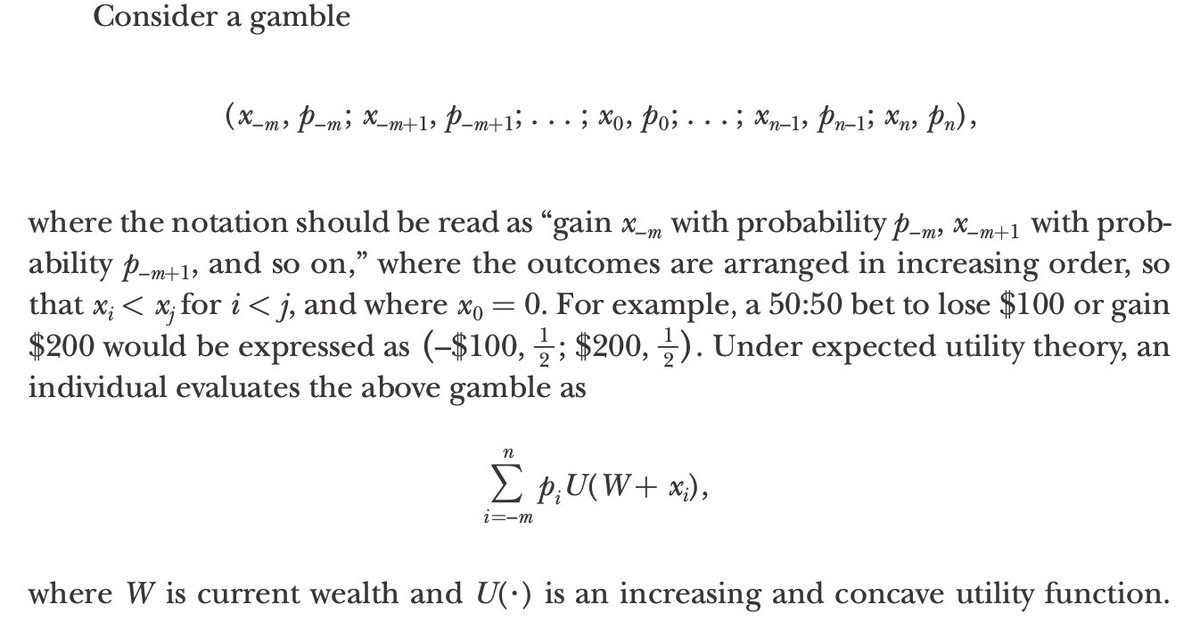

When economists define expected-utility theory, they say it optimizes E[u(t+δt)] (expected terminal utility).

That’s true, but E[u(t+δt)] here is really short-hand for E(δu), where

δu=u[x(t+δt)] - u[x(t)],

t is the time now,

and t+δt is the time after the gamble.

Barberis 2013:

That’s true, but E[u(t+δt)] here is really short-hand for E(δu), where

δu=u[x(t+δt)] - u[x(t)],

t is the time now,

and t+δt is the time after the gamble.

Barberis 2013:

Of course δu ≠ u(t+δt), but the idea is that we know our current wealth x(t) and its utility u[x(t)], and that's independent of any gamble on offer.

So we add the known constant u[x(t)] to δu, and that indeed leaves us with u[x(t+δt)].

But why are we allowed to do that?

So we add the known constant u[x(t)] to δu, and that indeed leaves us with u[x(t+δt)].

But why are we allowed to do that?

Well, adding a (deterministic) constant to δu makes no difference to decision theory. Why? Because decision theory is about ranking scalars, viz about whether

E(δu) > E(δu’)

for utilities u for one gamble and utilities u’ for another gamble.

E(δu) > E(δu’)

for utilities u for one gamble and utilities u’ for another gamble.

This inequality doesn’t change if we add the constant u[x(t)] on both sides (or any other constant), and therefore the corresponding decision theory predicts the same preferences as before.

But this short-hand confuses people into thinking that u[x(t)] and x(t) are irrelevant, and that one can write E(δu) as E[u(δx)].

But u(δx) is ill-defined without specifying x.

Descriptions of prospect theory often wrongly say that EUT has no reference-level dependence.

But u(δx) is ill-defined without specifying x.

Descriptions of prospect theory often wrongly say that EUT has no reference-level dependence.

Interestingly, people rarely (never?) point out that gaining expected utility quickly is better than gaining it slowly.

An improved EUT decision criterion would be

E(δu)/δt.

An improved EUT decision criterion would be

E(δu)/δt.

This quantity is close to something with a clear physical meaning.

If u(x) is chosen so that it grows additively over time (unlike x itself), then it is an ergodicity transformation, and E(δu)/δt is the properly defined time-average growth rate of wealth.

Yes, of wealth itself!

If u(x) is chosen so that it grows additively over time (unlike x itself), then it is an ergodicity transformation, and E(δu)/δt is the properly defined time-average growth rate of wealth.

Yes, of wealth itself!

That leads to a well-controlled formalism, which we call Ergodicity Economics. It works without psychology.

Without:

utility function

discounting function

probability weighting function

subjective perception of time

value function

moving kinks for losses and gains

…

Without:

utility function

discounting function

probability weighting function

subjective perception of time

value function

moving kinks for losses and gains

…

A simple physical formalism that agrees with evolutionary theory and solves the most puzzling problems of economic theory.

It’s both fascinating and deeply disturbing to stumble upon such a complete foundational re-imagining of a centuries-old field of formal human inquiry.

It’s both fascinating and deeply disturbing to stumble upon such a complete foundational re-imagining of a centuries-old field of formal human inquiry.