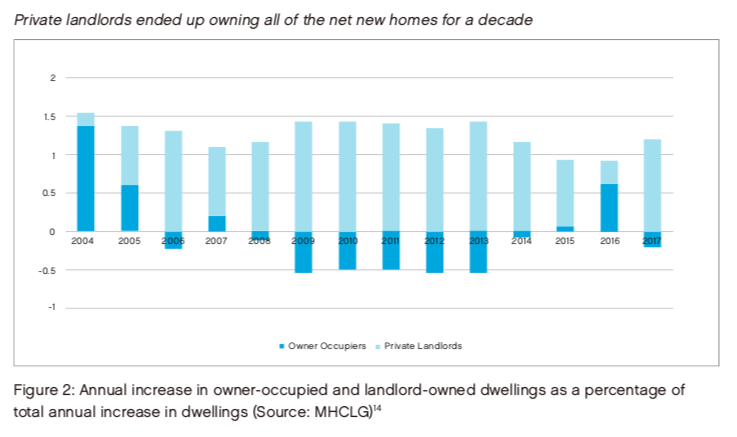

@CPSThinkTank @Telegraph In fact, on a net basis, we'd have ended up in a better position ownership-wise if we hadn't built any new homes over that decade but banned landlords from expanding their portfolios

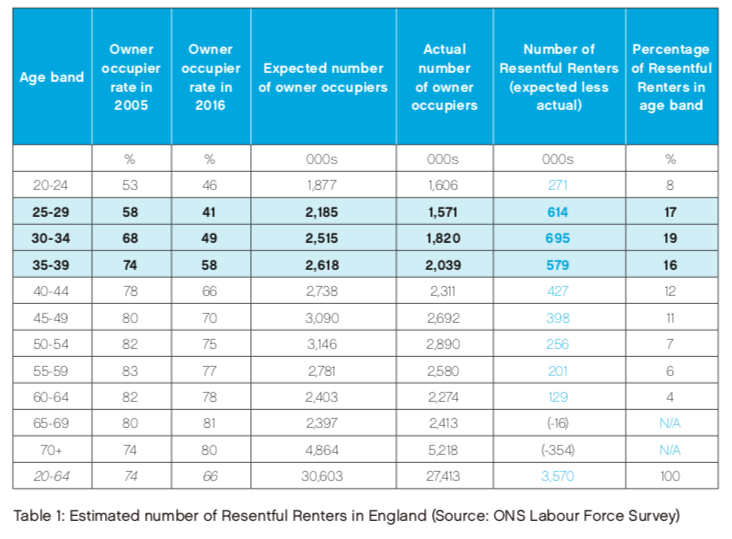

@CPSThinkTank @Telegraph In fact we have identified 3.6 million 'Resentful Renters' - those aged under 65 who would traditionally have been homeowners but now are not (the bulk of whom are between 25 and 40, as this chart shows)

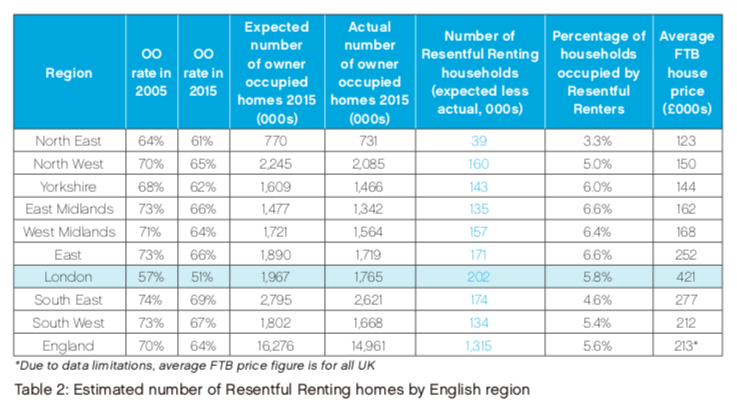

@CPSThinkTank @Telegraph But here's where it gets interesting. Over the last decade, Graham shows, this hasn't been driven primarily by house prices. House price rises have been highest in London and the SE - but the Resentful Renters are spread across the country

@CPSThinkTank @Telegraph Instead, as CPS focus groups have shown, there's a very simple problem: deposits. They've gone from being a stepping stone to home ownership to a cliff edge. It is hard to overstate how bitterly people resent this, on behalf of themselves and their children.

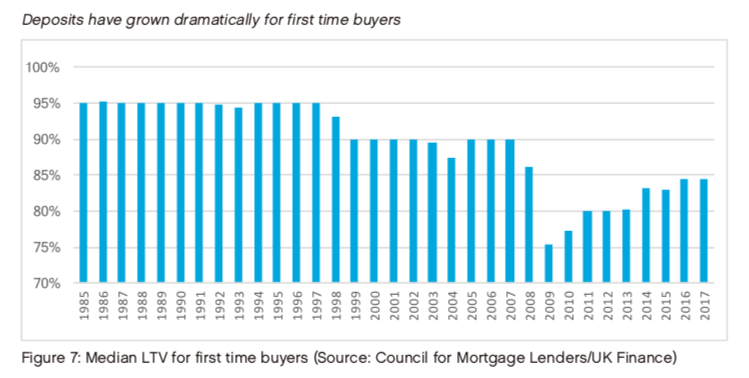

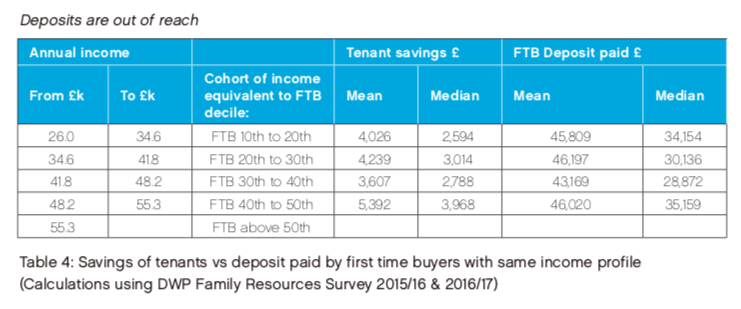

@CPSThinkTank @Telegraph You can see the evidence here. This chart shows the average first time buyer deposit - which is now three times as large as it was pre-crash.

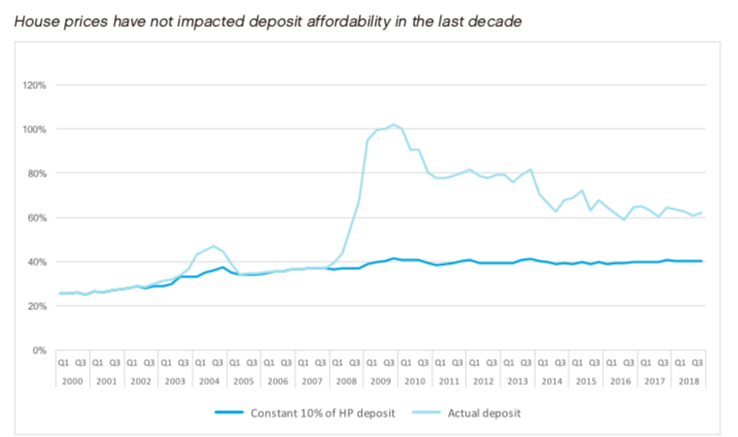

@CPSThinkTank @Telegraph And remarkable, as Graham shows, if FTB deposits had been held at 10% (not 5% as I said in Telegraph piece - sorry), they would have actually kept pace with the buyers' incomes. The top line here is actual deposit affordability - the bottom is a flat 10% rate.

@CPSThinkTank @Telegraph (Obviously for people in London this isn't as true, but we're talking nationwise here.)

@CPSThinkTank @Telegraph It's not just about deposits, but stress tests. To get a mortgage, you have to be able to pay back not just your mortgage rate, but the rate it would default to at the end of the three- or five-year period, plus an extra 3%.

@CPSThinkTank @Telegraph This means that people pay 2.35% interest on average, but are tested on whether they can afford to pay 7.26%. In other words, not 'Can they afford £633 a month?’ but ‘Can they afford £1,075 a month?’

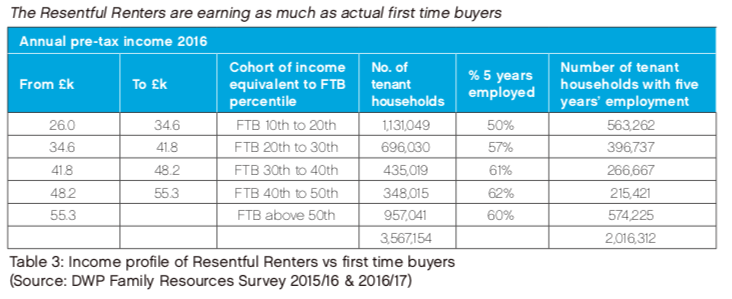

@CPSThinkTank @Telegraph And the really unfair thing about this is that the Resentful Renters are people doing exactly what they're meant to - working hard, getting on. Their financial profiles, as this chart shows, match those of actual first time buyers - they're good people with good jobs.

@CPSThinkTank @Telegraph What they don't have is the massive amount of savings (or help from Bank of Mum and Dad) that you now need to get on the housing ladder.

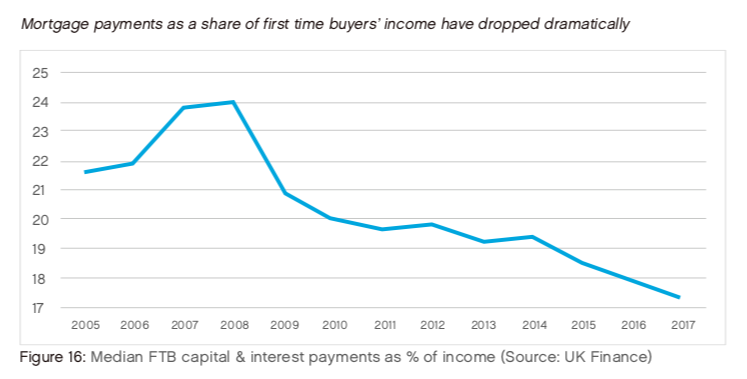

@CPSThinkTank @Telegraph The great irony here is that thanks to ultra-low interest rates, once you've actually got a mortgage, they've never been more affordable. We've created a two-tier housing market, where those who own are in clover and those who don't are in misery

@CPSThinkTank @Telegraph This, to say the least, is NOT GOOD. So how do we fix it?

@CPSThinkTank @Telegraph Graham's solution is simple. The Bank of England isn't going to relax its stress tests any time soon. But what if we could take them out of the picture - and democratise those ultra-low interest rates for the benefit of all?

@CPSThinkTank @Telegraph What he suggests is a new market in fixed-rate, long-term mortgages - which because of the certainty they offer wouldn't be subject to the stress test, and could be offered to first time buyers with much lower deposits

@CPSThinkTank @Telegraph His modelling shows that, depending on how you structure the mortgage, these could help between a million and 1.9 million households into home ownership. (Though you would also need to encourage landlords to sell up, and keep building more houses, to ensure demand matched supply)

@CPSThinkTank @Telegraph You also wouldn't need Government to underwrite it - institutional investors are crying out for these kind of attractive, long-term investments. Which is why Aviva Investors has welcomed our report.

@CPSThinkTank @Telegraph And of course the Conservatives get this, hence the inclusion of long-term, fixed-rate mortgages in the recent manifesto.

@CPSThinkTank @Telegraph In conclusion, there are many things we need to do to solve the housing crisis. But this idea could play a really important part. You can read the full thing here cps.org.uk/files/reports/…